Gen AI is taking hold in DACH businesses

<p><br> <span class="small">October 30, 2024</span></p>

<p><b>Our recent research explores the crucial elements that will either hinder or promote the adoption of generative AI by businesses in the DACH region. Leveraging these insights, we outline strategies for companies to achieve success with this transformative technology.</b></p>

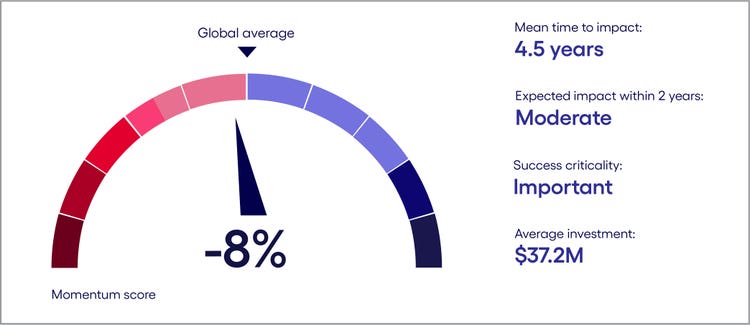

<p>Businesses in Germany, Austria and Switzerland (DACH) believe generative AI is critical to their future success. Buoyed by their conviction, businesses in the region report an average planned spend of $37 million this year, according to our recent research.</p> <p>The enthusiasm for this technology is unsurprising, given the recent surge of AI startups and investments in the region. <a href="https://www.appliedai-institute.de/en/hub/2024-ai-german-startup-landscape" target="_blank" rel="noopener noreferrer">According to a recent study</a>, Germany alone has seen a 35% increase in AI startups in 2024 compared with the previous year. The country has also seen a significant increase in AI-related patents and research and is home to the <a href="https://sciencebusiness.net/news/r-d-funding/rush-european-ai-patents-bosch-leading-successful-german-pack" target="_blank" rel="noopener noreferrer">highest number of AI patent applicants</a> at the European Patent Office. Meanwhile, over the border, Austria is predicted to see the market for gen AI <a href="https://www.statista.com/outlook/tmo/artificial-intelligence/generative-ai/austria#:\~:text=The%20Generative%20AI%20market%20in%20Austria%20is,a%20market%20volume%20of%20US$2.58bn%20in%202030." target="_blank" rel="noopener noreferrer">grow by 47%</a> from 2024 to 2030. Predictions <a href="https://www.statista.com/outlook/tmo/artificial-intelligence/generative-ai/switzerland" target="_blank" rel="noopener noreferrer">are similarly bullish</a> for Switzerland.</p> <p>However, our study also reveals that a majority of businesses (71%) in the DACH region believe they aren't moving fast enough with respect to their generative AI strategies. Over half (56%) believe these delays will result in a competitive disadvantage. And despite significant investment in generative AI, the average per-business spending this year is below the global average of $47.5 million.</p> <p>In addition, respondents express concerns that factors like talent shortages, technology insufficiencies and negative consumer perceptions may make it difficult to quickly develop and scale use cases in the DACH region.</p> <p>The fact is, regional variances—regulatory environment, flexibility of operating models, costs and available talent—will influence how successful businesses are with implementing their generative AI strategies and how they will use this powerful technology. As a result, the pace of generative AI uptake and the way in which it’s used will be uneven across the globe.</p> <p>To better understand what generative AI adoption will look like globally, we conducted a study of 2,200 business leaders in 23 countries and 15 industries, including 200 in the DACH region. The study assessed a wide range of generative AI adoption trends, including investment levels, use cases, how critical generative AI strategies are to business success, and organizational readiness to adopt the technology.</p> <p>We also analyzed 18 business factors that will either inhibit or accelerate business adoption of gen AI (see the end of the report for the full list of factors). Respondents evaluated each factor’s potential impact on their generative AI strategy, rating it as either positive or negative on a scale of high to low impact.</p> <p>From the results, we calculated a “momentum score” for each country or region. The momentum score represents the level of confidence business leaders have about their ability to roll out their generative AI strategy based on internal business factors and the prevailing local conditions of their country or region.</p> <p>For all the regions covered, inhibitors to adoption outranked accelerators, meaning that all momentum scores skewed negative. In effect, businesses globally feel constrained by their operating environment.</p> <p>To understand how different regions and countries varied relative to one another, we averaged the ratings to establish a baseline global momentum score. This approach enabled us to identify those that are more optimistic about their ability to adopt the technology compared with a global average.</p> <p>For DACH, the momentum score is 8% lower<b> </b>than the global average. The factors contributing to this score vary, but the most impactful are the comparatively more pessimistic views of talent availability and cost, and the perceptions of generative AI from both consumers and employees. Despite this, DACH businesses exhibit a more optimistic view of the flexibility of their operating models, the quality of output produced by generative AI and the readiness of their data.</p> <p><b>DACH gen AI scorecard</b></p>

#

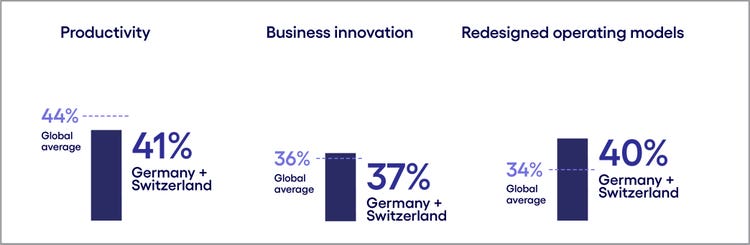

<p><span class="small">Base: 200 senior business leaders in DACH<br> Source: Cognizant and Oxford Economics<br> Figure 1</span></p> <p>As for where their generative AI investments will be aimed in the near term, we looked at two distinct uses of the technology: productivity, such as helping people work more quickly and get more done, and disrupt-the-business innovations, which involve more sweeping change to business and operating models. Overall, DACH mirrors the global trend: Over the next two years, more respondents expect to use generative AI to boost productivity than drive innovation. Crucially, businesses in the region register well above the global average for their plans to redesign operating models, as business leaders use the technology to drive significant transformation efforts.</p> <p><b>Greater focus on productivity than innovation</b></p> <p><i>Q: Which of the following best describes the role generative AI will play in your organization's business strategy in the next two years? (Percent of respondents naming each as a top-3 choice)</i></p>

#

<p><span class="small">Base: 200 senior business leaders in DACH<br> Source: Cognizant and Oxford Economics<br> Figure 2</span></p> <p>However, our study also reveals a change in what productivity means when pursued with generative AI. The end goal is not efficiency and cost-cutting, as has been the case with previous automation endeavors. Instead, the goal is to redirect productivity gains into funding endeavors that fuel growth. This new dynamic requires fresh thinking around understanding business use cases for generative AI, which we will address later in this report.</p> <p>This report identifies the regional and business factors that could either inhibit or accelerate generative AI momentum among companies based in the DACH region. It also provides an industry-specific look at how generative AI will be used, a regional focus on business readiness and strategies to successfully implement generative AI in DACH.</p>

<h4>Inhibitors and accelerators: The forces driving AI momentum</h4> <p>To dig deeper into these mechanics, rather than comparing to a global average, we will now examine how business leaders in the DACH region rate the inhibitors and accelerators within their country. By doing so, our study provides a detailed temperature check on what respondents view as the main inhibitors and accelerators to generative AI in the respective country. With this assessment, leaders can take advantage of what is working well in their local environment, while strategizing on overcoming challenges.</p> <p><b>Understanding DACH’s generative AI inhibitors</b></p>

#

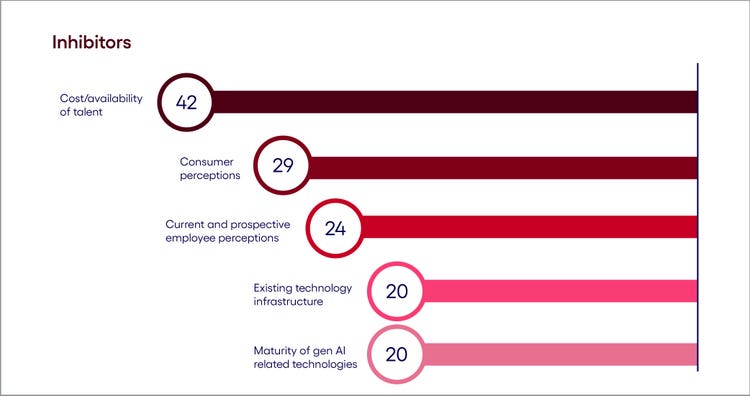

<p><span class="small">Respondents were asked which factors inhibit or accelerate their organization's adoption of generative AI. Score represents a percentage point difference to the country's momentum score compared to the global baseline.</span></p> <p><span class="small">Base: 200 senior business leaders in DACH<br> Source: Cognizant and Oxford Economics <br> Figure 3</span></p> <p><b>Talent scarcity</b> is a significant global issue and particularly acute for businesses in the DACH region. Germany—the largest economy in the region—faces challenges with worker and skills shortages in a variety of sectors.</p> <p>Perhaps the most impactful regarding the adoption of generative AI is the growing number of unfilled IT positions. <a href="https://www.bitkom.org/Presse/Presseinformation/Deutschland-fehlen-137000-IT-Fachkraefte#item-16847-close" target="_blank">A recent Bitkom study</a> reveals a current shortage of 137,000 IT specialists in Germany, marking nearly a 150% increase compared with the previous year. Meanwhile, The Adecco Group in Switzerland says the skills shortage in that country <a href="https://www.adeccogroup.com/en-ch/future-of-work/swiss-skills-shortage/swiss-skills-shortage-2023" target="_blank">reached record highs in 2023</a>, especially among IT specialists and technical engineers.</p> <p><b>Consumer perceptions </b>also rank highly as an inhibitor in the region. <a href="https://www.statista.com/statistics/1377582/opinions-artificial-intelligence-germany/#:\~:text=In%202023%2C%20around%2088%20percent,could%20strengthen%20the%20German%20economy." target="_blank">In a recent survey</a> of German consumers, roughly 88% said they believed AI software should be thoroughly checked and authorized before people are allowed to use it. At the same time, 79% also thought AI could strengthen the German economy.</p> <p>Another significant issue involves the views of both current and potential employees. In one <a href="https://www.continental.com/en/press/press-releases/germans-fear-job-losses-due-to-artificial-intelligence/" target="_blank">recent study, </a>nearly two-thirds of Germans fear the use of AI could lead to job losses. Although our findings show only 2% of executives in the DACH region intend to implement layoffs due to generative AI, these anxieties, along with concerns about ethical use and data privacy, could impede adoption.</p> <p>Companies in the region are also concerned about their <b>current technology infrastructure</b> and the <b>maturity of generative AI</b> tools on the market. Most businesses worry their outdated tech stacks will hinder adoption plans, necessitating investment in modernizing applications and infrastructure to maximize the benefits of the technology. On the flip side, they also believe the current range of solutions derived from this emerging technology is not yet advanced enough to address their business challenges.</p> <p><b>A look at DACH generative AI accelerators</b></p>

#

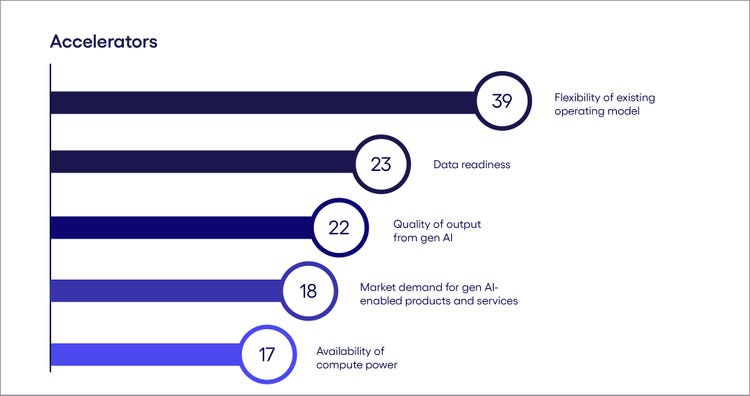

<p><span class="small">Respondents were asked which factors inhibit or accelerate their organization's adoption of generative AI. Score represents a percentage point difference to the country's momentum score compared to the global baseline.</span></p> <p><span class="small">Base: 200 senior business leaders in DACH<br> Source: Cognizant and Oxford Economics <br> Figure 4</span></p> <p>Although many businesses in DACH are concerned they are not moving fast enough when it comes to generative AI, one thing that is not stopping them, is the <b>flexibility of their operating models.</b> DACH businesses believe the agility across their operating structures will allow them to quickly adapt to changing generative AI market conditions and integrate innovative solutions into their workflows with relative ease.<br> <br> This contention is supported by the progress many businesses are making across a range of use cases (from pilots to production). According to our research, 78% are making progress on opening new revenue streams with the technology, while 77% plan to use the technology to write and test code.</p> <p>The <b>output quality</b> of existing generative AI solutions is another adoption accelerator for DACH businesses. In many ways, OpenAI’s ChatGPT captured the imaginations of businesses and individuals alike due to the speed and quality of its responses—albeit with a rocky start and multiple high-profile gaffes. But as this output has improved over the last year, business enthusiasm for generative AI has increased as well. In fact, 72% of DACH respondents are working to use the technology to engage with customers directly.</p> <p>Companies in DACH are equally optimistic about the <b>readiness of their data</b> to support generative AI-powered solutions. When asked about the current state of their technology infrastructure, 52% of businesses believe their data quality and cleanliness is in good-to-excellent condition to support generative AI strategies.</p> <p>At the same time, while companies are confident in their data readiness, other data challenges remain. Organizations in DACH are less confident in their data accessibility and security, for example. This is due, in part, to reliance on legacy technology applications, which hinder efforts to share data throughout the organization and develop accurate, timely insights.</p> <p>Perhaps unsurprisingly—given the planned investments noted above and the projected growth in gen AI markets across the DACH region—business leaders expect <b>market demand</b> for the technology to be a considerable boom for adoption.</p> <p>Leaders in the region are also bullish about the <b>availability of compute power</b>. DACH boasts the presence of a rich ecosystem of hyperscalers, regional infrastructure players and startups. Microsoft, for instance, has invested <a href="https://www.cio.com/article/1307933/microsoft-invests-e3-2-billion-in-ai-and-the-cloud-germany.html#:\~:text=Microsoft%20plans%20to%20support%20enterprises,more%20than%201.2%20million%20people.\&text=Microsoft%20will%20invest%20%E2%82%AC3.2,of%20its%20data%20centers%20there." target="_blank">€3.2billion</a> into its German data centers to double the AI and cloud capacities there.</p>

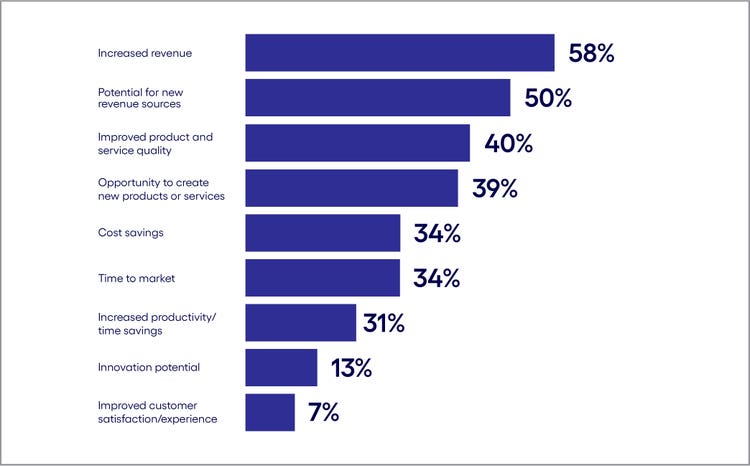

<h4>Sector spotlight: Stark differences in industries’ generative AI adoption priorities</h4> <p>Of course, there are many use cases and strategies for using generative AI. As we’ve said, businesses in the DACH region are primarily focused on realizing productivity gains with generative AI, at least in the next two years. However, a look at what’s driving their business cases sheds a new light on productivity from how it’s been seen historically.</p> <p>Traditionally, businesses have equated automation productivity gains with cost-cutting: driving down the cost of output by reducing the number of people needed to get the same volume of work done.</p> <p>While generative AI-driven automation will likely lower headcount to some degree, that is no longer the end goal. Instead, as seen through the metrics respondents will use to drive business cases, we see a shift toward redirecting productivity gains into funding endeavors that increase revenues or lead to entirely new revenue streams.</p> <p>At least 50% of DACH respondents say increasing revenue and discovering new revenue sources are the metrics that will be most important for justifying generative AI expenditures (see Figure 5). Conversely, metrics like cost savings, time-to-market and productivity were cited by 34% of respondents or fewer. In other words, the concept of productivity no longer stops at cost-cutting—businesses appear to be redirecting productivity gains into initiatives aimed at growth.</p> <p><b>Revenue is a top metric for justifying generative AI use cases</b><i></i></p> <p><i>Q: Which of the following metrics are most important in terms of justifying your organization’s generative AI business cases? (Percent of respondents naming each as a top-three choice)</i></p>

#

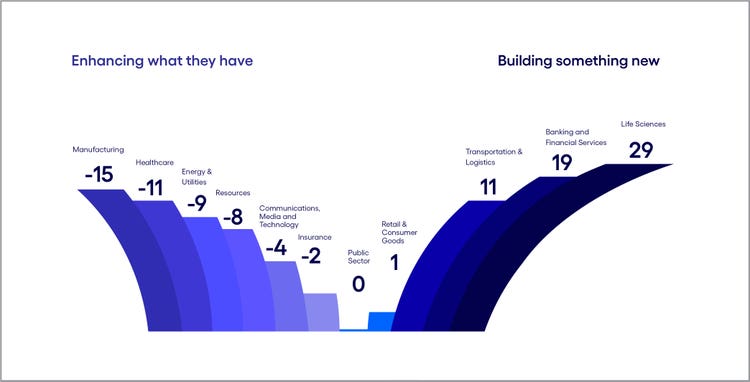

<p>Base: 200 senior business leaders in DACH<br> Source: Cognizant and Oxford Economics<br> Figure 5</p> <p>Using this more granular view of productivity goals and business drivers, we analyzed the differences in how industries intend to use the technology.</p> <p>Rather than focusing on the distinction between productivity vs. innovation, we grouped the metrics into two high-level categories of business use cases:</p> <ul> <li><b>Enhancing current business performance</b> (revenue, cost savings, time-to-market, productivity)</li> <li><b>Building something new</b> (new revenue sources, new or improved products, innovation)</li> </ul> <p>We then assigned each of the metrics a score to see the relative gap between a number-one-ranking metric and a number-three-ranking metric. By calculating the average score across industries, we could clearly see how each industry’s responses deviated from the baseline.</p> <p>Our analysis reveals stark differences among DACH industries in terms of the business use cases they’ll likely prioritize (see Figure 6).</p> <p><b>Industries diverge on business cases</b></p>

#

<p><span class="small">Note: This figure depicts each industry’s relative deviation from a baseline of “zero,” using a ranked scoring of the top-three metrics respondents cited as important for justifying their generative AI use cases. It reveals a weighted view of each industry’s overall priorities for generative AI deployment.</span></p> <p><span class="small">Base: 200 senior business leaders in DACH<br> Source: Cognizant and Oxford Economics<br> Figure 6</span></p> <ul> <li><b>The manufacturing industry </b>is primarily focused on innovative developments.<b> </b>For instance, German automaker <a href="https://www.volkswagen-newsroom.com/en/press-releases/world-premiere-at-ces-volkswagen-integrates-chatgpt-into-its-vehicles-18048" target="_blank" rel="noopener noreferrer">Volkswagen is incorporating gen AI</a> into its vehicles by integrating ChatGPT into its IDA voice assistant. In the future, customers in all Volkswagen models equipped with the IDA voice assistant will be able to easily get answers to their spoken natural-language queries in a variety of languages.<br> <br> Meanwhile, Switzerland-based food manufacturer Nestlé is using generative AI <a href="https://www.nestleusa.com/stories/unlocking-new-opportunities-gen-ai" target="_blank" rel="noopener noreferrer">in many aspects of its business</a>, from supporting consumer relationships to developing product innovation insights to anticipating stockouts at retail locations and optimizing pricing and promotions.<br> <br> The company has embedded the technology into the front end of its product innovation process, helping teams generate and test product ideas faster and more efficiently. The technology analyzes real-time market trends and consumer insights from more than 20 Nestlé US brands to suggest product concepts for exploration and testing, which has accelerated the product ideation process from six months to six weeks.<br> <br> </li> <li><b>In the insurance sector, </b>Swiss Re <a href="https://www.swissre.com/press-release/Swiss-Re-launches-Swiss-Re-Life-Guide-Scout-a-Generative-AI-powered-underwriting-assistant/d0d00d41-755c-4f0b-8bba-95a39b6fc21d" target="_blank" rel="noopener noreferrer">is changing how its clients manage risk</a> by introducing a generative AI version of its highly regarded underwriting manual Life Guide, which helps clients understand current and future risks so they can make informed decisions and build strong, sustainable portfolios. With this new edition, clients have access to a generative AI-powered underwriting assistant that generates swift answers compiled from curated expert knowledge in response to natural-language questions. This enables them to make faster, more precise decisions and improves knowledge transfer.<br> <br> </li> <li><b>In contrast, the banking sector </b>is focused on improving its existing operations. Recently, the Swiss private banking group Pictet partnered with AI startup Unique AG to give more than 5,000 employees access to an internal GPT-powered platform that enables them to create tailored client proposals, swiftly access regulatory compliance information and compose personalized emails.<br> <br> In Germany, Deutsche Bank <a href="https://www.hfsresearch.com/research/deutsche-bank-partners-with-publicis-sapient/" target="_blank" rel="noopener noreferrer">is using generative AI in a variety of ways</a>, including augmenting software code development, creating chatbots that work as advisers and assistants to employees, and improving anti-money laundering and regulatory compliance, such as detecting market abuse or suspicious activity using automated transcriptions of conversations. With these applications, Deutsche Bank believes it can enhance customer service, boost efficiency and employee productivity, manage risk, accelerate the speed of bringing new products to the market, and improve its ability to react to the fast-changing environment.<br> <br> </li> <li><b>The life sciences sector is also prioritizing improvements</b> to their current capabilities. Along with other major life sciences firms, Switzerland-based Novartis <a href="https://www.fiercebiotech.com/cro/novartis-makes-investment-ai-firm-yseop-clinical-trial-writing" target="_blank" rel="noopener noreferrer">has invested in French AI company Yseop</a>, a leader in generative AI for regulated industries. This investment aims to automate aspects of clinical trial report writing, potentially accelerating drug development. The strategy involves utilizing a natural language processing system to expedite clinical study submissions by analyzing data and automating the creation of essential documentation.</li> </ul>

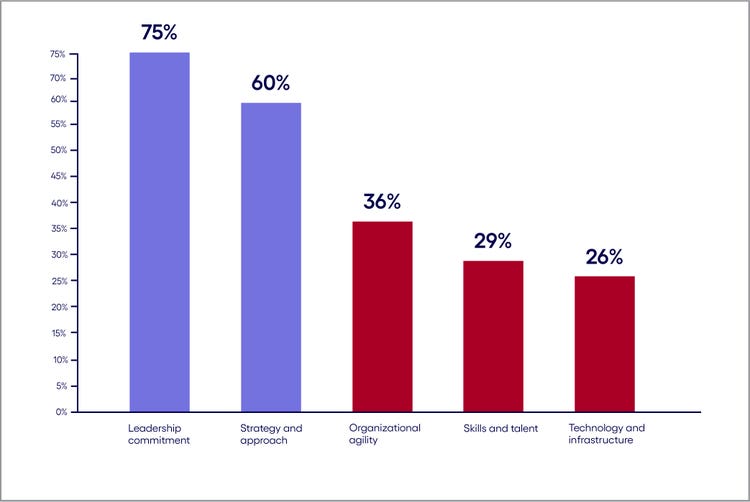

<h4>Business constraints: Talent shortages and shaky technology foundations</h4> <p>A remaining question is whether businesses are ready to drive real value from these business cases.</p> <p>The answer, according to our research, is mixed. To better understand how prepared executives believe their business is ready or not to adopt generative AI, we asked respondents to rank their organization’s maturity on a scale of 1 to 4 by selecting a statement that best described their organization in the following five areas, from low maturity to high:</p> <ul> <li>Organizational agility </li> <li>Leadership commitment </li> <li>Skills and talent </li> <li>Strategy and approach </li> <li>Technology and infrastructure</li> </ul> <p>The message from business leaders in DACH is clear: Leadership commitment is high, and strategies are robust. However, the fundamental operational and technological building blocks necessary to adopt generative AI are lacking (see Figure 7).</p> <p><b>Leadership support is sound, but fundamentals are lacking</b></p> <p><i>Respondents were asked to rate the maturity of their organization's operations in relation to generative AI. (Percent of respondents rating each as a 3 or 4, with 4 representing the highest level of maturity.)</i></p>

#

<p><span class="small">Base: 200 senior business leaders in DACH<br> Source: Cognizant and Oxford Economics<br> Figure 7</span></p> <p>Unsurprisingly, given that talent shortages sit high on the list of the biggest inhibitors impacting DACH, respondents assign low ratings to the maturity of their business’s skills availability and talent strategy. When it comes to the underlying tech infrastructure, while data readiness is rated highly as an accelerator, many other foundational aspects are lacking. <a name="_Hlk179901131" id="_Hlk179901131"></a>These include the ability to comply with company rules, policies and frameworks, data security and data accessibility. All of these technology infrastructure capabilities received a rating of "needs improvement" and even “non-existent” by the majority of respondents.</p>

<h4>Path to success: Strategic recommendations for DACH businesses</h4> <p>The challenge ahead is to overcome the inhibitors of change while also taking advantage of the factors that could boost generative AI adoption.</p> <p>To navigate these challenges, executives should prioritize the following actions:</p> <ul> <li><b>Explore partnerships to overcome the talent shortage:</b> In light of the significant talent shortages identified as a top inhibitor in the DACH region, businesses should consider forming strategic partnerships with educational institutions and other organizations. This can help bridge the gap in skills availability and enhance talent strategies. <br> <br> By fostering collaborative training programs and offering internships, companies can cultivate a skilled workforce that is well-versed in generative AI technologies. Additionally, tapping into a broader talent pool through partnerships can provide fresh perspectives and innovative solutions that are critical for successful AI implementation.</li> </ul> <ul> <li><b>Build trust in the tech:</b> It's imperative for businesses to establish trust in generative AI technologies among their stakeholders. Given the high ratings for data readiness but low ratings for compliance with company rules, policies and frameworks, businesses must prioritize transparency and robust data governance practices. <br> <br> By ensuring that AI implementation aligns with existing regulations and ethical standards, companies can build confidence among employees, customers and partners. Implementing stringent data security measures and fostering an environment of openness about how AI technologies are utilized could further solidify trust and drive adoption.</li> </ul> <ul> <li><b>Invest in a robust technology infrastructure:</b> While data readiness is considered a significant accelerator, other foundational aspects of tech infrastructure, such as data security and accessibility, require substantial improvement. Businesses should invest in modernizing their IT infrastructure to support the seamless integration of generative AI. <br> <br> This includes upgrading data storage solutions, enhancing cybersecurity protocols and ensuring that data is easily accessible yet secure. A robust technology infrastructure not only supports the efficient deployment of AI solutions but also ensures scalability and resilience in the face of evolving business needs.</li> </ul> <p><i>*The full list of regional factors we evaluated includes: the flexibility of the existing operating model, market demand for gen AI-enabled products and services, data readiness, quality of output from gen AI, availability of compute power, cost/availability of gen AI-related technologies, shareholder/investor sentiment, regulatory environment, sustainability, national infrastructure, cost/availability of capital, data privacy and security, existing technology infrastructure, current and prospective employee perceptions, flexibility of the existing business model, maturity of gen AI-related technologies, consumer perceptions and cost/availability of talent.</i></p> <p><i>Learn about the impact of generative AI on jobs and the economy in our report </i><a href="https://www.cognizant.com/us/en/gen-ai-economic-model-oxford-economics" title="https://www.cognizant.com/us/en/gen-ai-economic-model-oxford-economics" target="_blank"><i>New work, new world</i></a><i>.</i></p>

Jump to a section

Introduction #spy-1

Inhibitors and accelerators: The forces driving AI momentum #spy-2

Sector spotlight Stark differences in industries’ gen AI adoption priorities #spy-3

Business constraints: Talent shortages and shaky tech foundations #spy-4

Path to success: Strategic recommendations for DACH businesses #spy-5

<h5>Authors</h5>

<p>Dr. Kathrin Kind-Trueller, Director for AI and Advanced Analytics at Cognizant, began her career in 1999 at Siemens. She has developed ADAS, engine management, and autonomous driving functions at Bosch, ZF-TRW, BMW, and more. She holds a doctorate in AI and multiple advanced degrees.</p>

<p>Ramona Balaratnam is a Manager in Cognizant Research. With extensive experience in the Consulting industry, she delves into strategic research to uncover innovative market insights and analyze their impact across industries and businesses.</p>