European banks are embracing enterprise-scale agentic AI, but there's no single route forward. Cognizant's experience working with financial institutions reveals three distinct vectors for prioritization—and why consciously choosing matters more than following a predetermined path.

Agentic transformation is more than a technology shift—it’s a defining leadership moment. European banks that move decisively can set new standards for customer-centric innovation and unlock new growth models. Yet, with decades of complex systems and processes, IT leaders recognize that success demands a tailored, strategic approach to implementation.

What's emerging from Cognizant's work with European financial institutions is experience-led insight rather than prescriptive blueprints. Three distinct vectors deliver different outcomes at different speeds.

- Vector one enables product development and accelerates the elimination of technical debt.

- Vector two pioneers agent development cycles to help enterprises build new AI products and services.

- Vector three represents a perennial objective: do more with less.

The vector you prioritize first determines which teams you empower, how you measure success, and whether you're building toward enterprise scale or accumulating scattered experiments. Each bank's transformation will unfold differently, but the strategic choices remain consistent.

Vector one: enabling product development and accelerating technical debt elimination

Vector one transforms the software development lifecycle itself. Current teams typically run a set of developers under one manager, clustered in expensive locations. Vector one reconfigures this to a four-to-one ratio, with half the team working from cost-efficient cities. Development cycles run around the clock, passing work across time zones.

JPMorgan Chase exemplifies this approach, as the first article in this three-piece series points out. Its LLM Suite creates investment banking decks in 30 seconds—work that previously took teams hours. The same principle applies to code development, testing, and deployment.

The shift moves from traditional Software Development Life Cycle (SDLC) to what's emerging as ADLC: Agentic Development Lifecycle. You'll maintain some conventional development, but successful banks achieve 80-20 or even 90-10 splits, with agentic frameworks handling routine work. The ADLC becomes dominant: agents handle the actual development while humans focus on architecture, observability, and decision-making.

Technical debt that accumulated over decades starts unwinding at pace. Product development that took quarters compresses to weeks. The constraint shifts from development capacity to strategic prioritization.

Strategic fit: Choose vector one if development capacity constrains your organization, technical debt drowns your modernization efforts, or you need to match competitor velocity. This vector delivers the fastest visible returns with the least organizational disruption.

Vector two: pioneering agent development cycles to build new AI products and services

Vector two addresses what happens after initial success: how do you industrialize agent development to build new AI products and services at scale? This is where most banks can stumble—they prove the concept, then hit the industrialization wall.

The parallel with robotic process automation (RPA) is instructive. Organizations deployed bots across business units. Productivity surged initially. Then they hit 150 bots with no clear ownership, no tracking of what was executed where, and no way to measure which bots delivered value.

Agentic AI provides the intelligence that RPA lacked—genuine decision-making rather than just rules-based automation. But it creates a different challenge: inventory management at scale. Without systematic industrialization, you end up with thousands of agents doing similar tasks across different business units, with no coordination or reuse.

Banks succeeding at scale focus on operations and back-office processes with proper governance frameworks established before expanding deployments.

Vector two establishes three critical components:

- Agent repository: Where components live for reuse across the enterprise. Build once, deploy everywhere. This functions like GitHub for agents—version control, component management, and central improvement.

- Agent registry: Where agents are tracked for governance, utilization, and cost management. How many agents are deployed? What business services are they executing? Which ones consume excessive compute power relative to the value delivered?

- Agent orchestration: How agents coordinate with each other and existing systems. This is the difference between deploying 200 isolated agents versus deploying an orchestrated system where agents pass information, divide work, and escalate to humans appropriately.

Strategic fit: Choose vector two if you're ready to build institutional AI product capabilities, have development and infrastructure teams that can support systematic deployment, or want to establish competitive differentiation through proprietary agents.

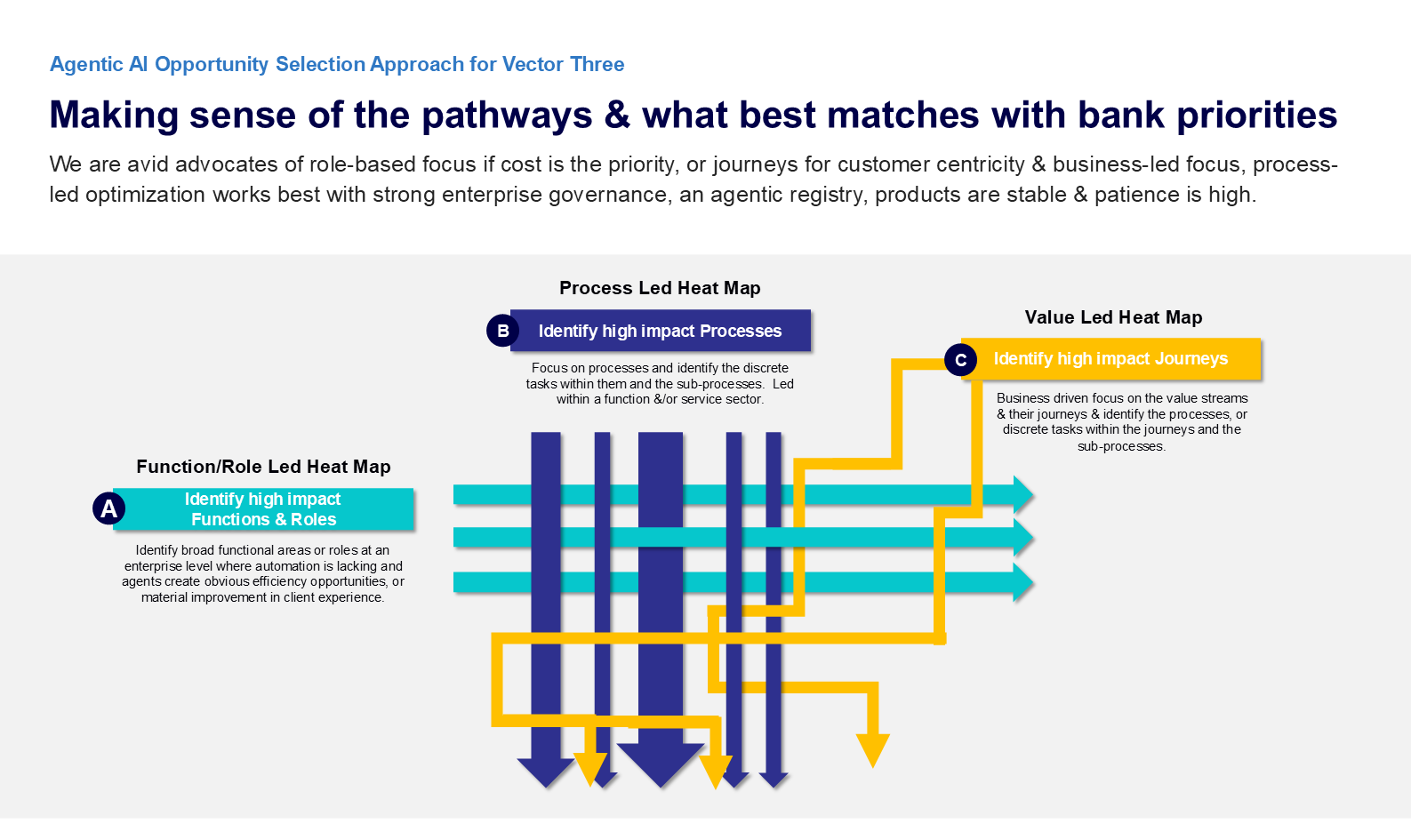

Vector three: unlocking new spend pools through workflow transformation

Vector three represents a perennial objective: do more with less. This is the most ambitious path, fundamentally transforming people-intensive workflows to unlock spend pools that weren't previously addressable. This goes beyond replacing human efforts with agents—it's about reimagining entire workflows to deliver outcomes that weren't economically viable under traditional operating models.

The strategic question becomes: where do you intervene?

Three distinct paths emerge, each aligned with different organizational priorities.