RESEARCH

What consumer preferences reveal about the future of AI in insurance

<p><br> <span class="small">August 21, 2025</span></p>

What consumer preferences reveal about the future of AI in insurance

<p><b>Our AI Inclination Index reveals which consumers are most open to using AI in the insurance purchase journey—as well as where and how they’ll use it. Knowing this, insurance organizations can develop a highly nuanced and effective consumer-facing AI strategy.</b></p>

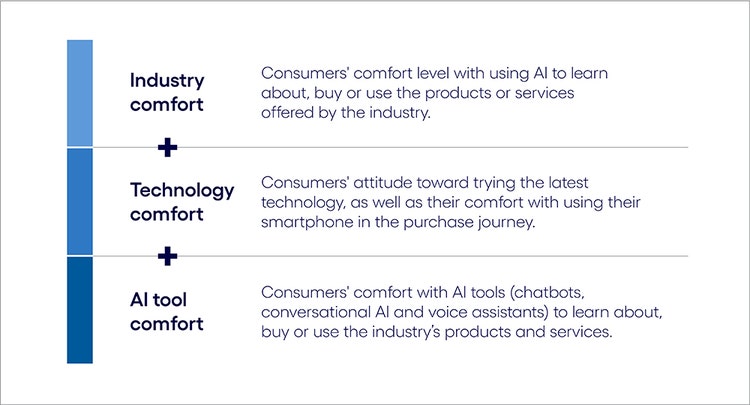

<p>Consumer AI tools offer a powerful opportunity to simplify and personalize the insurance customer journey. Instead of simply automating transactions, AI could enhance key points of engagement, from initial needs analysis and coverage selection, to intelligent servicing and seamless claims processing, to, in some cases, responsive investment management.</p> <p>Yet integrating AI into insurance requires precision. The customer relationship is deeply trust-dependent, demanding security, accountability and strict privacy safeguards. Because consumers rely on insurers to protect high-value financial and personal assets, even minor missteps in AI deployment can have far-reaching consequences.</p> <p>For this reason, the growing use of AI among consumers poses a distinct challenge for insurers as they strive to effectively engage with and retain customers. Which consumers are most (and least) inclined to use AI? Which tool would they prefer to use? And where in the purchase process would they be most comfortable using it?</p> <p>Our recent research uncovered some nuanced answers to those questions. Using data from <a href="https://www.cognizant.com/us/en/aem-i/new-minds-new-markets-ai-customer-experience" target="_blank">our recent consumer AI study</a>, we developed the AI Inclination Index, which quantifies consumers’ propensity to use the technology (see explainer box below).</p> <p>While the index reveals a lower inclination to use AI when purchasing insurance products than other industries’ products and services (see Figure 1), that broad finding masks important variations. For instance, consumers’ comfort levels differ dramatically across the three key phases of the consumer journey (Learn, Buy and Use) and the two insurance product categories in our study:</p> <ul> <li>Insurance (life, home, auto insurance)</li> <li>Investments (stocks, bonds, funds, exchange-traded funds, retirement accounts)</li> </ul> <p>Consider some of these findings on AI usage in the insurance customer experience:</p> <ul> <li><b>The Learn phase is where insurance consumers are most apt to use AI. </b>Comfort with AI is highest for researching insurance options. It then declines at the Buy phase, when purchasing decisions are finalized. AI inclination drops steeply in the Use phase, lagging significantly behind other industries. This is likely due to the high-stakes financial implications of filing claims and making investments, as well as the infrequent nature of insurance transactions. Most policyholders rarely interact with their coverage unless prompted by a life event or claim, dampening AI usage in the Use phase compared with higher-touch industries. Overcoming these hesitations presents a key growth opportunity for insurers.<br> <br> </li> <li><b>AI inclination varies dramatically across consumer age groups and purchase journey stages. </b>While the Learn phase is led by consumers aged 45 to 54, the Buy phase sees peak engagement from the 35–44 group, reflecting their comfort with automated financial decision-making. In the Use phase, the oldest consumers (55+) are most eager for AI to help manage their insurance activities, while younger investors (25–44) are interested in engaging with AI-powered portfolio tools.<br> <br> </li> <li><b>The tool of choice is often conversational AI.</b> This is particularly true in the Learn phase, where conversational AI consistently received the highest scores across both product categories. Its ability to provide personalized, interactive guidance makes it a valuable resource for consumers navigating complex policies.</li> </ul> <p><b>The AI Inclination Index</b></p> <p><i>To quantify consumers' propensity to adopt AI-driven technology features throughout the consumer journey, we developed the AI Inclination Index. The index was calculated using three measures from our New minds, new markets survey data.</i></p>

#

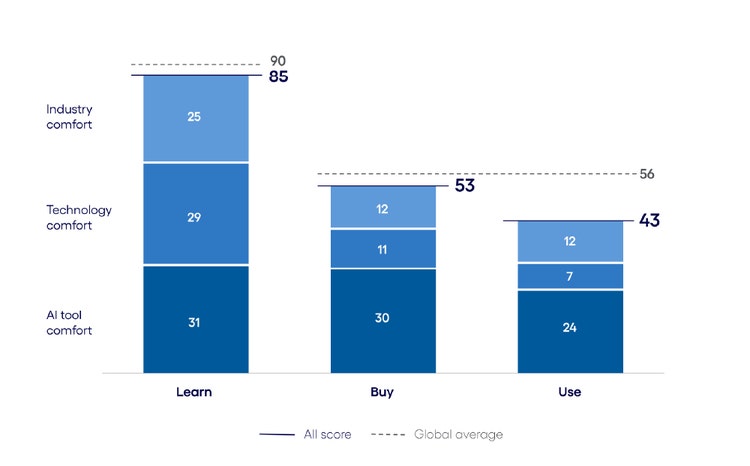

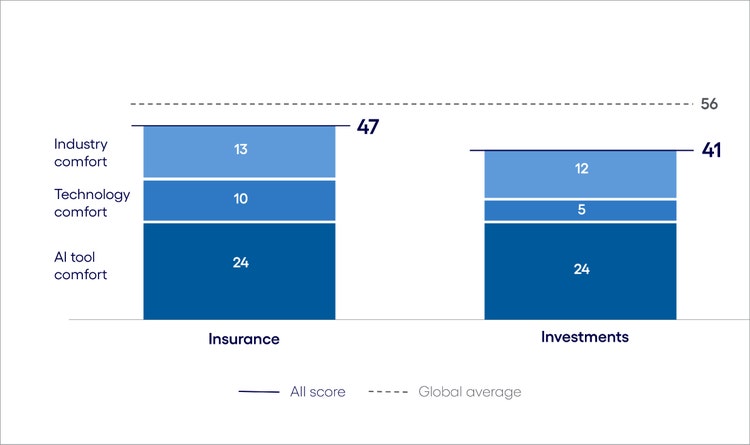

<p><b><br> AI inclination in insurance vs. the global average </b></p> <p><i>Consumers are somewhat less inclined to use AI when purchasing insurance-related products than other industries’ goods and services.</i></p>

#

<p><span class="small">Figure 1<br> Base: 8,451 respondents in the US, UK, Germany and Australia<br> Source: Cognizant Research</span></p> <p>With these variances, it’s clear insurance businesses will need to craft an AI strategy that captures the greatest areas of opportunity while carefully mitigating the risks associated.</p> <p>Understanding consumer use of AI, as well as the accompanying pockets of spending power, is essential for leaders in all industries. In our global study “<a href="https://www.cognizant.com/us/en/new-minds-new-markets-ai-customer-experience" target="_blank">New minds, new markets</a>,” we found that consumers who are enthusiastic about using AI will account for up to 55% of all purchases made across industries. This amounts to $4.4 trillion in spending in the US, $690 billion in the UK, $690 billion in Australia and $540 billion in Germany.</p> <p>In this report, insurance leaders will learn about where in the purchase journey consumers are most and least inclined to use AI, the AI tools they would be most apt to use and differences across age groups. With this information, businesses can reshape their approach to customer engagement—where and how it matters most.</p>

<h4>AI across the insurance consumer journey</h4> <p>As our AI Inclination Index indicates, consumers are somewhat less likely than the cross-industry average to use AI across all three stages of the insurance consumer journey: Learn, Buy and Use. This disparity is most evident in the Use phase, where the score is 13 points lower than the global average.</p> <p>Such hesitation reflects two key dynamics:</p> <ul> <li><b>Consumer sentiment.</b> Unlike sectors where AI enhances everyday transactions with minimal perceived risk, insurance remains deeply trust-dependent. Merely participating requires consumers to share some of their most sensitive data, touching on health, wealth and personal behaviors, which raises the stakes for every digital touchpoint. Consumers expect transparency, personalization and human oversight in policy decisions. <br> <br> This is particularly true in the Use phase, where confidence in AI-driven claims processing and policy adjustments remains limited, likely because these processes demand tone-sensitive customer service, and it’s a place where consumers need assurance that outcomes are accurate and fair. These processes often touch deeply personal experiences, and people want to feel heard, not just processed.<br> <br> </li> <li><b>Regulatory compliance requirements.</b> Through measures like the <a href="https://www.google.com/url?sa=t\&source=web\&rct=j\&opi=89978449\&url=https://www.brownejacobson.com/insights/the-word-april-2024/eu-ai-act\&ved=2ahUKEwiyspDGi7SNAxXcREEAHcmaIBIQFnoECBcQAQ\&usg=AOvVaw0vck6evCZAuy-bj0YeGQ7W" target="_blank">EU’s AI Act</a>, the role of AI in risk modeling, underwriting fairness and claims adjudication is under the spotlight. The act has categorized risk assessment and pricing in life and health insurance as high risk for the use of AI, reinforcing the need for caution in fully automating critical financial processes.</li> </ul> <p>While insurers have made strides in AI-powered fraud detection and dynamic risk assessment, these tools largely operate behind the scenes, rather than serving as direct consumer-facing solutions. AI’s ability to improve underwriting efficiency is clear, but its role in decision-making at the consumer level faces trust barriers.</p> <p>Meanwhile, the application of AI in insurance investments is far from frictionless. Robo-advisors and automated portfolio management tools have gained visibility, but post-purchase adoption remains low. Many consumers hesitate to trust AI with long-term investment oversight, particularly in volatile market conditions, where human judgment and strategic flexibility remain paramount.</p> <p>Bridging the trust gap, particularly in claims management and post-purchase engagement, will be key to unlocking AI’s full potential in insurance.</p>

About our analysis

To understand consumer AI behaviors and attitudes at a granular level, we structured our analysis around four key pillars:

- The consumer journey. We studied the specifics of AI use at each phase of the customer journey. This journey—how consumers discover, purchase and engage with products and services before and after a sale—is at the heart of the business-customer relationship.

- Consumer demographics. To gain a better understanding of how consumer attitudes and behaviors differ by age group, we divided consumers into five categories: 18-24, 25-34, 35-44, 45-54, and 55+.

- Consumer AI tools. We defined consumer AI use by asking about their intended use of three key tools that are prevalent in the consumer world: voice assistants, chatbots and conversational AI.

- Industry-specific products. We included two insurance product categories in our analysis: insurance and investments.

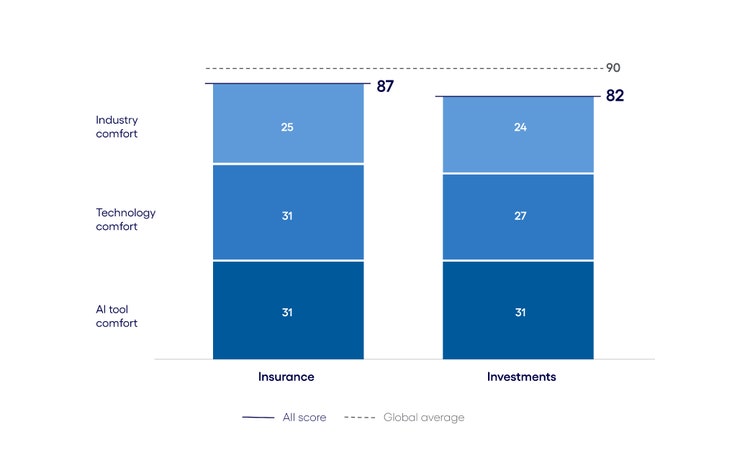

<h5>The Learn phase: Policy comparison capabilities bolster comfort with AI</h5> <ul> <li><span class="eds-label">Consumers are more interested in using AI to research insurance options than investments</span></li> </ul> <ul> <li><span class="eds-label">Older consumers are the biggest AI enthusiasts, but younger consumers remain engaged</span></li> </ul> <ul> <li><span class="eds-label">Conversational AI is the tool of choice</span></li> </ul> <p>The Learn phase ranks as the most comfortable stage for AI adoption in insurance. While index scores for both insurance and investment products fall below the global average, the former performs slightly better than the latter (see Figure 2).</p> <p>In the Learn phase, insurers have a valuable opportunity to secure consumer interest early and influence their decision-making before commitment. Success depends on understanding what drives AI adoption—what consumers find most useful, which tools they prefer and how businesses can enhance transparency and trust in AI-powered discovery.</p> <p><b>Insurance AI Inclination Index: The Learn phase</b></p>

#

<p><span class="small">Figure 2<br> Base: 8,451 respondents in the US, UK, Germany and Australia<br> Source: Cognizant Research</span></p> <p><b>Consumers are more interested in using AI to research insurance options than investments</b></p> <p>This preference may stem from consumers’ greater familiarity with AI-driven digital interactions in insurance, where comparison tools, automated risk assessments and policy estimators have become standard features. This familiarity is also reflected in the insurance product category’s slightly higher technology comfort score. As one consumer put it, “You tend to think recommendations from family and friends are more trustworthy, but with insurance, they may be not so well-informed or have access to the numbers and the bigger picture.”</p> <p>In contrast, investment products often require a higher level of financial literacy and trust, making consumers more hesitant to rely on AI alone for portfolio exploration. Regulatory factors also come into play. Investment platforms operate within tight compliance frameworks, limiting the extent to which AI can autonomously guide decisions.</p> <p>The European Securities and Markets Authority, for example, recently <a href="https://www.simmons-simmons.com/en/publications/clymordyh0020txdsa6abcze8/esma-published-guidance-for-firms-using-ai-in-investment-services" target="_blank">provided guidance</a> to firms using AI in investment services, emphasizing the need to comply with EU financial regulations. This includes ensuring that AI-driven recommendations align with clients' financial situations, investment objectives and risk tolerance. This directly impacts how AI can be used in portfolio exploration, as the technology cannot autonomously suggest portfolios that don't meet these criteria.</p> <p><b>Older consumers are the biggest AI enthusiasts, but younger consumers remain engaged</b></p> <p>Older generations, particularly the 45–54 cohort, are the most inclined to use AI to explore both insurance and investment products, with an index score of 68 for both product categories. This likely reflects their increased financial responsibilities, including long-term policy planning and retirement considerations.</p> <p>AI inclination scores for the youngest consumer cohort (18–24) drop just two points, but only for the insurance product category. As they begin driving, for instance, people in this age group might turn to AI-powered comparison tools to evaluate auto insurance quotes and assess policy benefits. Their reliance on digital tools makes AI-driven insurance discovery a natural extension of their technology use.</p> <p>The oldest consumer group (55+) exhibits similar interest in using AI for insurance products at this phase, reflecting an interest in policy security, risk assessment and automated comparisons.</p> <p><b>Conversational AI is the tool of choice</b></p> <p>Conversational AI can bridge the gap between consumer uncertainty and policy clarity. Unlike static comparison tools, which provide only surface-level pricing insights, conversational AI acts as an interactive advisor, helping consumers understand coverage options, exclusions and tailored policy recommendations in a way that feels personalized and intuitive.</p> <p>For instance, a consumer exploring life insurance could ask about term vs. whole-life policies, receive an explanation based on their financial goals, and even get scenario-based recommendations on long-term affordability—all without needing to sift through dense policy documents. This interactive, guidance-driven approach is also valuable in auto and home insurance, where details like accident history, location-based risks and deductibles can heavily influence pricing.</p> <p>By continuously refining responses based on consumer input, conversational AI makes policy selection less overwhelming and more confidence-driven, ensuring users feel empowered rather than uncertain and confused.</p>

<h5>The Buy phase: Trust issues and high stakes force an AI inclination drop</h5> <ul> <li><span class="eds-label">Younger consumers lead AI engagement in the purchase phase</span></li> </ul> <ul> <li><span class="eds-label">Insurance continues to hold a slight edge over investments</span></li> </ul> <ul> <li><span class="eds-label">Conversational AI dominates again</span></li> </ul> <p>AI interest drops in the Buy phase. However, while AI inclination scores in both product categories fall below the global average, it’s much higher than in the Use phase and closer to the global average when compared with the Learn phase.</p> <p>Capitalizing on AI inclination in this phase starts with understanding what consumers value about using AI when it comes to automating purchases and the AI tools they’re most apt to use.</p> <p><b>Insurance AI Inclination Index: The Buy phase</b></p>

#

<p><span class="small">Figure 3<br> Base: 8,451 respondents in the US, UK, Germany and Australia<br> Source: Cognizant Research</span></p> <p><b>Younger consumers lead AI engagement in the Buy phase</b></p> <p>The Buy phase sees peak engagement among the 35–44 cohort, whose AI inclination scores are 12 points higher than the 45–54 cohort. At this life stage, consumers are often just getting started on securing long-term insurance policies, managing higher-value investments and making complex financial commitments. This could translate into increased interest in how AI tools could simplify and automate the purchase phase.</p> <p>The youngest consumer cohort (18–24) shows moderate AI engagement with purchasing insurance, likely due to their auto insurance needs—one of the first major insurance products most people encounter. Here again, young consumers exhibit greater caution in investment purchasing, likely tied to their lower financial literacy and risk sensitivity.</p> <p>Older consumers (55+) remain engaged but show continued reliance on traditional decision-making approaches, particularly in investments. While AI plays a growing role in policy refinement and investment adjustments, trust for this generation remains a decisive factor. This is particularly true in life insurance, where financial security and personal risk assessment outweigh convenience-driven AI recommendations.</p> <p><a><b>Insurance continues to hold a slight edge over investments</b></a><b></b></p> <p>Once again, insurance edges out investments in terms of AI inclination. The dynamics are similar: Investments require a high degree of financial literacy and trust, while insurance purchases tend to be more structured, with standardized underwriting principles, defined coverage tiers, regulatory safeguards and comparison tools that ease the decision-making process.</p> <p>Readily available comparison tools are also directly integrated with insurer websites, making the transition from Learn to Buy more seamless, often reducing it to a single-click transaction. For instance, in the UK, one study found almost <a href="https://store.mintel.com/report/uk-price-comparison-sites-in-financial-services-market-report#:\~:text=UK%20Price%20Comparison%20Websites%20Market%20Statistics%20\*,using%20multiple%20sites%20in%20the%20last%20year." target="_blank">two-thirds (64%)</a> of consumers had used Compare the Market in 2023-2024. Such platforms provide full visibility and control, allowing consumers to compare policies side by side, evaluate pricing models and assess insurer reputations, all in one place.</p> <p>The growing adoption of usage-based pricing models, where AI analyzes driving behavior to automatically adjust premiums, further reinforces consumer trust in AI-enabled purchasing.</p> <p>Life insurance will likely follow a more cautious adoption curve as it carries long-term financial implications, making human oversight a critical factor in purchasing decisions. AI can assist with needs analysis, illustrations and underwriting, but consumers will likely continue to seek reassurance that their financial security is evaluated with transparency and fairness, not purely algorithmic logic.</p> <p>Consumers also have reason for concern over the use of algorithms in life insurance underwriting. The industry combines applicant-provided responses with data from external sources to assess mortality risk, even amid <a href="https://www.dfs.ny.gov/reports\_and\_publications/press\_releases/pr20240711241" target="_blank">continued regulatory scrutiny</a> of data neutrality and algorithmic bias. If consumers perceive AI as biased or unfair during the early stages of policy exploration, they may never progress to the Buy phase. This reinforces the need for clear, explainable AI models that build trust before purchasing even becomes an option.</p> <p>Investments present a different challenge. While robo-advisors and AI-driven portfolio modeling have grown in adoption, the stakes remain higher for consumers committing to automated financial strategies. Market fluctuations, risk exposure and long-term financial security make consumers more cautious about fully embracing AI-driven investment support. This hesitation is amplified by strict regulatory oversight, ensuring investment recommendations comply with fiduciary obligations and align with individual risk profiles.</p> <p><b>Conversational AI dominates again</b></p> <p>Conversational AI continues to be a dominant choice, although its role differs from that in the Learn phase. During the Buy phase, consumers primarily engage with AI-driven comparison platforms to evaluate policy pricing, coverage variations and insurer reliability. Conversational AI assists in clarifying terms, offering tailored purchase recommendations and guiding consumers toward decisions. However, full automation of purchasing remains limited, particularly in investments, where trust and regulatory compliance demand a hybrid approach.</p>

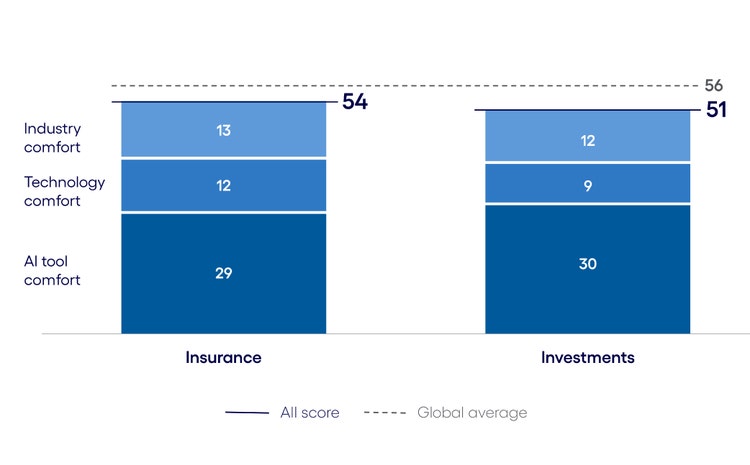

<h5>The Use phase: Big opportunities despite low AI interest</h5> <ul> <li><span class="eds-label">Older consumers are once again the most AI-inclined</span></li> </ul> <ul> <li><span class="eds-label">AI adoption lags across both insurance and investments</span></li> </ul> <ul> <li><span class="eds-label">AI tool preferences differ for insurance products vs. investments</span></li> </ul> <p>The Use phase is where we see the most hesitation about AI. Scores in all three areas of the index are the lowest of all three purchase journey phases, particularly the technology comfort component. This indicates a historic inability or unwillingness to use digital technologies such as smartphone apps when interacting with a range of insurance products. </p> <p>The dip in AI interest at this phase bucks the trend seen in our cross-industry report, where the Use phase sees an uptick in interest compared with Buy. It is also contrary to the expectation that AI could markedly simplify post-purchase interactions with insurance products and services. For example, AI could help provide real-time policy updates, assist with personalized risk management, streamline customer support through AI-driven chat services or offer proactive alerts for policy adjustments based on changing customer needs. </p> <p>As such, the Use phase holds substantial potential for AI to enrich and extend the business-consumer relationship through enhanced convenience and proactive support. Insurance businesses would do well to design, demonstrate and communicate the value of AI in this phase to unlock its considerable potential for post-purchase engagement.</p> <p><b>Insurance AI Inclination Index: The Use phase</b></p>

#

<p><span class="small">Figure 4 <br> Base: 8,451 respondents in the US, UK, Germany and Australia <br> Source: Cognizant Research</span></p> <p><b>Older consumers are once again the most AI-inclined</b></p> <p>While the oldest consumer cohort (55+) is the most highly AI-inclined for the insurance product category, it’s the 45–54 age group who—as in the Learn phase—shows the greatest engagement levels across both insurance and investments. Their continued reliance on AI in the Use phase is likely tied to their need to keep policies up to date, submit and track claims, and adjust their investment portfolios. In all these areas, AI-powered automation could offer a high level of convenience.</p> <p>Younger consumers (18–24) also show high levels of AI engagement for post-purchase insurance activities. Given that many in this age group are first-time policyholders, they are more inclined to interact with AI-powered tools for policy renewals, premium tracking and customer service inquiries.</p> <p>Investment products see the steepest decline in AI comfort during the Use phase, particularly among the youngest consumers (18–24). Hesitation here likely stems from lower perceived reliability in AI-driven portfolio adjustments, where real-time market volatility demands a higher degree of human financial oversight.</p> <p>The 55+ cohort also shows a decline in AI comfort for the investment product category, reinforcing skepticism about fully automated management of retirement savings or complex assets. Younger investors (25–44) are the most interested in engaging with AI-powered portfolio tools.</p> <p><b>AI adoption lags across both insurance and investments</b></p> <p>While both product categories fall below the global average, the investment product category trails significantly, sitting 15 points behind the global average, compared with insurance’s nine-point gap.</p> <p>Insurance maintains a relative advantage due to the structured nature of policyholder engagement. AI-driven tools have been integrated into claims processing, fraud detection and automated policy adjustments. AI-powered chatbots, for example, assist consumers in filing claims, tracking approvals and managing policy renewals, making AI adoption in insurance more transactional and service-oriented rather than purely advisory.</p> <p>However, challenges remain in achieving widespread consumer confidence. Many policyholders still encounter frustrations with automated claims adjudication, particularly when AI-generated decisions lack clear reasoning or avenues for dispute resolution.</p> <p>In contrast, investments struggle in the Use phase because AI-driven financial tools often prioritize prepurchase guidance rather than ongoing management. While robo-advisors and predictive analytics assist consumers in making initial portfolio choices, post-purchase AI interaction remains underdeveloped compared with insurance. Consumers often expect real-time market analysis, proactive risk alerts and portfolio adjustments tailored to shifting financial goals; however, AI in investments is still largely constrained to static monitoring functions rather than interactive, adaptive engagement.</p> <p><b>AI tool preferences differ for insurance products vs. investments</b></p> <p>In insurance, conversational AI could play a critical role in claims processing, policy management and customer support. Here, consumers engage with AI-powered assistants to file claims, track approvals and adjust coverage, making it the most widely used AI tool in the Use phase. The nature of insurance interactions, often routine but requiring clarity, makes conversational AI the preferred choice, as it allows for real-time explanations and ensures consumers feel supported throughout their policy lifecycle.</p> <p>In investments, preference is more evenly split between conversational AI and chatbots. While conversational AI provides interactive market insights and portfolio tracking, chatbots are seen as equally useful for transactional inquiries, such as balance checks, automated financial alerts and account servicing.</p> <p>The difference in engagement stems from consumer trust dynamics. While insurance claims and policy queries follow structured protocols, investment tools are expected to handle more nuanced financial decisions, leading consumers to engage with both static chatbots for simple interactions and conversational AI for more personalized financial insights.</p>

<h4>Meeting consumers where they are in insurance</h4> <p>Consumer use of AI is growing fast and, with it, the acceptance of consumer AI agents. For insurance consumers, AI agents will act like a personal risk manager and policy advisor, orchestrating complex tasks like tracking claims, optimizing coverage and even securing the best policy deals. Soon, the internet as we know it will become the agentic internet: an interconnected ecosystem of AI-enabled tools and agents that autonomously locate, evaluate, purchase and maintain the products and services people rely on.</p> <p>For the insurance sector, this means future insurance providers won’t exist in isolation. They’ll be deeply interconnected with other players in the broader financial ecosystem: payment providers, fintech innovators, even industries like healthcare or smart home technology.</p> <p>While consumer AI uptake may be somewhat slower in insurance, reflecting both cautious industry deployment and uneven consumer readiness, we believe leaders have less than five years to navigate this change. To prepare for the AI-driven consumer era ahead, insurance businesses will need to rethink how they operate across these areas:<b></b></p> <ul> <li><b>Prioritize hybrid human-AI models for high-stakes interactions</b>: Our research shows consumers are hesitant about fully automating the insurance journey with AI, particularly in the Use phase for investments and sensitive areas like claims processing. Given the high financial and emotional stakes, it’s key to take a hybrid approach, combining AI-driven analysis with human oversight.<br> <br> AI can efficiently generate initial recommendations, assess risk or process routine claims, but human advisors remain essential for interpreting complex insights, adapting solutions to individual circumstances, and providing the empathy and reassurance consumers seek.<br> <br> Transparency is key: By implementing clear, accessible processes for consumers to request human review of AI-driven decisions, insurers can ensure customers feel empowered and supported throughout their journey.<br> <br> </li> <li><b>Capitalize on the Learn phase with conversational AI: </b>Of the three stages in the purchase journey, customers are most comfortable using AI in<b> </b>the Learn phase, using conversational AI to discover their best options. This presents a prime opportunity for insurers to engage consumers early and build a foundation of trust. Insurers should double down on conversational AI to provide personalized, interactive guidance for policy exploration, comparison and understanding complex terms. By acting as an intelligent, accessible advisor, conversational AI can demystify insurance products, enhance financial literacy and influence decision-making long before a purchase is considered.<br> <br> </li> <li><b>Build function-first, age-inclusive strategies across the insurance value chain: </b>Our findings reveal a clear variation in consumer engagement across the insurance journey. Rather than promoting AI as a selling point, leaders must focus on functional and service benefits that address real needs across all age cohorts in the moments that matter.<br> <br> <ul> <li><b>For</b> <b>needs analysis and risk assessment,</b> younger users seek mobile-first tools for quoting and comparison, particularly in auto insurance, where usage-based pricing and channel-native delivery create transparency and ease. But across life and health, older and mid-career consumers need assurance: affordability modeling, guided advice and hybrid journeys that respect their expectations. Here, <b>AI earns trust not by its name but by how it shows up—quietly powering clarity and customization</b>.<br> <br> </li> <li><b>For servicing and post-purchase engagement, o</b>lder cohorts routinely engage with digital tools to monitor policies and manage renewals. Their priorities are anchored in efficiency, simplicity and control, and their relevance is long-term: <b>a 55-year-old today is still decades away from aging out of the system, making loyalty and trust across digital channels a high-stakes investment</b>. Mid-career users are receptive to digital servicing for wealth products, provided it’s explainable and optional. Younger users expect seamless support and proactive nudges but often lack deep brand attachment. Loyalty will follow if service delivers—<b>not if it dazzles, but if it works</b>.<br> <br> </li> <li><b>With</b> <b>claims and fraud</b>, consumers across generations value empathy and speed when navigating claims. Conversational AI and automation can help, but only when service design prioritizes <b>clarity, responsiveness and fairness</b>. The value lies not in the technology’s presence, but in its effectiveness at reducing friction, and ensuring human touch is available, when wanted.</li> </ul> </li> </ul>

Jump to a section

Introduction #spy-1

AI across the insurance consumer journey #spy-2

subnav- The Learn phase: Policy comparison capabilities bolster comfort with AI#spy-21

subnav- The Buy phase: Trust issues and high stakes force an AI inclination drop#spy-22

subnav- The Use phase: Big opportunities despite low AI interest#spy-23

Meeting consumers where they are in insurance #spy-3

<h5>Authors</h5>