RESEARCH

Big changes are ahead for health insurers as consumers adopt AI

<p><br> August 29, 2025</p>

<p><b>Our AI Inclination Index reveals which consumers are most open to using AI in the health insurance journey—as well as where and how they’ll use it. These insights can empower health insurers to develop an effective and nuanced consumer-facing AI strategy.</b></p>

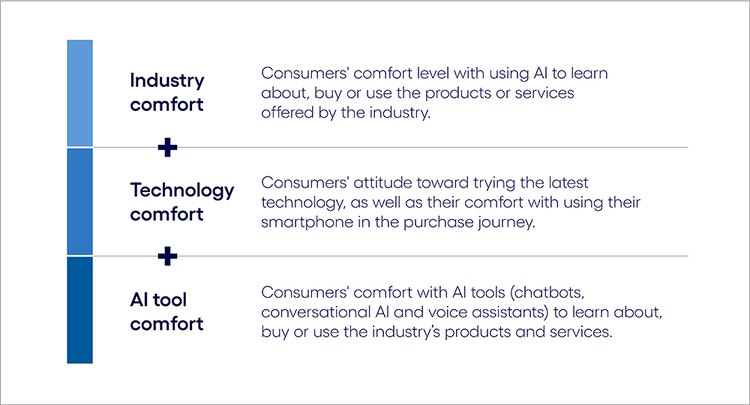

<p>Buying health insurance products and services can leave the average consumer feeling overwhelmed and ill-informed. Most people would happily say goodbye to reviewing and reselecting plans each year, investigating coverage options and experiencing the unwelcome surprise of out-of-pocket fees and claims denials.</p> <p>AI could go a long way toward reducing those frustrations and complexities. Increasingly sophisticated consumer AI tools could help curate insurance plan options, identify coverage gaps and streamline communication between health providers and payers.</p> <p>However, the growing use of consumer AI poses a distinct challenge for health insurers aiming to engage customers on their terms and capitalize wisely on the opportunity. This comes at a time when the use of AI in health insurance has, in some cases, raised questions for consumers about the decisions made in insurance claims and beyond. Health insurers need to determine which individuals are most (and least) inclined to use AI, the preferred tools and the exact points where AI integration would be most suitable.</p> <p>Our recent research uncovered some surprising answers to those questions. Using data from <a href="https://www.cognizant.com/us/en/aem-i/new-minds-new-markets-ai-customer-experience" target="_blank" rel="noopener noreferrer">our consumer AI study</a>, we developed the AI Inclination Index, which quantifies consumers’ propensity to use AI (see explainer box below). While the index reveals that consumers are slightly less inclined to use AI in health insurance than in other industries (see Figure 1), that broad finding masks important variations.</p> <p>Consumer attitudes toward AI differ significantly depending on whether they’re learning about, buying or using products and services and which of the four health insurance product categories they are in. While the US market typically encompasses health, pharmacy, long-term care and areas such as dental and vision, our research focused on the four categories listed below:</p> <ul> <li>Health insurance plans</li> <li>Prescription drugs</li> <li>Health monitoring (wearables, in-home monitoring)</li> <li>Health services</li> </ul> <p><b>The AI Inclination Index</b></p> <p><i>To quantify consumers' propensity to adopt AI-driven technology features throughout the consumer journey, we developed the AI Inclination Index. The index was calculated using three measures from our New Minds, New Markets survey data.</i></p>

#

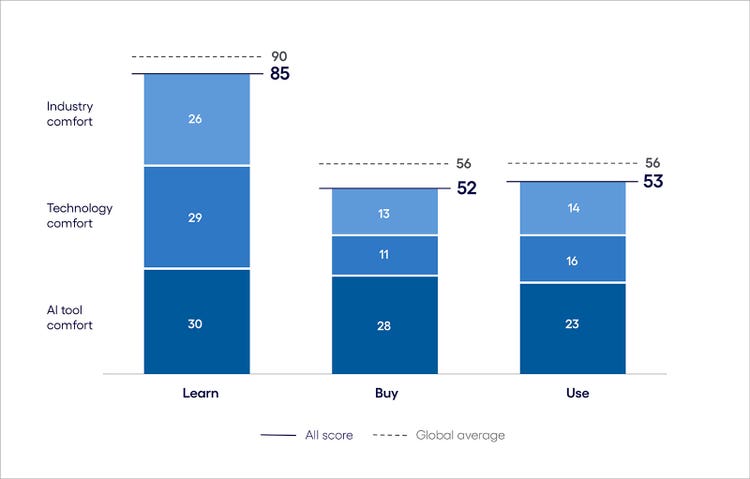

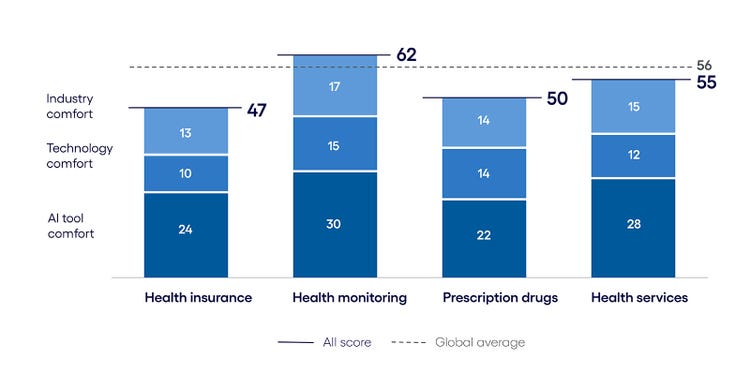

<p> </p> <p><b>AI inclination in health insurance vs. the global average</b></p> <p><i>Consumers are somewhat less inclined to use AI when purchasing health insurance products and services than other industries’ goods. </i></p>

#

<p><span class="small">Figure 1 <br> Base: 8,451 respondents in the US, UK, Germany and Australia <br> Source: Cognizant Research</span></p>

<p>For instance:</p> <ul> <li><b>Consumers are most interested in using AI in the Learn phase.</b> This is particularly true when it comes to choosing an insurance plan and researching the growing number of health monitors on the market. The Learn phase is where consumers are most inclined to use AI to help save time and make more informed decisions. At the same time, inclination index scores for prescription drugs and health monitoring devices exceed the global average in the Buy and Use phases of the customer journey, respectively.<br> <br> </li> <li><b>Older consumers (55+) are the most compelled to use AI.</b> Typically seen as slower to adopt new technology, older consumers are more familiar with the complexities of health insurance and the costly consequences of a poor decision. Conversely, younger populations, who might generally be more AI-savvy, have less need to make health insurance decisions, particularly as they can stay on their family's plan until the age of 26.<br> <br> </li> <li><b>Different tools have their shining moments throughout the purchase journey.</b> While conversational AI is preferred in the Learn phase when consumers are seeking a knowledgeable sounding board, AI voice assistants are the tool of choice in the Buy phase when fast transactions like quick purchase confirmations are involved. Tool preferences are more varied during the Use phase, depending on product category and age group.</li> </ul>

<p>With these variances, it’s clear healthcare payers will need to craft a highly precise and nuanced AI strategy that captures the greatest areas of opportunity while avoiding low-value pursuits.</p> <p>Understanding consumer use of AI, as well as the accompanying pockets of spending power, is essential for leaders in all industries. In our global study <a href="https://www.cognizant.com/us/en/new-minds-new-markets-ai-customer-experience" target="_blank" rel="noopener noreferrer">New minds, New markets</a>, we found that consumers who are enthusiastic about using AI will account for up to 55% of all spending made across industries. This amounts to $4.4 trillion in spending in the US alone and from $540 billion to $690 billion in Germany, Australia and the UK.</p> <p>In this report, health insurers will learn about where in the purchase journey consumers are most and least inclined to use AI, the AI tools they would be most apt to use and how this differs among consumers across age groups. With this information, businesses can reshape their approach to customer engagement—where and how it matters most.</p>

<h4>AI across the health insurance journey</h4> <p>As our AI Inclination Index indicates, consumers are less likely than the global average to use AI across all three stages of the health insurance consumer journey: Learn, Buy and Use. This disparity is particularly high in the Learn and Buy phases, where scores are about 7% lower than the global average.</p> <p>But a closer analysis reveals the different dynamics at play between the health insurance product categories in our study.</p> <p>For example, the Learn phase shows the highest index scores across all product categories. Health monitors lead the way, with health insurance and health services close behind, while prescription drugs lag. However, in the Buy phase, trends mirror those of our cross-industry report, where overall consumer interest drops when it comes to AI-automated purchasing. In particular, technology comfort and AI tool comfort scores nosedive by nearly 50% across all product areas.</p> <p>In the Use phase, the scores show an uptick from the Buy phase but are still not as strong as the Learn phase. Here, scores for insurance, prescription drugs and health services are all below those of monitoring devices.</p> <p>These variances among product categories are important to keep in mind as we review how consumers feel about using AI across all purchase stages of the health insurance industry.</p>

About our analysis

To understand consumer AI behaviors and attitudes at a granular level, we structured our analysis around four key pillars:

- The consumer journey. We studied the specifics of AI use at each phase of the customer journey. This journey—how consumers discover, purchase and engage with products and services before and after a sale—is at the heart of the business-customer relationship.

- Consumer demographics. To gain a better understanding of how consumer attitudes and behaviors differ by age group, we divided consumers into five categories: 18-24, 25-34, 35-44, 45-54, and 55+.

- Consumer AI tools. We defined consumer AI use by asking about their intended use of three key tools that are prevalent in the consumer world: voice assistants, chatbots and conversational AI.

- Industry-specific products. We included four health insurance product categories in our analysis: health insurance plans, prescription drugs, health monitoring devices and health services.

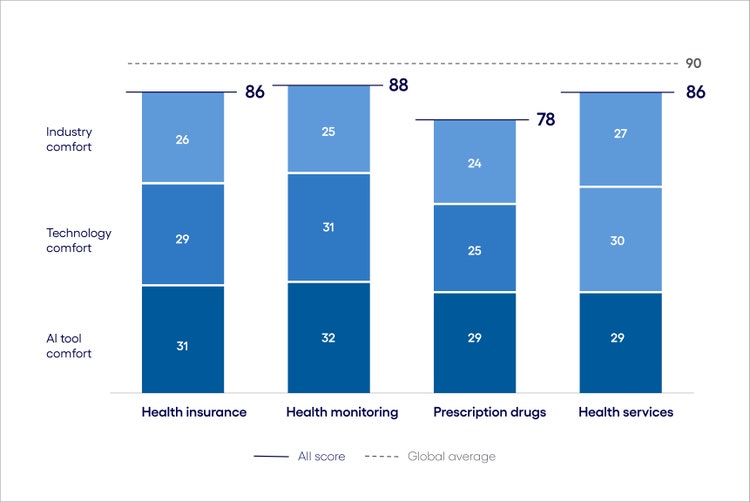

<h5><b>The Learn phase: Information overload drives AI interest in health insurance</b></h5> <ul> <li><span class="eds-label">Insurance plans, health services and monitors capture the highest AI interest</span><br> <br> </li> <li><span class="eds-label">Older consumers are the biggest AI enthusiasts at this stage</span><br> <br> </li> <li><span class="eds-label">Conversational AI leads the charge</span></li> </ul> <p>The discovery phase is where consumers are most inclined to use AI-enabled tools in the healthcare payer industry. The Inclination Index score for the Learn phase is 33 points higher than in the Buy phase. Among the four product categories, prescription drugs are the furthest below the global average (see Figure 2). </p> <p>This is the stage when consumers are researching insurance plans, monitoring devices and treatment pathways, determining which would be the best fit and at what cost. Whether it’s understanding which providers are in-network for a given plan or learning about prescription drugs, AI tools can play a role here in helping people feel more informed and in control of their health outcomes.</p> <p>As such, the Learn phase represents a prime opportunity for businesses to capture attention and influence decisions. Doing so starts with understanding what consumers value about using AI in this phase and the AI tools they’re most apt to use. </p> <p><b>Health insurance AI Inclination Index: The Learn phase</b></p>

#

<p><span class="small">Figure 2<br> Base: 8,451 respondents in the US, UK, Germany and Australia<br> Source: Cognizant Research</span></p> <h6><b>Insurance plans, health services and monitors capture the highest AI interest</b></h6> <p>With premiums <a href="https://www.kff.org/report-section/ehbs-2024-section-1-cost-of-health-insurance/" target="_blank" rel="noopener noreferrer">rising 25% in the last five years</a>, consumers value the idea of AI assisting with identifying a health plan that will minimize their costs and provide the coverage they need. When it comes to churning through the array of premiums, deductibles, coinsurance, copays and in- and out-of-network options, few consumers feel equipped to get it right.</p> <p><a href="https://theconversation.com/choosing-health-insurance-is-so-complicated-23-of-workers-with-only-two-choices-picked-the-worse-one-147235" target="_blank" rel="noopener noreferrer">In one academic study</a>, 23% of people who were given just two plans to choose from picked the one that left them worse off financially. Of insured adults, <a href="https://usafacts.org/articles/how-many-people-skip-medical-treatment-due-to-healthcare-costs/" target="_blank" rel="noopener noreferrer">25%</a> skipped medical care due to cost. As one consumer said, “With the number of healthcare insurance options out there, the process of picking and choosing can feel overwhelming, but AI can help to alleviate that burden.”</p> <p>Index scores are even higher for health monitoring, which falls just two points below the global average. This is likely due to the wide range of monitoring technologies available, from wearables that measure heart rate to specialized devices for blood pressure, glucose levels and even heart abnormalities. AI instills confidence in consumers looking for the optimal product to meet their specific needs.</p> <h6><b>Older consumers are the biggest AI enthusiasts at this stage</b></h6> <p>Older generations are significantly more inclined than younger ones to use AI and digital technologies, such as their mobile phones, to learn about health insurance products.</p> <p>For example, in prescription drugs, the score for consumers aged 55+ exceeds that of the youngest cohort (18–24) by more than 20 points.<b> </b>This could be due to the fact that, according to the <a href="https://www.cdc.gov/nchs/hus/topics/rx-drug-use.htm#explore-data" target="_blank" rel="noopener noreferrer">CDC,</a> less than 40% of consumers between the ages of 18 and 44 take at least one prescription, compared with over 80% of those aged over 65.</p> <p>In health monitoring, the gap between the oldest and youngest consumer cohorts is 22 points. While younger consumers are more likely to own wearable devices overall, health monitors are more prevalent among older individuals. As such, older consumers are more likely to have weathered the challenges of finding the best solution for their needs and are searching for a change.</p> <p>Furthermore, in the insurance industry, most consumers 55 and older are shopping for Medicare plans. These enrollments are often facilitated by both brokers and agents on an annual basis. However, notable trends have emerged, with increased investment focused on transitioning individuals from commercial to Medicare plans. In these scenarios, the primary goal is retention, which is an area where AI has enhanced various processes.</p> <h6><b>Conversational AI leads the charge</b></h6> <p>Conversational AI is the overwhelming tool of choice across all age groups in all four product categories. The versatility of the tool allows for explorative exchanges regarding health and insurance plan options. The tool can take the patient's personal information into consideration in its responses, far surpassing the generalized, one-size-fits-all capabilities of traditional searches. </p> <p>For example, conversational AI tools, such as HealthBird, can provide guidance on the best insurance plan option, taking into account personal information such as income, health conditions, anticipated coverage needs, prescriptions and preferred doctors.</p>

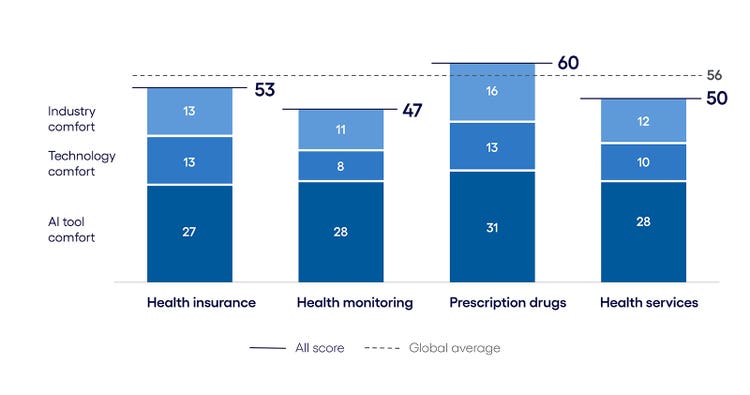

<h5><b>The Buy phase: Interest in health insurance AI is low—except for prescription drugs</b></h5> <ul> <li><span class="eds-label">Top AI enthusiasts are consumers aged 25–34</span><br> <br> </li> <li><span class="eds-label">Prescription drugs see the highest AI uptake</span><br> <br> </li> <li><span class="eds-label">AI voice assistants are the tool of choice at this stage</span></li> </ul> <p>In health insurance, most employers offer a limited selection of plans, though coverage levels can still vary widely. At the same time, the majority of consumers actively shopping for insurance are typically seeking government-sponsored plan options or those available through the Affordable Care Act (ACA). </p> <p>In either case, decisions in the Buy phase can range from high-stakes choices with lasting and costly implications, like selecting an insurance plan, to administrative tasks, such as scheduling an appointment after learning about a service or managing a medication purchase after a doctor’s prescription.</p> <p>Scores in all three components of the index are much lower in Buy than in Learn, especially the technology comfort component, which drops 18 points. This indicates a historical reluctance to use digital technologies like smartphone apps for final health insurance transactions. Unlike in retail and other industries where purchase decisions are reversible, consumers are more reluctant to use technology for these decisions.</p> <p>Industry comfort is also lower, showing discomfort with sharing personal health information with AI tools. As one consumer noted, "AI might be as secure as the companies I share info with today, but it requires a leap of faith to share the same with AI."</p> <p>However, as with the Learn phase, attitudes differ across consumer age groups and product categories, particularly for prescription drugs.</p> <p><b>Health insurance AI Inclination Index: The Buy phase</b></p>

#

<p><span class="small">Figure 3<br> Base: 8,451 respondents in the US, UK, Germany and Australia<br> Source: Cognizant Research </span></p> <h6><b>Top AI enthusiasts are consumers aged 25–34</b></h6> <p>Unlike in the Learn phase, it’s younger consumers (25–34) who are most apt to use AI to buy health insurance products and services. This trend is particularly true for monitoring devices, where this age group's index score surpasses the 55+ cohort by 16 points and the 18–24 age group by 20 points. </p> <p>This dynamic may be due to the prevalence of smart wearable devices among consumers in this age group. In <a href="https://www.coolest-gadgets.com/apple-watches-statistics/" target="_blank" rel="noopener noreferrer">one recent study</a>, people aged 25–34 were the largest cohort of Apple SmartWatch users, with nearly one-third owning such a device. </p> <p>A similar disparity appears in the insurance plan product category. Here, younger consumers may be less experienced with the negative ramifications of choosing an unsuitable plan and thus more trusting of AI. Additionally, because they were the first to grow up in a digital world, they are naturally more comfortable with making purchases in this way.</p> <h6>Prescription drugs see the highest AI uptake</h6> <p>Prescription medication is the only health insurance product category to rank higher on the AI Inclination Index during the Buy phase than the global average. This is likely due to the frustrations consumers can encounter with purchasing prescription drugs. <a href="https://healthpolicytoday.org/2024/01/24/insurers-drop-coverage-for-more-than-600-drugs/" target="_blank" rel="noopener noreferrer">One in three</a> Americans with health insurance will be prescribed a medication this year that their insurer won’t cover. Insurers are also adding new controls, such as step therapies, creating additional hurdles for patients to navigate. </p> <p>Because of process gaps, consumers often have to make multiple phone calls to the pharmacy, healthcare provider and payer to close loops in prior authorizations or denials or to understand pricing. For example, one <a href="https://static1.squarespace.com/static/5c326d5596e76f58ee234632/t/650924780b6b9c590edfa2b4/1695097983750/Unravelling\_the\_Drug\_Pricing\_Blame\_Game\_3AA\_APCI\_0923.pdf" target="_blank" rel="noopener noreferrer">study</a> cites that a single drug purchased at the same retail pharmacy was calculated at five different prices during a single day.</p> <p>Delays in filling prescriptions can impact treatment effectiveness and have long-term negative implications on both health outcomes and insurer costs. AI could work on the consumer’s behalf to help troubleshoot, overcome or at least explain and provide updates on process gaps and ensure prescriptions are filled promptly, at the right dosage.</p> <h6>AI voice assistants are the tool of choice at this stage </h6> <p>AI voice assistants achieve their highest scores during the purchase phase, particularly for prescription drugs. This differs from the Learn phase, where conversational AI takes the lead. This is likely because the purchase phase is oriented toward quick transactions, such as confirming orders and clarifying quantities, or setting delivery preferences.</p> <p>This technology is seeing some uptake. A <a href="https://www.supermarketnews.com/health-wellness/giant-eagle-pharmacy-patients-can-now-ask-alexa" target="_blank" rel="noopener noreferrer">collaboration</a> between Amazon, medication management specialist Omnicell and regional pharmacy Giant Eagle allows patients to use their voice assistant to issue prescription refill requests. Through a voice prompt, requests are met using the patient’s prescription information at the pharmacy, which promises to increase convenience and accuracy.</p>

<h5><b>The Use phase: Health insurance complexity evens the AI playing field</b></h5> <ul> <li><span class="eds-label">All age groups have a surprisingly similar AI attitude at this phase </span><br> <br> </li> <li><span class="eds-label">Monitoring devices exceed the global average for AI inclination </span><br> <br> </li> <li><span class="eds-label">Technology comfort levels remain low</span></li> </ul> <p>During the Use phase, consumers are trying to navigate insurance plan claims, stick to a treatment plan, optimize medication intake times and set up their monitoring device. These post-sale activities are often open for interpretation; hence, it’s where AI has the potential to offer support on making products and services work more effectively.</p> <p>This is why index scores, especially for older demographics, show a slight uptick in the Use phase from the Buy phase, particularly for monitoring devices, where index scores surpass the global average (see Figure 4). </p> <p>In other product categories, like prescription drugs and insurance plans, consumers are less inclined to see the value of injecting AI. And as with other consumer journey phases, there are big differences among consumer groups.</p> <h6><b>Health insurance AI Inclination Index: The Use phase</b></h6>

#

<p><span class="small">Figure 4 <br> Base: 8,451 respondents in the US, UK, Germany and Australia <br> Source: Cognizant Research</span></p> <h6><b>All age groups have a surprisingly similar AI attitude at this phase</b></h6> <p>Unlike<b> </b>the big variances in Learn and Buy, there are smaller peaks and valleys among consumer cohorts during the Use phase, especially for health insurance, prescription drugs and health services.</p> <p>Within these three product categories, scores for individuals aged 55+ are only three to six points higher than those of the youngest and lowest scoring cohort, aged 18–24. This is, on average, 65% lower than the variation between the oldest and youngest cohorts in Learn.</p> <p>As such, the Use phase is a common ground for how consumers see AI helping them navigate their insurance product or services, whether for the first time or as their healthcare needs evolve over their lifetime. This commonality highlights a unified view of the difficulty that all patients face in navigating their health insurance needs.</p> <h6><b>Monitoring devices exceed the global average for AI inclination</b></h6> <p>Consumers overwhelmingly see the value of AI aiding in their use of monitoring devices, with index scores surpassing the global average. This could be due to the increased sophistication of health monitoring devices and their growing role in health insurance.</p> <p>Over <a href="https://www.health.harvard.edu/staying-healthy/whats-the-future-of-remote-patient-monitoring" target="_blank" rel="noopener noreferrer">50 million Americans</a> currently use remote patient monitoring devices for various health and wellness purposes and chronic conditions. AI can satisfy a myriad of use cases that can boost treatment adherence, such as alerts and reminders through wearable devices, and even early detection of health issues.</p> <p>Additionally, utilizing these devices could help consumers engage with <a href="https://www.thinkbiosolution.com/wp-content/uploads/2020/01/TBS\_business\_whitepaper\_20191201\_Using\_RPM\_To\_Underwrite\_health\_insurance.pdf" target="_blank" rel="noopener noreferrer">interactive insurance policies</a> that reward premium discounts for reaching fitness targets. As one consumer noted, “AI could serve as my healthcare center, where I obtain personal health information, identify issues quickly, and assist me on my health journey.”</p> <h6><b>Technology comfort remains low</b></h6> <p>As in the Buy phase, consumers’ comfort with trying the latest technology is low, especially for insurance plans and prescriptions. Here, the stakes are similarly high for consumers. Whether it’s misinformation on plan claims or mistakes on acceptable use of medications generated by chatbots, consumers could imagine AI inviting negative monetary and health outcomes.<br> <br> This could be due in part to consumer backlash against insurers using AI to make coverage decisions, resulting, in some cases, in improper <a href="https://journalistsresource.org/home/ai-in-the-health-insurance-industry-explainer-and-research-roundup/" target="_blank" rel="noopener noreferrer">denial of coverage</a>.<br> <br> On the other end of the spectrum, this raises important questions about medical liability as AI becomes increasingly integrated into areas such as drug selection, dosage recommendations and personalized treatment plans. These advancements introduce challenges in determining accountability for AI-driven decisions, creating ambiguity around whether responsibility lies with developers, healthcare providers or the institutions deploying the technology. This underscores the need for strategically placed controls and checkpoints as the technology continues to evolve.</p>

<h4>Meeting consumers where they are in the health insurance journey</h4> <p>Consumer use of AI is growing fast and, with it, the emergence of consumer AI agents. These AI agents will act like a personal digital concierge, orchestrating complex tasks across the purchase journey. Soon, the internet as we know it today will become the agentic internet: an interconnected ecosystem of AI-enabled tools and agents that autonomously locate, evaluate, purchase and maintain the products and services they rely on. </p> <p>While consumer AI uptake may be slightly below the global average for consumers of health insurance products and services, we believe leaders have less than five years to navigate this change. </p> <p>To prepare for the AI-driven consumer era ahead, healthcare payers will need to rethink how they operate across these four key areas:</p> <ul> <li><b>Integrate AI agents across health insurance products under the wider provider umbrella. </b>Together, health monitoring, health services, prescription drugs and health insurance AI agents will have enough information to build a comprehensive view of a patient’s overall health profile. Moving forward, it will be essential to ensure interoperability and seamless communication between these agents under the provider umbrella. Not only will it provide a more robust understanding of one’s health than any single agent alone, but it will also help to prevent data fragmentation.<br> <br> For example, presenting this information in a unified view, as demonstrated by Blue Cross Blue Shield’s <a href="https://news.blueshieldca.com/2024/06/26/your-health-in-the-palm-of-your-hand-blue-shield-of-california-is-reimagining-health-record-access" target="_blank" rel="noopener noreferrer">Member Health Record</a> app, highlights the potential of such networks to empower patients with a clearer understanding of their health insurance plan and making it easier to manage their healthcare moving forward.<br> <br> </li> <li><b>Prioritize trust-building. </b>Many consumer reservations are centered around fears of data misuse, especially in the health monitoring arena, where they fear sensitive health information could be levied against them. Healthcare payers need to ensure transparency in AI data usage and prioritize security of personal health data to build consumer trust.<br> <br> They can do this by clearly communicating how consumer data will be used, stored and protected, and provide options for consumers to control what their data is used for. By clearly delineating the line of accountability when it comes to AI acting on a consumer’s behalf, payers can further make consumers feel more secure using AI technologies where mistakes can occur. Fears of being held accountable for AI’s missteps, especially regarding payments, creates significant pause.<br> <br> An example of this, based on the analysis presented in our recent report “<a href="https://www.cognizant.com/en\_us/industries/documents/the-billion-dollar-question-for-health-insurers-and-generative-ai.pdf" target="_blank" rel="noopener noreferrer">The Billion-Dollar Question for Health Insurers and Generative AI</a>,” is appeals and grievances (A&G) processing. This space has seen significant streamlining across various tasks, including initial case intake, policy matching to claims events, and coordination with both internal and external stakeholders. These time-saving capabilities can enhance the overall member experience and enable A&G experts to serve members more efficiently.<br> <br> </li> <li><b>Focus on enhancing low-stakes, high-reward aspects of consumers’ lives.</b> Health insurers should familiarize consumers with the benefits of using AI tools in low-stakes, high-reward situations, such as insurance plan recommendations, scheduling routine appointments based on health monitoring data, and requesting prescription refills. Doing so can build trust while the technologies of tomorrow have time to develop.<br> <br> It is important to exercise caution in the rollout of AI-powered health insurance tools, as consumers and lawmakers alike expect fail-proof solutions, especially when it comes to pharmaceuticals and monitoring devices.<br> <br> </li> <li><b>Balance AI integration with fair treatment.</b> Businesses must understand that they, and the technological advancements they implement, hold ethical obligations to ensure the fair treatment and diligent consideration of patients' needs within the systems they seek care. This responsibility is underscored by the need for robust regulatory frameworks to safeguard privacy, security and integrity. For many businesses, AI has the potential to expedite processes, but as they are finding, there are certain touchstones in the journey that are worth the time.</li> </ul>

Jump to a section

Introduction #spy-1

AI across the health insurance journey #spy-2

subnav- The Learn phase: Information overload drives AI interest in health insurance#spy-3

subnav- The Buy phase: Interest in health insurance AI is low—except for prescription drugs#spy-4

subnav- The Use phase: Health insurance complexity evens the AI playing field#spy-5

Meeting consumers where they are in the health insurance journey #spy-6

<h5>Authors</h5>