Payments networks aren’t just about payments anymore

<p><br> <span class="small">December 12, 2023</span></p>

Payments networks aren’t just about payments anymore

<p><b>What it will take to create ‘value-movement networks’ that support everything from digital currencies to non-monetary and even intangible forms of value.</b></p>

<p>Just as consumers today have a seemingly infinite number of goods and services to choose from, they also have <a href="https://www.cognizant.com/us/en/industries/banking-technology-solutions/digital-payments" target="_blank" rel="noopener noreferrer">fast-expanding ways to pay for them</a>: digital wallets, one-click payments, account-to-account, real-time payments and more. As a result, payments networks have had to evolve from what could be seen as a monorail to a multi-rail system that supports multiple payment instruments and methods.</p> <p>However, even more changes are in store for payments networks. Thanks to recent innovations like QR code payments and SoftPOS (which enables contactless smartphone payments),<b> </b>merchants can now use smartphones as payment acceptance devices. Further, alternative digital currencies like<b> </b>crypto and stable coins are adding even more new payments capabilities to an already strong multi-rail network.</p> <p>With all these changes, payments networks—once dedicated just to fiat-only currencies—need to evolve to enable trade of an ever-growing array of value types. In fact, rather than simply being payments networks, we believe these networks will evolve into “value-movement networks” that will support everything from digital currencies to non-monetary and even intangible forms of value.</p> <p>To be ready for these new payments era, payments networks and financial services companies will need to adapt in several areas, including new regulations and policies, common standards, transparent value-exchange mechanisms, trust and reliability, and data protection.</p> <h4>Shift to value movement</h4> <p><span style="font-weight: normal;">Historically, faster, more convenient, cheaper and more secure commerce has shaped the evolution of payments networks. Today, digital currencies are increasingly in use, from cryptocurrencies such as bitcoin, to the central bank digital currencies (CBDC) being explored by an increasing number of countries. Further, non-monetary forms of value are also on the rise, including carbon credits and non-fungible tokens.</span></p> <p>Meanwhile, intangible forms of value, such as time and influence, will likely emerge. An example of using time as currency is Ikea Dubai, whose “Buy with Your Time” campaign provides discounted prices to customers based on the amount of time they spent getting to the retailer’s store. Customers show staff their Google Maps timeline, and pricing is calibrated to the duration of the trip. In effect, Ikea is allowing consumers to pay with their time vs. traditional currency.</p> <p>When it comes to influence as a currency, we may see celebrities with a high number of social media followers turn that quantification of their influence into a source of exchangeable value. For example, professional footballer Cristiano Ronaldo, with over 600 million followers, could theoretically use his power of influence to pay for his hotel reservation by posting a story about his stay rather than paying in fiat currency.</p>

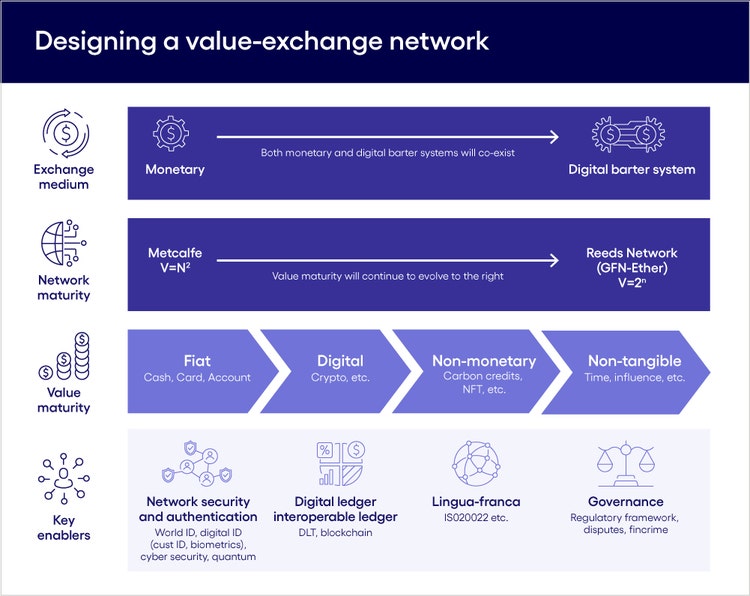

<h4><br> A new role for payments networks</h4> <p>All these forms of value will continue to co-exist in the foreseeable future. As this landscape evolves, payments networks have a great opportunity to partake in this development and be the front-runners of realizing the value ecosystem.</p> <p>The goal for the network should be to eventually become like an invisible transmission medium for all exchange of value—between individuals, businesses and governments—and facilitate the formation of subgroups on the network to enable inter/intra-group economic activity.</p> <p>An example of this is retailers’ rewards programs—which are mainly applicable today across stores from the same chain or limited subsidiaries and partners—becoming part of an interoperable, cross-organization value network. Rewards from your favorite coffee shop, for example, could be applied to book a hotel. From a payments network perspective, this means that the primary members (banks) would need to collaborate with each other to form an independent group on the network to facilitate economic activity, thereby creating the network effects.</p> <h4>Five changes needed</h4> <p>To design such a value-movement network, several aspects will have to be considered:</p> <ul> <li><b>Regulations.</b> A conducive regulatory environment would be needed to support the formation and growth of these newer forms of value and drive cross-sector collaboration. Enhanced operating policies would be needed to support the new network business model, particularly in the areas of customer complaints, data privacy, security and financial crime frameworks.</li> </ul>

#

<p><span class="small">Figure 1</span></p> <ul> <li><b>Common standards</b>. To be truly interoperable, the value-movement network would need a common lingua franca. Standards like ISO 20022 could potentially be the de-facto common language to exchange messages between the participants. The ability to transport large amounts of data in ISO 20022 messages should be exploited to include specifics of that economic activity. For example, ISO 20022 messages can contain code that provides the reason for the payment and can be used to drive personalization, KYC/AML compliance, etc.<br> <br> </li> <li><b>Transparent value-exchange mechanism.</b> To ensure consumer adoption, coexistence and interoperability of these newer values of exchange, it is imperative to have a transparent value-exchange mechanism or a “distributed yet trusted exchange factor.” This is the case for value exchanges between fiat and digital currencies, digital currencies and NFTs or an intangible value. The exchange needs to be transparent and true to all participants at a given moment in time.<br> <br> Going back to our influencer example, the hotel would need a model (a value-exchange mechanism) to calculate the worth of the influencer to trade the assets. While someone with as many followers as Ronaldo might get a royal suite, others with fewer followers would need their influence to be assessed to allocate the type of room they’d receive. So, the payments network in this case has the opportunity to provide the platform and means to offer this model.<br> <br> </li> <li><b>Trust and reliability.</b> A critical criterion for the growth of any new store of value, product or service—and, in this case, “the value-exchange network”—is consumer trust and network reliability. Such a network would need a strong governance model supported by modern authentication means, such as digital IDs (ie, the blockchain-based passport and protocol from Worldcoin, World ID) or biometrics.<br> <br> </li> <li><b>Data protection. </b>As stores of value transcend into digital forms, it will be even more important to have strong cybersecurity frameworks to protect assets, curb fraud and, more importantly, protect customer data. For example, with something like the World ID concept, a breach in the personal customer information linked and available across multiple network groups could potentially lead to risks across other network groups where the customer is participating. As a result, more security rules need to be associated around personal customer data, using encryption, tokenization and other forms while still linking to the universal digital ID.<br> </li> </ul> <h4>Can past foretell the future?<b><br> </b></h4> <p>The future of payments provides limitless possibilities to enrich customer experience. However, history tells us that data and its convergence with contemporary trends in commerce, communication, technology and more will reshape the world we live in. As a result, payments networks will also have to evolve to remain relevant. </p> <p>The scale of opportunity is massive for payments networks that enable a seamless, secure and trusted exchange of all types of value for network participants.<br> </p> <p><i>To learn more, visit the </i><a href="https://www.cognizant.com/us/en/industries/banking-technology-solutions/digital-payments" target="_blank"><i>Payments</i></a><i> section of our website or </i><a href="https://www.cognizant.com/us/en/industries/banking-technology-solutions/digital-payments#contact-us" target="_blank"><i>contact us</i></a><i>.</i></p>

<p>Rahul has 20+ years of experience in the cards and payments domain, along with diverse exposure across product companies, networks, banks, processors, PFACs fintech, and academia.</p> <p><a href="mailto:Rahulkumar.Ramakrishnan@cognizant.com">Rahulkumar.Ramakrishnan@cognizant.com</a></p>

<p>Shray has 13+ years of experience in IT and business consulting, specializing in the cards and payments domain. He has extensively worked with leading FIs in strategic digital transformation initiatives and the rollout of new payment products across the US, Europe, LATAM and APAC.</p> <p><a href="mailto:Shray.Khajuria@cognizant.com">Shray.Khajuria@cognizant.com</a></p>

<p>Shree has 23+ years of experience in digital transformation, specializing in cards and payments. He has extensively worked with domestic & international clients across different business entities, including issuers, acquirers, networks, payment processors and fintech.</p> <p><a href="mailto:Shreegopal.Ramakrishnan@cognizant.com">Shreegopal.Ramakrishnan@cognizant.com</a></p>