How incumbent banks can close the open finance gap styles-h2 text-white

How incumbent banks can close the open finance gap

The past six months have seen a surge in dialog surrounding the purported value of “open finance” and whether or not its potential has been realized in the UK. We see open finance as the natural evolution of finance—a collection of standards, technologies and organizations that enables consumers to access reimagined credit, asset management, insurance and pension products with greater ease and transparency from a range of bank and non-bank suppliers.

While the debate has stoked critical thinking around what financial institutions can hope to achieve through open finance, large questions remain around the potential benefits still on the table.

To better understand how financial institutions are approaching open finance, between April and July 2022, we surveyed over 200 decision makers with responsibility for open finance within their organizations. Respondents were drawn from a representative cross-section of leaders from within the CMA9, building societies and incumbent, challenger and neo banks.

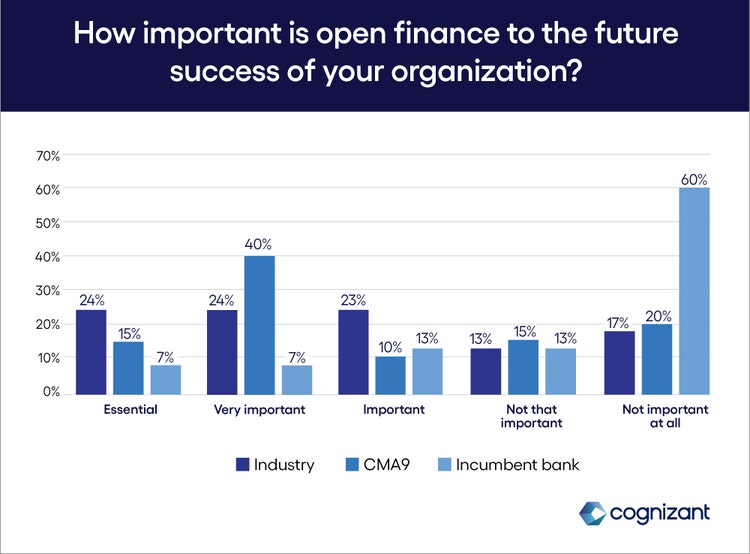

Through our research, we discovered a paradox in financial institutions’ approach to open finance. The paradox is two-pronged: First, there’s a marked inconsistency in the models that different financial organizations are using to align with the concept; second, business and investment priorities are frequently misaligned in areas where open finance could help institutions achieve their goals.

In this series, we explore the differing priorities, strategies and opinions among financial institutions to investigate the current state of play and the likely direction of travel—whether they’re confidently embracing open finance or reluctantly doing the bare minimum to comply with regulation.

“Open finance is a relatively new concept, and top management's decision to promote it is rather uncertain, particularly because of the possible harm from sharing data with third parties regarding customers' cybersecurity. Within top management, most believe open finance is an important step toward digitalization. In contrast, some believe it could be a threat, that we are not ready for the risk involved, and that it is important to change the risk management policies before it is implemented.” – Chief Product Owner PSD2/Open finance, Incumbent bank

“Our organization views open finance as imperative to our survival because customers … now expect services to be tailored to their specific needs. Open finance provides previously unavailable opportunities, like improved security and accountability, easy integration, customers having more access and control over their data, improved treasury management and new business models… I strongly believe that open finance … will transform the future of money.” – Director/Head of Open Finance, CMA9 bank