While banks debate strategy, their customers are rapidly embracing an AI-powered world. European financial institutions must lay proper foundations for agentic AI or risk being perpetually behind competitors who invested in the right infrastructure.

JPMorgan Chase made headlines in late September with its blueprint to become "the world's first fully AI-powered megabank," with Chief Analytics Officer Derek Waldron interviewed by CNBC. The bank's LLM Suite platform can now create investment banking decks in 30 seconds—work that previously took teams of junior bankers hours to complete. But here's the crucial detail: JPMorgan spent years building the foundation first.

Some 96% of enterprises are expanding their use of AI agents, according to Cloudera's April 2025 survey of IT leaders across 14 countries. Banking is facing an unprecedented transformation, in which agentic systems—capable of independently executing complex, multi-step tasks and learning from interactions—have transitioned from experimental technology to essential infrastructure.

The global agentic AI market in financial services reached $2.1 billion in 2024 and is projected to hit $80.9 billion by 2034, representing a 43.8% compound annual growth rate, Market.us reported earlier in 2025. North America leads adoption, but European institutions are rapidly closing the gap as they recognize agentic capabilities as core business infrastructure.

This shift reflects broader market pressures. Consumer purchasing behavior is evolving toward intelligent, anticipatory experiences. Regulatory complexity continues to increase across European jurisdictions. Cost-income ratios demand optimization amid uncertain economic growth. Traditional operational models—built for human-centric workflows—struggle to address these converging challenges simultaneously.

Yet implementation remains problematic. While banks understand agentic potential, many struggle with execution. Pilot programs proliferate but fail to scale. Legacy systems resist integration. Workforces lack preparation for synthetic collaboration. The gap between strategic intent and operational reality creates competitive vulnerability for institutions that delay building proper foundations.

The October 2025 Evident AI Index tells the story: JPMorgan Chase leads global banks in AI readiness, while two European institutions—UBS and HSBC—slipped in rankings despite significant investments. Meanwhile, Bank of America and Morgan Stanley made dramatic gains, demonstrating that speed matters less than investing in a systematic foundation.

This three-part series examines how European banks can successfully navigate agentic transformation, starting with the foundational investments that determine long-term success.

Agentic future vs today's reality

Sarah, a product owner at a progressive European bank, arrives at her office in 2027 with business cases already prepared. Her AI agents worked overnight, analyzing customer behavior patterns and stress-testing regulatory compliance. Where she once spent weeks gathering information, she now spends time making strategic decisions. Her "sparring agent"—trained to think like a former Big Four auditor—has already flagged potential weaknesses in her proposals.

Meanwhile, business owner Fred receives his daily briefing, which shows automatically compiled business unit performance metrics, optimised cost-income ratios across product lines, and strategic growth opportunities ranked by market potential. This is only achievable because Fred has four unique agents—his Finance agent, Product Manager agent, Business Manager agent, and Strategy agent—all interacting and challenging one another. The Finance agent questions the Product Manager about revenue projections. The Business Manager agent validates market assumptions. The Strategy agent synthesizes their debate into actionable recommendations.

Elsewhere, Elena, the technical owner, discovers that 47 applications were deployed seamlessly while she slept, and that three security vulnerabilities were detected, patched, and documented without human intervention.

Some institutions are already building toward this future. However, most European banks remain stuck between ambition and execution, planning for transformation while struggling to implement it.

Back in 2025, Sarah manually reviews call center reports from yesterday's complaints, scheduling meetings to address problems that occurred 18 hours ago. Information gathering consumes most of her strategic thinking time. Fred discovers business unit underperformance through quarterly reviews—issues that real-time analytics could have flagged weeks earlier. His strategic planning remains reactive rather than predictive. Elena's team worked overnight on system patches, with manual deployment processes creating bottlenecks.

The distance between today's manual processes and tomorrow's autonomous possibilities represents more than technological evolution. It represents a competitive transformation that will separate market leaders from followers.

Consumer expectations gap

Consumer behavior is shifting faster than banking transformation. Cognizant's New Minds, New Markets research shows that AI-powered consumers could drive up to 55% of spending by 2030. These customers already experience AI-powered interactions across various industries, including retail, entertainment, and travel. They expect the same from their banks.

Yet financial institutions face a critical implementation gap. While many plan to adopt generative systems, fewer have implemented cross-enterprise solutions at scale. This gap creates more than competitive pressure. It threatens the fundamental economics of the banking industry.

Realizing agentic AI benefits is central to closing the consumer expectations gap and creating necessary headroom in cost-income ratios for the uncertain growth ahead.

Banks are on a journey to find ROI from AI investments. Despite significant spending on proof-of-concepts and pilots, many institutions struggle to demonstrate meaningful returns. Agentic AI can deliver those returns if properly embraced.

The transformation requires a shift from the analog mindset. Like the industrial revolution, successful adoption means lower workforce requirements but dramatically higher output. One progressive European bank shared its workforce planning: 800 human employees will be supported by 2,200 autonomous systems by 2027, with thousands of agents sitting behind these systems. This represents workforce expansion through synthetic collaboration, not replacement.

But achieving this requires foundation investment. Banks attempting agentic transformations without proper groundwork encounter predictable barriers: data trapped in silos, systems that can't communicate, and workforces unprepared for synthetic colleagues.

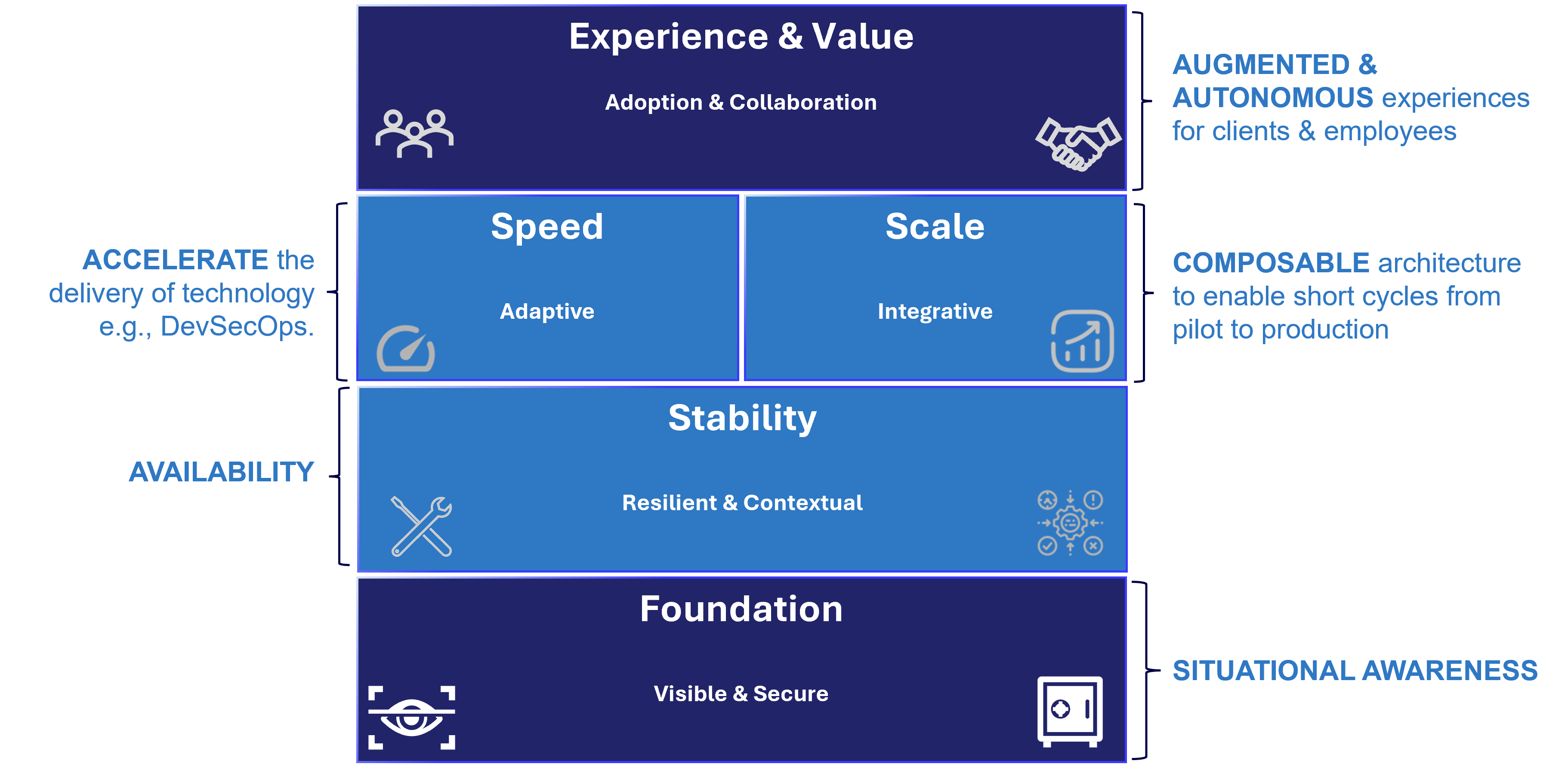

Foundation pillars

Success requires five critical foundations that must work as an integrated system, creating the architecture needed to deliver speed, scale, and sustainable value.