RESEARCH

What consumer preferences reveal about AI adoption in banking and finance

<p><br> <span class="small">July 03, 2025</span></p>

What consumer preferences reveal about AI adoption in banking and finance

<p><b>Our AI Inclination Index reveals which consumers are most open to using AI in the banking and financial services purchase journey—as well as where and how they’ll use it. Knowing this, banking organizations can develop an effective consumer-facing AI strategy.</b></p>

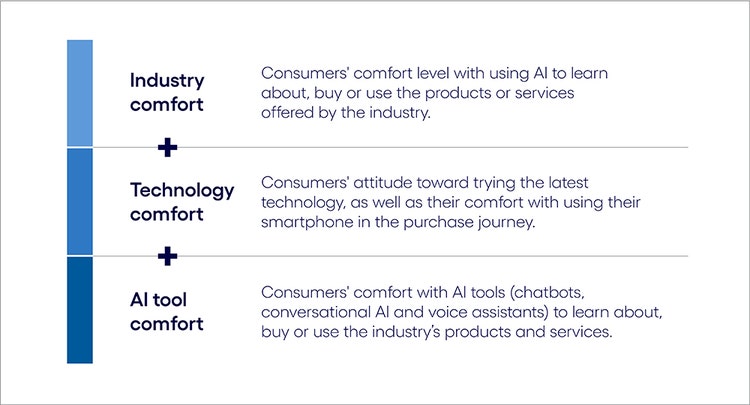

<p>Banking products and services often overwhelm consumers with their complexity. Whether it's selecting the right credit card or investment from a sea of options or deciphering the fine print on a loan agreement, the banking journey can feel daunting and opaque. </p> <p>AI could play a big role in cutting through the confusion and empowering consumers to make confident financial decisions. But which consumers are most (and least) inclined to use AI? Which tool would they prefer to use? And where in the purchase process would they be most comfortable using it?</p> <p>Our recent research uncovered some nuanced answers to those questions. Using data from <a href="https://www.cognizant.com/us/en/aem-i/new-minds-new-markets-ai-customer-experience" target="_blank" rel="noopener noreferrer">our recent consumer AI study</a>, we developed the AI Inclination Index, which quantifies consumers’ propensity to use AI (see explainer box below). </p> <p>While the index reveals a lower inclination to use AI when purchasing banking and financial services products than other industries’ products and services (see Figure 1), that broad finding masks important variations.</p> <p>Consumers’ comfort levels differ dramatically across the three key phases of the consumer journey (Learn, Buy and Use) and the five banking and financial services product categories in our study: </p> <ul> <li>Deposit accounts (checking, savings accounts) </li> <li>Digital payments (payment apps, digital wallets) </li> <li>Credit cards </li> <li>Loans (personal, auto, mortgage, business and student loans) </li> <li>Investments (stocks, bonds, funds, ETFs, retirement accounts) </li> </ul> <p><b>Consider these metrics about AI adoption in banking:</b></p> <ul> <li><b>Financial consumers are most apt to use AI at the beginning of the purchase journey: the Learn phase.</b> However, interest tapers off during the purchase and post-sale Use phases, particularly for more complex financial products like loans.<br> <br> </li> <li><b>AI inclination levels shift dramatically across consumer age groups and buying phases.</b> While the highest levels of AI interest are among consumers aged 45–54 in the Learn phase, that shifts to older consumers (55+) in the Use phase. Meanwhile, younger demographics show strong interest in using AI for simpler, mobile-first solutions like digital payments.<br> <br> </li> <li><b>The tool of choice is often conversational AI.</b> Conversational AI consistently receives higher scores than the other two tools in our study: voice assistants and chatbots. Its ability to simplify complex topics, such as guiding users through investment options or helping them compare credit card benefits, can make the Learn phase more accessible and less intimidating. </li> </ul> <p><b>The AI Inclination Index</b></p> <p><i>To quantify consumers' propensity to adopt AI-driven technology features throughout the consumer journey, we developed the AI Inclination Index. The index was calculated using three measures from our New minds, new markets survey data.</i></p>

#

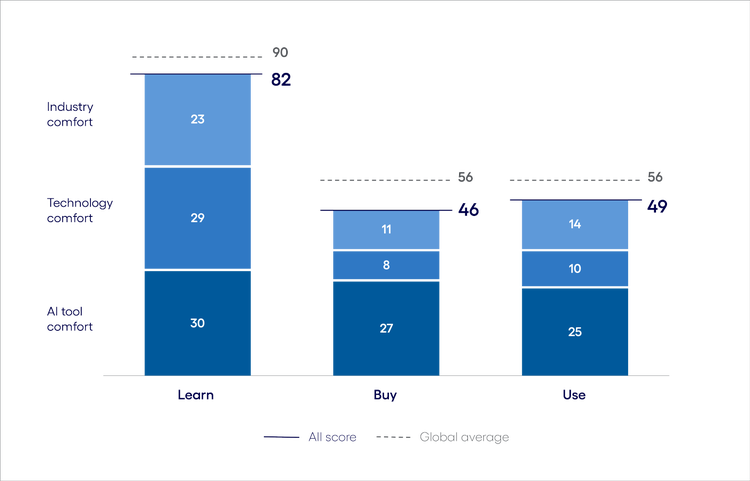

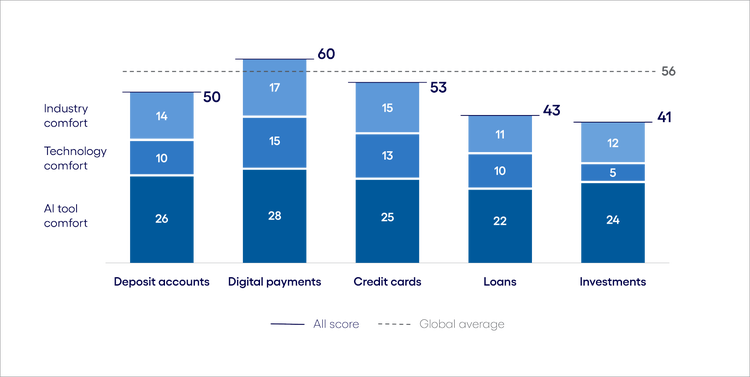

<p> </p> <p><b>AI inclination in banking and financial services vs. the global average</b></p> <p><i>Consumers are somewhat less inclined to use AI when purchasing banking and financial services products than other industries’ goods.</i></p>

#

<p><span class="small">Figure 1<br> Base: 8,451 respondents in the US, UK, Germany and Australia<br> Source: Cognizant Research</span></p>

<p>With these variances, it’s clear banking and financial services businesses will need to craft an AI strategy that captures the greatest areas of opportunity while carefully mitigating the risks associated.</p> <p>This is especially true because of the industry’s demand for 100% accuracy in its customer interactions, which presents a delicate balancing act: The financial sector knows a lot about its customers, but it’s also subject to strict regulation. While AI models are fairly easy to build, the challenge in financial services is to apply them with the most impact and the least risk.</p> <p>Understanding consumer use of AI, as well as the accompanying pockets of spending power, is essential for leaders in all industries. In our global study “<a href="https://www.cognizant.com/us/en/new-minds-new-markets-ai-customer-experience" target="_blank">New minds, new markets</a>,” we found that consumers who are enthusiastic about using AI will account for up to 55% of all purchases made across industries. This amounts to $4.4 trillion in spending in the US, $690 billion in the UK, $690 billion in Australia and $540 billion in Germany.</p> <p>In this report, banking and financial services leaders will learn about where in the purchase journey consumers are most and least inclined to use AI, the AI tools they would be most apt to use and how this differs among consumers across age groups. With this information, businesses can reshape their approach to customer engagement—where and how it matters most. </p>

<h4>AI adoption across the financial consumer journey</h4> <p>As our AI Inclination indicates, financial consumers are less likely than the global average to use AI across all three stages of the banking and financial services consumer journey—Learn, Buy and Use. This disparity is most evident in the Buy phase, where the score is 10 points lower than the global average. </p> <p>A closer analysis, however, reveals an important distinction that serves to pull the score down: the very different dynamics at play between the complex products offered by the tightly regulated banking sector, such as mortgages and loans, and the more innovation-friendly domains of credit cards and investments, often influenced by fintech players. </p> <p>While credit cards and digital investments are more consumer-driven and amenable to AI-driven exploration, traditional products like loans and mortgages require higher trust and involve stricter compliance, which creates hesitation in adopting AI. Our inclination index reflects this, with loans scoring significantly lower on the inclination index than digital payments or credit cards, effectively dragging down the overall sector score. </p> <p>This gap between the digital payments and more traditional banking areas is important to keep in mind as we review how consumers feel about using AI across all five product categories of the banking and financial services industry.</p>

About our analysis

To understand consumer AI behaviors and attitudes at a granular level, we structured our analysis around four key pillars:

- The consumer journey. We studied the specifics of AI use at each phase of the customer journey. This journey—how consumers discover, purchase and engage with products and services before and after a sale—is at the heart of the business-customer relationship.

- Consumer demographics. To gain a better understanding of how consumer attitudes and behaviors differ by age group, we divided consumers into five categories: 18–24, 25–34, 35–44, 45–54, and 55+.

- Consumer AI tools. We defined consumer AI use by asking about their intended use of three key tools that are prevalent in the consumer world: voice assistants, chatbots and conversational AI.

- Industry-specific products. We included five banking and financial services product categories in our analysis: deposit accounts, digital payments, credit cards, loans and investments

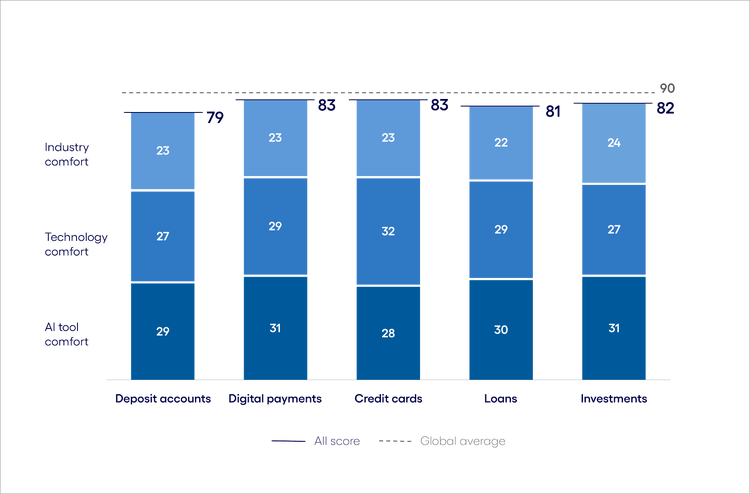

<h5><b>The Learn phase: AI has a place in demystifying complex financial products</b></h5> <ul> <li><span class="eds-label">When it comes to AI in the Learn phase, older consumers rule</span><br> <br> </li> <li><span class="eds-label">AI inclination is highest for learning about credit cards and digital payments</span><br> <br> </li> <li><span class="eds-label">Deposit accounts and loans capture the least AI interest</span><br> <br> </li> <li><span class="eds-label">Conversational AI is the tool of choice</span></li> </ul> <p>The discovery phase is where consumers are most inclined to use AI-enabled tools in banking and financial services. The inclination index score for the Learn phase is 36 points higher than in the Buy phase. While all product categories fall below the global average, digital payments and credit cards rank highest (see Figure 2). </p> <p>As such, the Learn phase represents a prime opportunity for businesses to capture attention and influence decisions. Doing so starts with understanding what consumers value about using AI in this phase and the AI tools they’re most apt to use. </p> <p><b>Banking and financial services AI Inclination Index: The Learn phase</b></p>

#

<p><span class="small">Figure 2 <br> Base: 8,451 respondents in the US, UK, Germany and Australia <br> Source: Cognizant Research</span></p> <h6><b>When it comes to AI in the Learn phase, older consumers rule</b></h6> <p>While our global cross-industry research study revealed higher AI comfort among younger consumers, it’s older generations, particularly those aged 45–54, who are more inclined to use AI to learn about all five banking and financial services product categories.</p> <p>Many people in this age group are intensive users of banking products and services, as they are often balancing not just their own financial needs but also those of their children and aging parents. As such, they are likely to see the value of using AI to learn about available options.</p> <p>The largest gap between consumer age groups is in the loans market. Here, the score for the 45–54 cohort exceeds the youngest cohort (18–24) by 20 points. This is likely due to younger consumers’ limited financial experience and lower borrowing needs. A <a href="https://www.experian.com/blogs/ask-experian/research/consumer-debt-study/" target="_blank" rel="noopener noreferrer">study by Experian</a> revealed that Generation X (consumers aged 44–59) carried the largest total debt balance in 2024 despite being a smaller demographic group than either millennials or baby boomers.</p> <p>That said, the core banking products that younger consumers are more likely to engage with see inclination scores reach higher levels. Deposit accounts, for example, see just a two-point gap between 18-to-24-year-olds and 45-to-54-year-olds, with scores of 60 and 62 points, respectively. There’s a similarly small three-point gap between both groups for credit cards—at 63 and 66, respectively.</p> <h6>AI inclination is highest for learning about credit cards and digital payments</h6> <p>The overwhelming variety of credit card options—each with its own rewards programs, interest rates and fees—can make decision-making complex. According to <a href="https://nilsonreport.com/articles/payment-cards-projected-worldwide-6/" target="_blank" rel="noopener noreferrer">Nilson</a>, there are about 17.45 billion credit, debit and prepaid cards in circulation worldwide; in the US, according to <a href="https://www.experian.com/blogs/ask-experian/average-number-of-credit-cards-a-person-has/" target="_blank" rel="noopener noreferrer">Experian</a>, the average consumer has 3.9 credit cards. As one consumer in our study said, “There is a lot of information out there about different financial services products, and I feel like AI can really cut through a lot of that noise.”</p> <p>Meanwhile, AI is already deeply embedded in digital payment experiences. The widespread adoption of mobile wallets, contactless payments and online platforms have normalized AI-driven mechanisms. Digital payment transactions are also generally smaller-scale and less consequential, which lowers consumers’ perception of risk and increases their willingness to embrace AI.</p> <h6>Deposit accounts and loans capture the least AI interest</h6> <p>Deposit accounts have the lowest index score in the Learn phase, largely due to the commodity-like nature of these products. Because the financial attachment and risk are relatively low, consumers see little need for extensive AI-driven research, relying instead on bank websites or comparison tools.</p> <p>By contrast, consumers approach loans with far greater scrutiny. With their complex terms, long-term financial commitments and potential risks, consumers are more likely to turn to trusted sources like bank representatives, financial advisors and independent comparison platforms. </p> <p>AI's effectiveness in loans is also often constrained by the intricate nature of financial data and strict regulations surrounding its use. For example, <a href="https://www.fca.org.uk/publications/research-notes/credit-where-credit-due-how-can-we-explain-ai-role-credit-decisions-consumers" target="_blank" rel="noopener noreferrer">the UK’s Financial Conduct Authority (FCA)</a> is actively exploring the implications of AI-driven credit decisions on consumer outcomes, underscoring the careful experimentation required in this space. As one consumer noted, “AI could potentially provide misinformation when reviewing a person’s data for mortgages and not take important context into consideration.”</p> <h6>Conversational AI is the tool of choice</h6> <p>Conversational AI can replicate the kind of nuanced guidance consumers typically seek from a financial advisor. Unlike static comparison tools or predictive models, it provides a two-way dialogue, allowing consumers to ask follow-up questions, refine their search and receive tailored explanations in real time.</p> <p>If a first-time borrower asked conversational AI for assistance with understanding their mortgage options, AI could evaluate the user’s financial profile, suggest the most appropriate loan types, offer advice on repayment strategies and even recommend alternative plans if the original choice doesn’t align with the user’s financial goals or circumstances. </p>

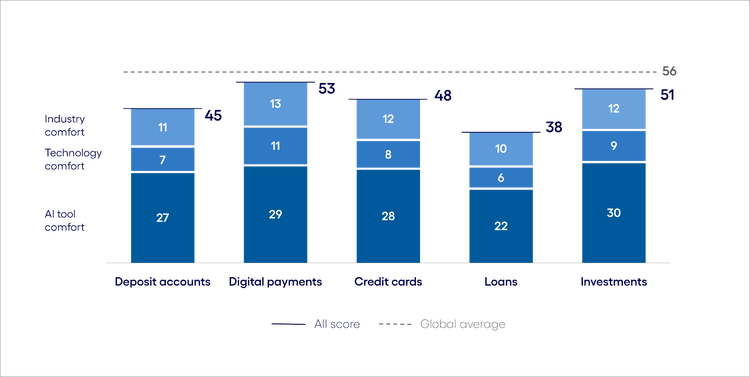

<h5><b>The Buy phase: As financial stakes increase, consumers are less likely to close a deal using AI</b></h5> <ul> <li><span class="eds-label">AI interest tracks with life priorities</span><br> <br> </li> <li><span class="eds-label">Digital payments see the highest AI uptake</span><br> <br> </li> <li><span class="eds-label">Loans lag behind</span><br> <br> </li> <li><span class="eds-label">The AI tool of choice depends on transaction type</span></li> </ul> <p>The Buy phase is where we saw the most hesitation to use AI. Scores in all three areas of the index are lower than in the Learn phase, particularly the technology comfort component, which drops an average of 20 points between the phases. This indicates an historic inability or unwillingness to use digital technologies such as smartphone apps to buy a range of financial products.</p> <p>Industry comfort is also lower across the board, demonstrating a particular squeamishness about using AI to purchase financial products and services. As one consumer argued, “I am very protective over my finances, so definitely unsure on allowing AI to buy financial services products.”</p> <p>In practice, consumers of financial products emphasize the importance of trust at this stage of the journey, with a clear view that the “human touch” is more reliable than algorithms and analytics—or specifically, that it offers the greatest psychological comfort when discussing pension plans, investment strategies and college funds.</p> <p>However, as with the Learn phase, attitudes differ across consumer age groups and product categories.</p> <p><b>Banking and financial services AI Inclination Index: The Buy phase</b></p>

#

<p><span class="small">Figure 3 <br> Base: 8,451 respondents in the US, UK, Germany and Australia <br> Source: Cognizant Research</span></p> <p><b>AI</b> <b>interest tracks with life priorities</b></p> <p>In the Buy phase, interest in AI is spread evenly across the 25–54 age range, with specific patterns emerging across product categories.</p> <p>For example, in investments, the 35–44 cohort outpaces the 45–54 group by 13 points and the 55+ cohort by 24 points.<b> </b>This could reflect the priorities of the 35–44 demographic, who are in their peak earning years and actively seeking to grow wealth through AI-powered insights.</p> <p>The 45–54 cohort shows strong performance in categories like loans, where their score edges out younger groups. This aligns with their stage in life, often characterized by substantial financial commitments, such as mortgages, business investments and education costs, where AI offers convenience and efficiency. They may also be old enough to recognize the inefficiencies of traditional borrowing methods but young enough to trust AI-driven processes.</p> <p>Younger consumers aged 18–24 trail behind across most categories. Their lower scores, particularly in loans and credit cards, reflect limited financial experience and less immediate need for complex products. However, their interest in digital payments suggests that familiarity with mobile-first solutions is fostering early adoption.</p> <p><b>Digital payments see the highest AI uptake</b></p> <p>Digital payments, at just 3 points below the global average, stand out as the strongest-performing product category during the Buy phase. Consumers are very familiar with AI working behind the scenes to enhance the convenience and security of digital payments, such as the real-time fraud detection mechanisms that flag unusual activity on purchases made with payment apps like PayPal or Apple Pay.</p> <p>Unlike more complex products, such as loans or investments, digital payments are part of consumers' everyday routines, making them more comfortable with relinquishing certain decisions to AI. For instance, AI could suggest preferred payment methods tailored to a user's habits.</p> <p>Moreover, AI plays a crucial part in improving security and speed, two factors that have historically created friction for users in financial transactions. Consumers appreciate how AI-powered systems detect suspicious activities, such as unusual spending patterns, and prevent fraud before it occurs. These advantages align with the expectations of consumers seeking a reliable and efficient buying experience.</p> <p><b>Loans lag behind</b></p> <p>Loans, meanwhile, lag with the lowest overall score and fall 18 points below the global average. This reflects consumer skepticism about entrusting high-stakes decisions to AI, particularly when committing to a specific loan product and finalizing the agreement. As one consumer said, “There is a lot of money at stake for bad advice and bad decisions.” Another emphasized that “any technical issue with AI could affect a genuine customer. Again, sometimes financial matters need a human touch.”</p> <p>These concerns highlight broader challenges with AI making loan decisions, including the need for expansive datasets to train AI models, the risks of algorithmic bias and the need for explainable outcomes to meet regulatory transparency standards.</p> <p>This is particularly critical given the estimated <a href="https://www.weforum.org/stories/2024/07/why-financial-inclusion-is-the-key-to-a-thriving-digital-economy/#:\~:text=The%20World%20Bank%20estimates%20that,in%20the%20global%20financial%20landscape." target="_blank">1.4 billion unbanked individuals worldwide</a> who lack traditional credit profiles and won’t appear on credit bureau reports. Lenders who exclusively rely on these datasets risk excluding these customers from the financial system.</p> <p><b>The AI tool of choice depends on transaction type</b></p> <p>Preferences for AI tools vary across product categories. Digital voice assistants take the lead for deposit accounts, reflecting consumer interest in quick, straightforward responses to account-related queries. In contrast, conversational AI dominates digital payments and credit cards, with scores exceeding those of the other two AI tools combined. This could stem from its ability to provide personalized recommendations and a more interactive experience for selecting payment methods or card options.</p> <p>For loans, both digital voice assistants and conversational AI share the highest comfort levels, likely owing to their ability to simplify loan terms while retaining an element of human-like interaction. Investments, however, see moderate comfort across all AI tools, reflecting a lack of standout preference.</p>

<h5><b>The Use phase: While keen on AI-enhanced payments, consumers are more conservative about ongoing use in banking</b></h5> <ul> <li><span class="eds-label">Older consumers’ interest in AI rebounds in the Use phase</span><br> <br> </li> <li><span class="eds-label">In digital payments, AI finds its groove</span><br> <br> </li> <li><span class="eds-label">Trust in AI plummets in investments</span></li> </ul> <p>Consumers’ inclination to use AI shows a slight uptick in the Use phase, especially in the digital payments category, where the index score exceeds the global average by 4 points (see Figure 4). </p> <p>From the Buy phase to the Use phase, the overall score in digital payments increases by 7 points. The biggest reason for this upswing is AI’s versatility in payments. In addition to assisting consumers in making purchases, it helps track transaction history and automate budgeting and fraud detection. </p> <p>The Use phase offers fewer opportunities for AI in product categories like investments, where enthusiasm tends to drop after the Learn and Buy phases. And as with other consumer journey phases, there are big differences among consumer groups. </p> <h6>Banking and financial services AI Inclination Index: The Use phase</h6>

#

<p><span class="small">Figure 4 <br> Base: 8,451 respondents in the US, UK, Germany and Australia <br> Source: Cognizant Research</span></p> <p><b>Older consumers’ interest in AI rebounds in the Use phase</b></p> <p>Consumers 55+ consistently show the highest interest in AI across most product categories in the Use phase, but particularly for deposit accounts. This likely reflects their reliance on secure, straightforward financial products where AI can monitor accounts and make personalized recommendations.</p> <p>Older consumers’ greater interest in AI extends to digital payments, where younger generations might be expected to lead. Capabilities like flagging suspicious activity in real time or providing alerts for routine bill payments could offer older consumers peace of mind.</p> <p>Younger generations, such as the 25–34 cohort, also demonstrate strong comfort with using AI in digital payments, driven by their preference for mobile-first solutions and modern financial habits.</p> <p>Meanwhile, investments and loans see lower scores across all age groups, but the 25–34 cohort comes out on top, likely due to their active financial engagement at this life stage.</p> <p><b>In digital payments, AI finds its groove</b></p> <p>Digital payments shine as the strongest performer in the Use phase, with a score exceeding the global average by 4 points. This strong interest in AI tracks with the growing interest in digital payments. <a href="https://www.pymnts.com/money-mobility/2024/study-digital-wallets-to-overtake-debit-cards-for-in-store-payments-by-2027/" target="_blank">According to a report by Worldpay</a>, digital wallets are projected to surpass debit cards in transaction volume at physical points of sale by 2027.</p> <p>And beyond simple transactions, digital wallets are evolving into versatile platforms. Consumers now use them to store essentials like driver’s licenses, passports and event tickets, while also taking advantage of advanced money mobility features such as account-to-account transfers.</p> <p>As payment tech evolves, financial consumers will gain a greater understanding of AI’s potential in the Use phase; for instance, AI algorithms can analyze transaction size, destination and historical patterns to determine the most efficient route for any given payment.</p> <p><b>Trust in AI plummets in investments</b></p> <p>Investments emerge as the weakest-performing category, dropping 10 points from the Buy phase to the Use phase. Consumers remain wary of entrusting AI with high-stakes decisions involving their financial future. The technology comfort score for investments is a mere 5. As one consumer noted, “Any scenario where AI is managing your investments directly is way too far for me and can cause a lot of problems, such as selling off your most valuable investment at a bad time.”</p> <p>AI in investments also faces heightened scrutiny from regulatory bodies like the SEC in the US and the FCA in the UK. While these efforts aim to safeguard market integrity, they also slow adoption. Compounding the issue is the phenomenon of “AI washing,” where firms overstate their AI capabilities. In March 2024, the <a href="https://www.sec.gov/newsroom/press-releases/2024-36" target="_blank">SEC settled charges</a> against two investment advisers for misleading investors about their use of AI, including one firm that falsely claimed to use client data to enhance its algorithmic strategies. One consumer from our study addressed this fear, “The drawback I see is someone taking the information that they learn from AI and selling the information as if they’re a financial investment guru.”</p> <p>Transparency remains a critical challenge for AI-powered investment tools. Unlike digital payments, where the benefits of AI are clear and tangible, investment tools often fail to provide users with the clarity they need to trust the technology. Consumers struggle to understand how algorithms assess risk or recommend assets. Building trust in this complex category will require greater emphasis on explainable AI and hybrid approaches that blend human expertise with technological insights.</p>

<h4>Meeting consumers where they are in banking and financial services</h4> <p>Consumer use of AI is growing fast and, with it, the emergence of consumer AI agents. For banking consumers, AI agents will act like a personal financial planner, orchestrating complex tasks, like tracking investments and securing the best loan deals. Soon, the internet as we know it today will become the agentic internet: an interconnected ecosystem of AI-enabled tools and agents that autonomously locate, evaluate, purchase and maintain the products and services they rely on.</p> <p>For the financial services sector, this means future banks won’t exist in isolation. They’ll be deeply interconnected with other players in the financial ecosystem: payment providers, fintech innovators, even industries like healthcare or e-commerce.</p> <p>While consumer AI uptake may be somewhat slower in banking and financial services, we believe leaders have less than five years to navigate this change. To prepare for the AI-driven consumer era ahead, banking and financial services businesses will need to rethink how they operate across these areas:</p> <ul> <li><b>Prioritize hybrid human-AI models for high-stakes decisions:</b> Given consumers’ skepticism toward AI in critical financial areas like loans and investments, a practical path forward will be a hybrid approach that combines AI-driven analysis with human oversight. AI can efficiently generate initial recommendations and risk assessments, but human advisors will remain essential in interpreting these insights, adapting them to individual circumstances and providing the reassurance that consumers seek in complex financial decisions.<br> <br> Banks should implement clear, accessible processes for consumers to request a human review of AI-driven decisions, ensuring that customers feel empowered rather than excluded from the decision-making process. By striking the right balance between AI efficiency and human judgment, financial institutions can meet both consumer expectations and regulatory requirements, ultimately strengthening confidence in AI’s role in high-stakes financial products.<br> <br> </li> <li><b>Delicately balance AI and human trust:</b> The success of AI in banking hinges on gaining consumer confidence, especially for high-stakes products like loans and investments. Our research shows that trust still plays a fundamentally important part of the financial services business—and regardless of advances in AI, consumers are still squeamish about its involvement in their financial lives.<br> <br> By deploying explainable AI models that detail how and why recommendations are made, financial institutions can satisfy regulatory requirements and reassure consumers that their decisions are supported by sound, verifiable logic. Replaying the algorithm’s rationale in a human-understandable way leads to better outcomes for both lenders and borrowers. Explainable AI will be crucial for building trust.<br> <br> </li> <li><b>Tailor the use of AI to generational preferences:</b> While current AI interactions vary by generation, the differences provide valuable lessons that inform the transition toward AI agents, ensuring they are trusted, effective and aligned with longer-term consumer behaviors.<br> <br> For older consumers (45+), the emphasis on security, clarity and human oversight highlights the importance of explainability in AI-driven financial decisions. Their preference for advisory-style interactions suggests that AI agents will need strong transparency measures and escalation pathways to build long-term confidence. <br> <br> Among consumers aged 25–44, the adoption of AI-driven personalized recommendations for investments and lending decisions underscores the need for precision and tailored insights. AI agents will need to evolve beyond static recommendations and become proactive financial assistants that offer real-time, context-aware guidance while ensuring explainability. <br> <br> Eighteen-to-24-year-olds’ ease with mobile-first, automated financial experiences points toward a future where AI agents function as embedded, predictive financial companions: anticipating needs, offering proactive solutions and enhancing personalization at scale. This cohort’s comfort with automation sets the foundation for AI agents to become central to financial decision-making.</li> </ul>

Jump to a section

Introduction #spy-1

AI across the financial consumer journey #spy-2

subnav- The Learn phase: AI has a place in demystifying complex financial products#spy-3

subnav- The Buy phase: As financial stakes increase, consumers are less likely to close a deal using AI#spy-4

subnav- The Use phase: While keen on AI-enhanced payments, consumers are more conservative about ongoing use in banking#spy-5

Meeting consumers where they are in banking and financial services #spy-6

<h5>Authors</h5>