While insurers are benefiting from admirable technology investment, they face both macroeconomic uncertainty and an evolving marketplace.

Few industries are as well positioned for the future as insurance. As Economist Impact research commissioned by Cognizant demonstrates, the industry, which was investing heavily in digital even before the pandemic, is full of companies that are recognizing strategic business value from their digital investments.

Yet challenges remain. Insurers find themselves beset by niche insurtech competitors that are unencumbered by technical debt; a sometimes-challenging regulatory environment to innovate within; and ever more demanding consumers who insist on shopping, buying, and servicing experiences for complex products at a level akin to a purchase of a new set of earbuds.

Here are insights on ways in which the insurance industry is future-ready—and where there is work to be done.

Sustaining the first-mover advantage

What they’re good at

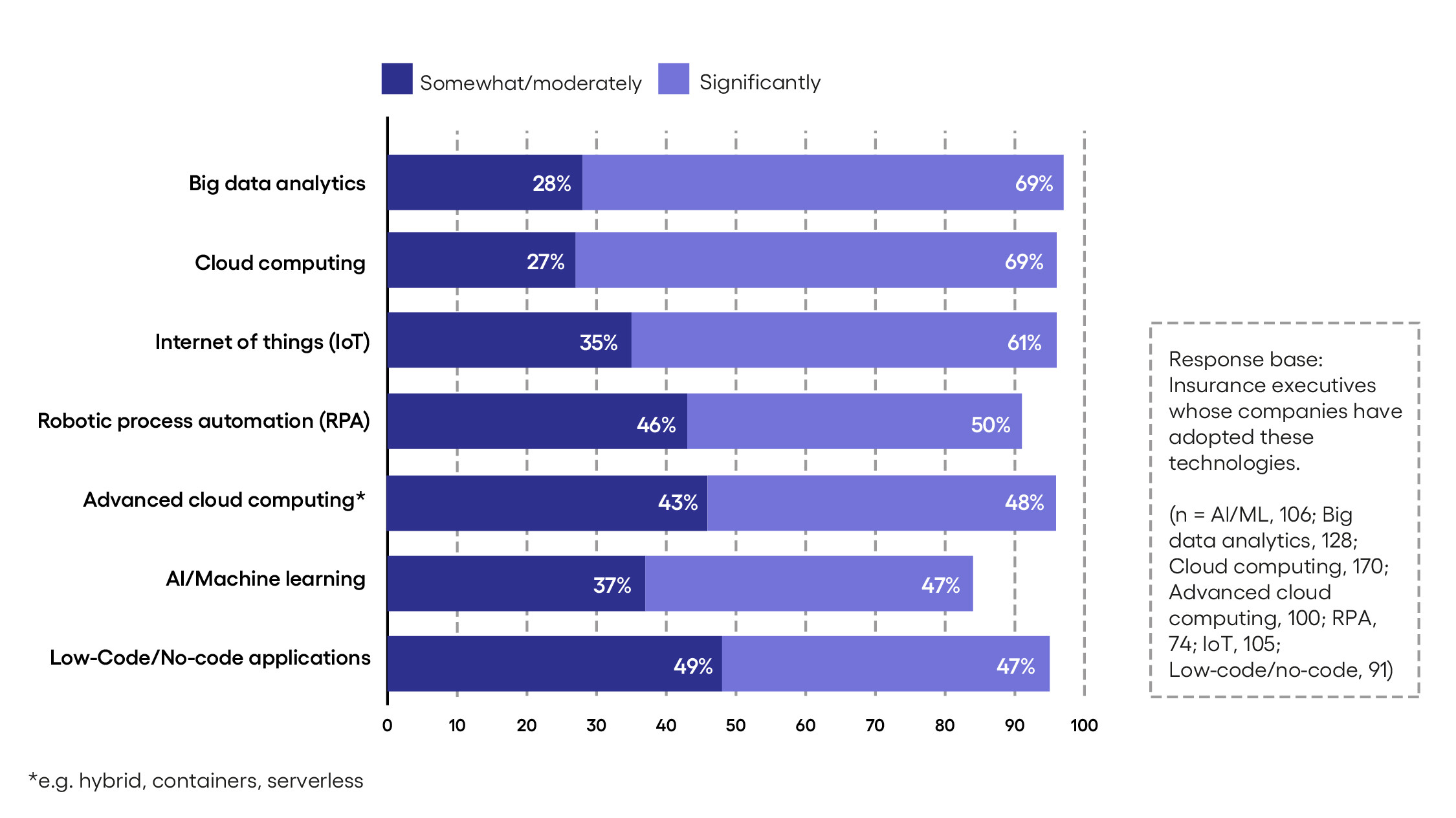

- Mastery of data. Insurance is all about data: how it informs the design of products and services, and how it manages customer experience. Insurers are ambitious users of technology and are skillful at linking it to business goals and extracting strategic value from it—this is fundamental to the business. Big data analytics and cloud technology are increasingly being used to handle the massive volumes of data passing through systems and risk engines, searching for insights that lead to differentiation. Almost seven in ten insurance companies that have adopted these two technologies are seeing them deliver significant value. Tech is moving beyond the foundational to the frontier, opening the doors to emerging risks and protection with the promise of predictive analytics and artificial intelligence (AI) contributing to healthier bottom lines and superior customer experience.

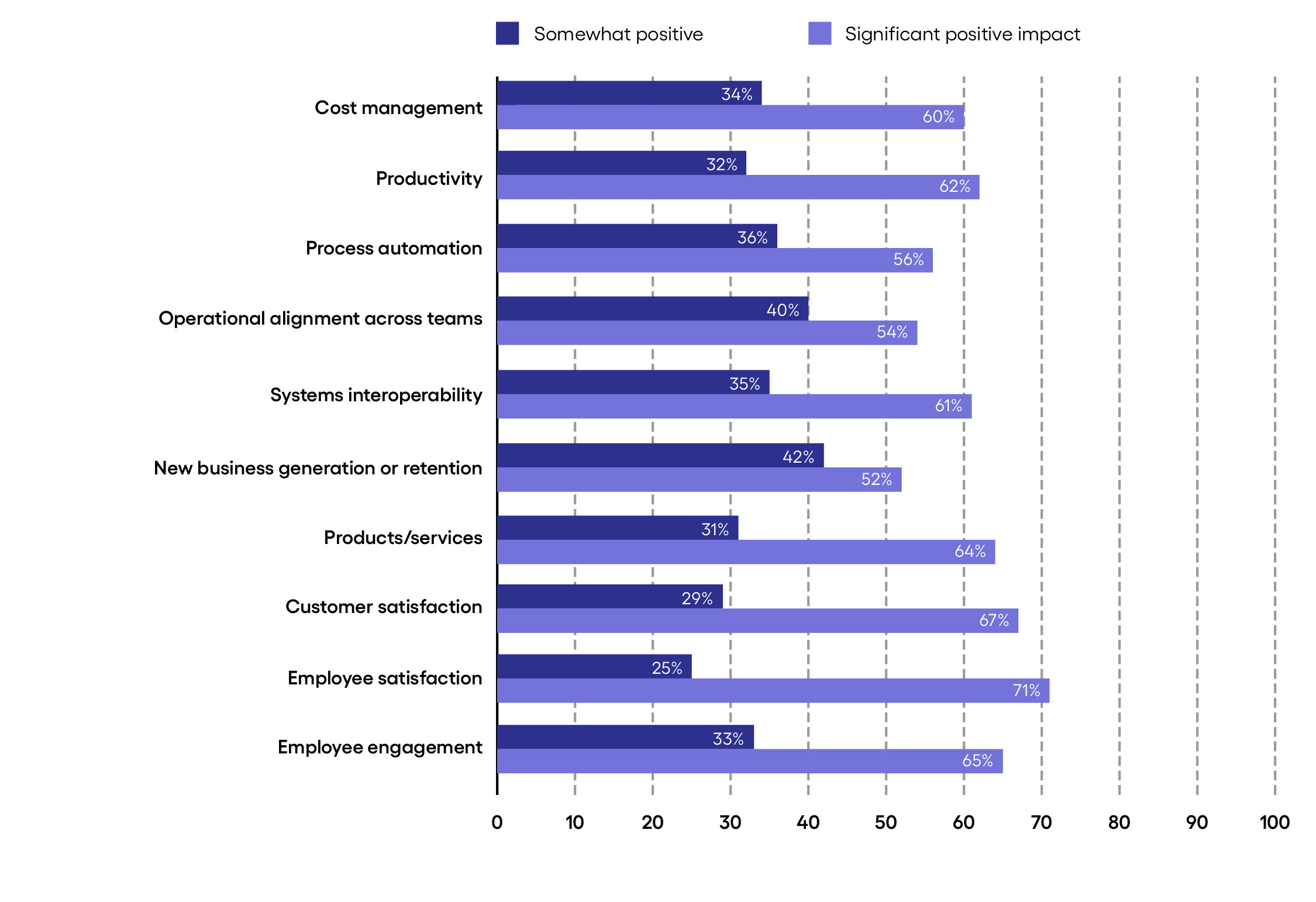

Insurers are deriving significant strategic value from tech investments

Respondents were asked to what extent the following technologies and methodologies already adopted by their business are delivering strategic value to their operations. (Percentage of respondents who advised each technology is, or is not, providing significant value to their business)