Banking and capital markets: building on today’s successes to address the future styles-h2 text-white

<p><span class="medium"><br>September 12, 2022</span></p>

Banking and capital markets: building on today’s successes to address the future

<p><b>After years of modernizing, banks, asset managers and financial intermediaries have more to do, especially in the areas of core modernization, personalization and rethinking the operating model.</b></p>

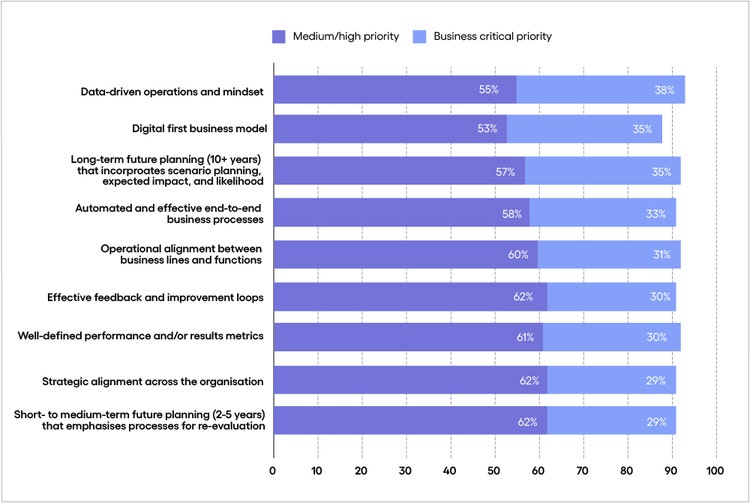

<p>The banking and financial services industry has made visible progress in its efforts to modernize. But in the face of tighter regulation and lingering reputational damage—scars from the 2008-2009 financial crisis—as well as increased competition from tech-savvy, client-obsessed fintechs, there’s more to do. </p> <p>The rise of the environmental, social and governance (ESG) agenda adds still more pressure on financial institutions to modernize, especially when combined with the industry’s key role in global efforts to tackle climate change, notably through their loan portfolios and capital markets financing.<br> </p> <p>In recent Economist Impact research supported by Cognizant, the banking and capital markets industry ranked fifth of eight in future-preparedness. From advancing core modernization, to boosting personalization, to rethinking their operating models, banks, asset managers and financial intermediaries need to step up their modernization game.<br> </p> <p>Here are insights into where financial institutions stand in terms of future-readiness—and where there is work to be done.<br> </p> <h4>Advance core modernization</h4> <h5><span style="font-weight: normal;">To what extent does your company's corporate strategy prioritize the following?</span></h5> <p><i>(Percentage of respondents rating each strategic imperative as business-critical or high/medium priority.)</i></p>

#

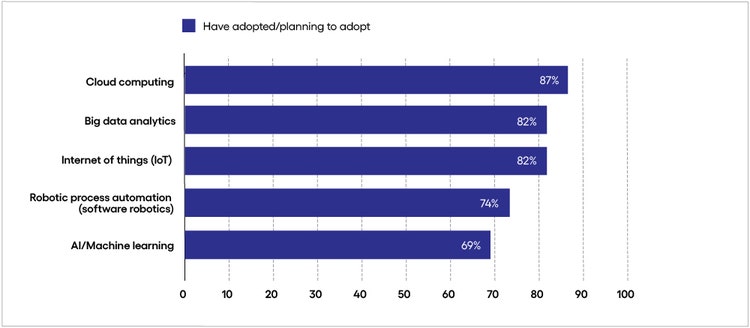

<p><span class="small">Response base: 250 senior executives from the banking and capital markets industry <br> Source: Economist Impact Survey 2022<br> Figure 1</span></p> <h5>What they’re good at </h5> <ul> <li><b>Cloud mastery.</b> Banks have enthusiastically embraced the cloud, and nearly 70% are realizing significant value from their cloud investments.<br> <br> Replacing legacy operations with cloud-based and open-banking solutions is a key feature of core modernization. Although cloud migration can be a complex endeavor requiring tailored solutions, banks that have undertaken it are benefiting from operational efficiencies, cost reductions, artificial intelligence (AI) enablement, superior employee experience and built-in automation capabilities leading to shorter time-to-market.</li> </ul> <h5>Long way to go<br> </h5> <ul> <li><b>Getting executive buy-in.</b> Core services modernization is not easy for financial services organizations. For universal banks—those that provide retail, commercial and investment banking services under one roof—it often means evolving from monolithic systems serving all core banking functions, to a more agile, cloud-based infrastructure in which functions such as customer master data management, liquidity management and payment initiation and execution are dealt with separately.<br> <br> But only about 40% of executives report strong leadership support for modernization efforts, and just under 30% say cross-organizational strategic alignment is a business-critical priority for their companies.</li> </ul> <h5>The importance of bridging the gap<br> </h5> <ul> <li><b>Strategic alignment requires top leadership support.</b> Core services modernization is a highly complex transition demanding strong, long-term support from leadership and deep alignment throughout the company. Without it, modernization efforts will not reach their potential, and new offerings will lag.<br> <br> </li> <li><b>Clients’ evolving needs must be met.</b> Increasingly tech-savvy clients who have grown accustomed to the seamless experiences provided by fintechs have ever-rising expectations. Personalized, omnichannel services will remain vital for the next generation of banking customers, who quickly adopt new ways of banking, investing and paying for goods and services, such as through social media apps that act as payment processing gateways.<br> <br> Having a modernized core is crucial to not just detecting these new behaviors and preferences but also providing the services next-gen consumers expect at scale.<br> <br> </li> <li><b>Modernization ensures robust processes and resilient operations.</b> A modernized core supported by cloud, big data analytics and cutting-edge AI technology lowers costs, underpins robust processes and adds resilience to the company’s operations—an especially important feature in a risk-plagued environment.<br> <br> Forward-thinking financial institutions, for example, are using AI to process vast amounts of transactional information to fortify sound loan management decisions or detect fraud. The technology can also collect and analyze data from multiple sources, including mobile apps, and generate insights to lower costs, speed processes, boost revenue and drive resilience.<br> </li> </ul> <h4>Boost personalization</h4> <h5><span style="font-weight: normal;">Which of the following technologies and/or methodologies has your business department adopted, or is planning to adopt?</span></h5> <p><i>(Percentage of respondents who have adopted or are planning to adopt.)</i></p>

#

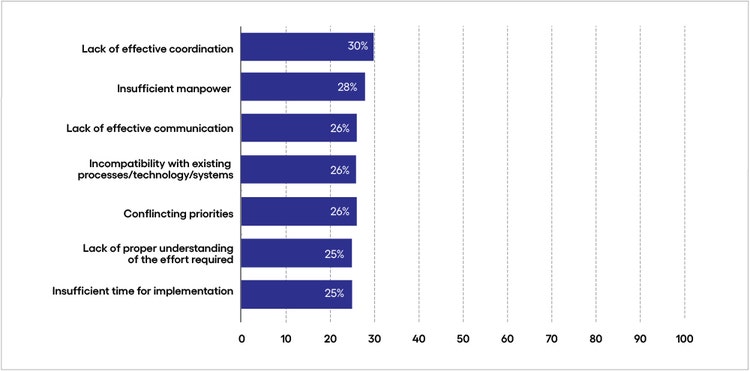

<p><span class="small">Response base: 250 senior executives from the banking and capital markets industry<br> Source: Economist Impact Survey 2022<br> Figure 2</span></p> <h5>What they’re good at</h5> <ul> <li><b>Embracing the right tech for personalization.</b> Personalization can profoundly transform customer relationships. It means moving from generalized demographic segmentation to catering to individual needs, better anticipating these needs and building solid relationships with clients.<br> <br> This starts with adopting the technologies that allow financial institutions to translate data generated in client interactions through all different touchpoints into data-informed insights and actions. The financial services industry shows an appetite for this, with 82% of companies having adopted or planning to adopt big data analytics (and 69% in the case of AI/machine learning).</li> </ul> <h5>Long way to go<br> </h5> <ul> <li><b>Realizing value for their personalization investments.</b> Banks, asset managers and financial intermediaries can do more to extract value from their investments in personalization-enabling technology. For example, while 60% of those that have adopted big data analytics are seeing significant value from it, this figure drops to 40% for AI/machine learning.<br> <br> To fully realize their potential, companies in the industry need to build analytics- and AI-generated insights into their decision-making flows, and use them to generate hyper-personalized experiences across every touchpoint, whether human- or technology-enabled.</li> </ul> <h5>The importance of bridging the gap<br> </h5> <ul> <li><b>Building long-term relationships with clients.</b> It has never been easier for customers to switch to a new financial services organization. By enabling companies in the industry to understand the needs of individual clients, data-based personalization helps them build a long-lasting relationship and superior brand appeal. It also gives them the tools needed to nudge their clients to make more sustainable investment and purchasing decisions.<br> <br> </li> <li><b>Creating new products and services.</b> With deeper insight into their clients’ preferences, financial services organizations can develop innovative products and services ahead of the competition and increase their market share.<br> <br> For example, they can use ongoing data collection to deliver dynamic experiences on their mobile apps that change in step with customers’ unfolding behaviors and desires. When new data arrives—whether through a banking interaction or a lifecycle event discovered from an external data source—the application code could automatically adapt the experience.<br> <br> A simple example would be a banking app that notes that the customer always checks their credit card balance first and automatically personalizes the experience by displaying the balance front-and-center on the app’s home page.</li> </ul> <h4>Rethink the operating model</h4> <h5><span style="font-weight: normal;">Which of the following were the most significant challenges for your business department when implementing new processes, products, services and technologies in the past year?</span></h5> <p><i>(Percent of respondents selecting each challenge. Select up to five.)</i></p>

#

<p><span class="small">Response base: 250 senior executives from the banking and capital markets industry <br> Source: Economist Impact Survey 2022<br> Figure 3</span></p> <h5>What they’re good at </h5> <ul> <li><b>Gathering data to drive decisions.</b> Over the last two decades, financial institutions have done a good job of centralizing the management of key functions and services (such as finance, risk management, client-centric design and procurement) at the enterprise level. This has led to significant savings and allowed different business areas to make more informed decisions thanks to data availability.<br> <br> </li> <li><b>Distributed work models.</b> Even before the pandemic, financial institutions had become adept at working in a highly distributed environment, which proved crucial to keeping business running smoothly when COVID struck. Now, the vast majority (88%) of respondents say their organization offers employees the ability to work from home (at least some days per week) and/or at alternative times.<br> </li> </ul> <h5>Long way to go<br> </h5> <ul> <li><b>Realizing operational efficiencies.</b> An important step to make progress in these areas is to handle more services—such as data management and environmental impact compliance—at the enterprise level.<br> <br> Clearly, it makes sense to manage some areas at the function level; for example, personalization initiatives and client experience and touchpoint management are specific initiatives better left to the business functions that understand them well. For most others, however, an operating model that concentrates activities at the enterprise level will be far more efficient.<br> </li> <li><b>Coordination and staffing. </b>The main challenges identified by survey respondents reveal un unsettling picture of poor coordination, ineffective allocation of human and technological resources, and deficient management. For example, 30% of respondents identify lack of effective coordination as one of their companies’ top challenges, and almost as many points to a lack of skilled people as a substantial hurdle. <br> </li> </ul> <h5>The importance of bridging the gap<br> </h5> <ul> <li><b>Responding swiftly to change.</b> By managing more initiatives at the enterprise level and also investing in a culture of cross-departmental collaboration, financial institutions can respond more quickly to change, be it regulatory or market-driven. In an increasingly fast-paced market, in which fintechs and established competitors display the cultural DNA of dynamic startups, this is a crucial step for banks to remain relevant in the medium to long term.<br> <br> </li> <li><b>Scaling up sustainability efforts.</b> Through their lending, borrowing, investing and payments practices, financial institutions can also serve as the heart of the massive economic transformation needed to move away from fossil fuels and achieve a net-zero world. There is ample opportunity, for example, to offer new, “green” investment vehicles, such as credit cards, loans and accounts that promise to lower carbon footprint and reduce emissions.<br> <br> The pressure is also on to identify risks associated with portfolio emissions and use climate-based assessment as part of the criteria to direct investments or make lending decisions. All of this can only be achieved with an efficient operating model.</li> </ul> <p><i>To learn more, visit the <a href="/content/cognizant-dot-com/us/en/insights/modern-business.html" target="_blank" rel="noopener noreferrer">Modern Business</a> section of our website or <a href="/content/cognizant-dot-com/us/en/about-cognizant/contact-us.html" target="_blank" rel="noopener noreferrer">contact us</a>.</i></p> <p><i>The views and opinions expressed in this report are those of Cognizant and do not necessarily reflect the view and policies of Economist Impact. Data presented is from an Economist Impact executive survey, commissioned by Cognizant, conducted in early 2022.</i></p> <p><i>This article was written by Sanghosh Bhalla, Digital Banking Consulting Partner, Robert Benyo, Risk & Compliance Solution & Platform Architect in Cognizant’s Banking and Financial Services practice, and Eduardo Plastino, Director in Cognizant Research.</i><br> </p>

<p>We’re here to offer you practical and unique solutions to today’s most pressing technology challenges. Across industries and markets, get inspired today for success tomorrow.</p>