The financial services industry is preparing to shorten the settlement cycle for several financial instruments from T+2 to T+1 (i.e., 3 days to 2 days).

In the US, the roadmap has now been laid to implement this change by mid-2024. The Canadian Capital Markets Association has confirmed transition to a T+1 settlement cycle on same day as the US markets. Mexico is also exploring a move to T+1, but any formal plan has not yet been announced.

In the European context, AFME published a paper in September 2022 to discuss if EEA should also move to a T+1 settlement regime. UK has also now put a foot forward in this direction with the government launching an Accelerated Settlements Taskforce in December 2022 to assess the potential for accelerated settlements of financial trades in the UK.

This tectonic shift in the settlements process will put a huge strain on banks as existing post trade operating models built upon legacy technology and siloed operations will be put to the test. It would, therefore, require a coordinated effort from market participants to make this transition a success.

While this change may appear painful in the short term in terms of operational and technological overhauls but in the long term, the industry will reap the benefits of reduced counterparty & market risks, increased liquidity and reduced volatility. The end client (street investor) also stands to gain as they would have access to the proceeds of their trades on the next day itself, reducing the market risk faced and improving liquidity.

There will likely be several legal, regulatory, technological and infrastructural challenges that will require a coordinated effort. These challenges include:

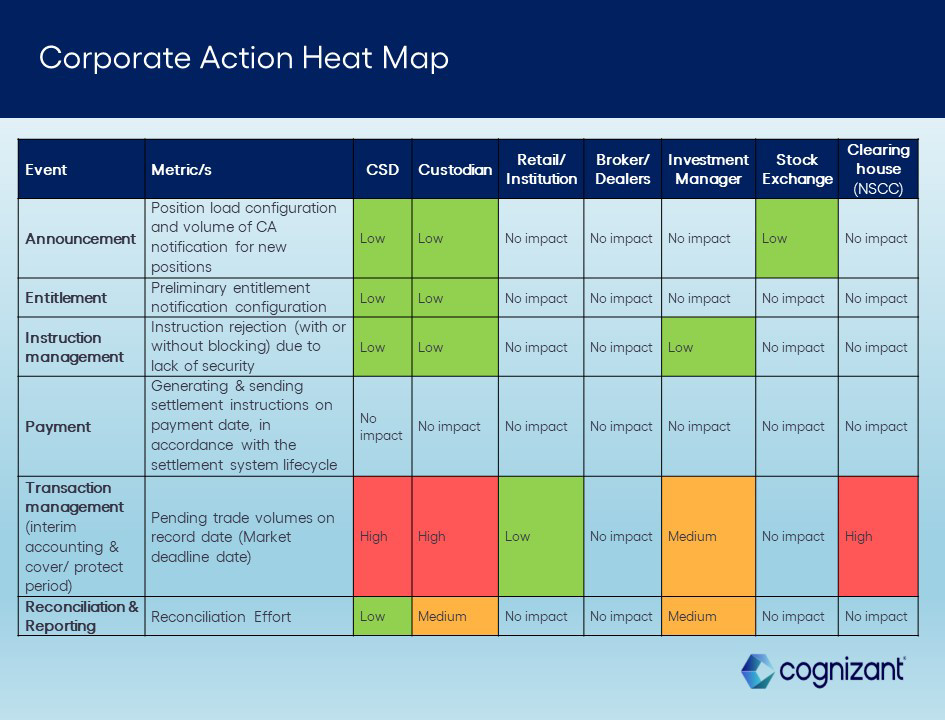

Increased operational complexities for global participants stemming from time zone differences (i.e., a single global ‘close of business day’ process) and cross-currency FX transactions.

Securities lending impact as the timeline to identify and recall securities is reduced which can increase settlement fails and penalties.

Impact on asset servicing functions such as corporate actions because of changes to ex-date, cover/protect period.

This article focuses on the impact T+1 will have on how corporate actions are handled in the settlement process.

So, what is the fuss around Corporate Actions?

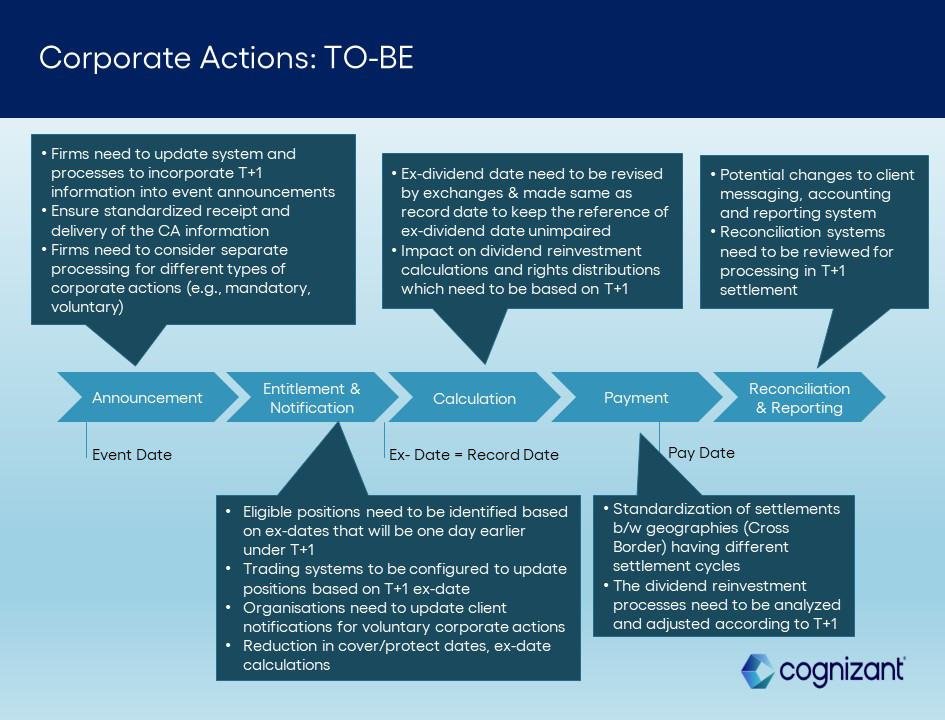

Corporate actions, owing to their high volumes, variations and manual/semi-automated operational processes will be under stress. As part of moving to T+1, some potential impacts on Corporate Actions processes are:

Ex-date calculation and cover/protect period changes

Dividend reinvestment process adjustment

Distinct processing of different corporate actions (mandatory, voluntary etc.) owing to different timelines and processes

Entitlement capture process-related adjustments

Reconciliation and reporting processes would need to be reviewed for T+1

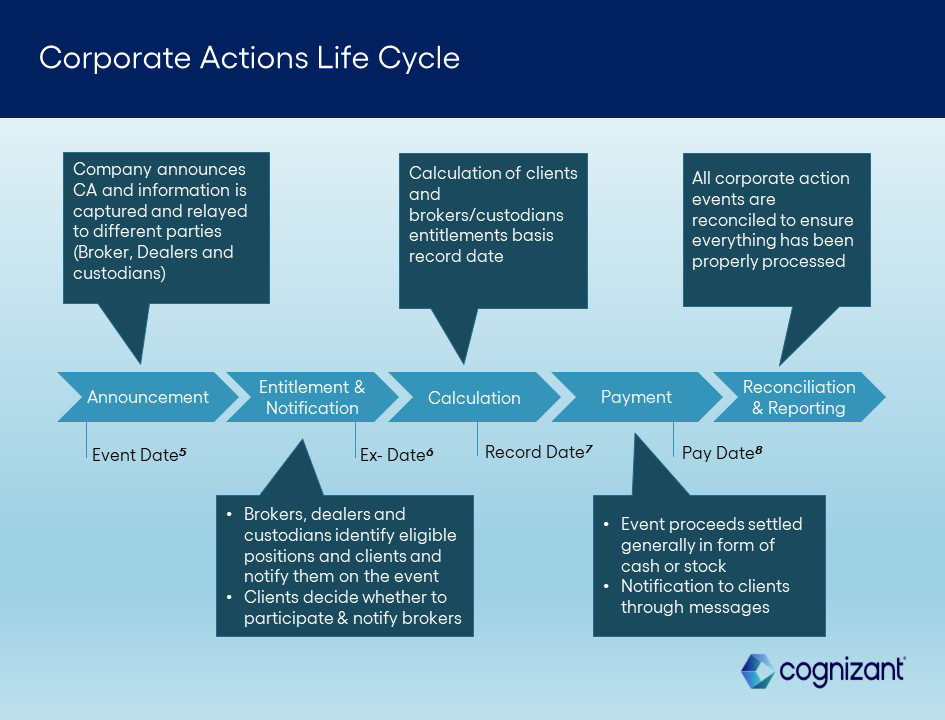

How are Corporate Actions managed today?

Corporate Actions can be mainly classified4 as mandatory or voluntary as listed below:

| Mandatory | Voluntary |

| Dividends (cash, stock, property etc.) | Rights issue |

| Stock splits | Optional dividends |

| Acquisitions | Tendor offers |

A typical Corporate Actions lifecycle is illustrated below: