RESEARCH

How consumer AI adoption will change the car-buying journey

<p><br> <span class="small">August 14, 2025</span></p>

How consumer AI adoption will change the car-buying journey

<p><b>Our AI Inclination Index reveals which consumers are most open to using AI in the car-buying journey—as well as where and how they’ll use it. With this insight, automotive organizations can develop a highly nuanced and effective consumer-facing AI strategy.</b></p>

<p>AI tools have already started shaping how people explore, configure, purchase and maintain vehicles. From virtual showrooms to AI-enabled maintenance reminders, the landscape is changing fast. Yet the automotive customer journey is also very personal and emotionally charged, layered with cost considerations, safety expectations and long-term commitments.</p> <p>For automakers, dealers and mobility providers, this creates a distinct challenge: How do you tap into growing consumer interest in AI while acknowledging the hesitation that persists? Consumers may not fully trust AI-led pricing and financing recommendations. They may want more transparency into how trade-in values or service alerts are generated. And they may want transactional control when navigating a high-stakes purchase that is still heavily associated with face-to-face negotiations.</p> <p>For these reasons, the growing use of AI among consumers poses a distinct challenge for automotive brands. Which consumers are most (and least) inclined to use AI? Which tool would they prefer to use? And where in the purchase process would they be most comfortable using it? </p> <p>Our recent research uncovered some nuanced answers to those questions. Using data from our recent consumer AI study, we developed the AI Inclination Index, which quantifies consumers’ propensity to use the technology (see explainer box below).</p> <p>While the index reveals a lower inclination to use AI when purchasing cars than other industries’ products and services (see Figure 1), that broad finding masks important variations. For instance, consumers’ comfort levels differ dramatically across the three key phases of the consumer journey (Learn, Buy and Use).</p> <p><b>Consider some of these findings on AI adoption in the automotive customer experience:</b></p> <ul> <li><b>The Learn phase is where consumers are most apt to use AI. </b>Comfort with AI is highest, by far, in the research stage. Whether comparing trims, building a configuration or understanding financing models, consumers see the value in AI helping to simplify the discovery process. However, inclination scores drop sharply in the Buy and Use phases, reflecting hesitation to rely on AI when making high-stakes decisions and managing vehicle ownership.<br> <br> </li> <li><b>AI inclination varies dramatically across consumer age groups and purchase journey stages. </b>The youngest cohort (18–24) leads in the Learn phase, suggesting a strong affinity for AI-driven digital exploration tools. However, it's the 25–34 age group that shows the strongest engagement during both the Buy and Use phases—indicating a growing comfort with AI-enabled transactions and ongoing car ownership experiences. Conversely, consumers 55+ are highly interested in the Learn and Use phases but markedly hesitant about using AI in the purchase itself.<br> <br> </li> <li><b>Conversational AI is the tool of choice across stages.</b> Consumers gravitate toward interactive, dynamic tools that offer tailored insights and guidance. In the Learn phase especially, conversational AI consistently receives the highest comfort scores. Its ability to reduce complexity and help users ask nuanced questions like, “Which electric SUVs under $50,000 offer lane assist?” make it a vital tool for confidence-building in early research.</li> </ul> <p><b>The AI Inclination Index</b></p> <p><i>To quantify consumers' propensity to adopt AI-driven technology features throughout the consumer journey, we developed the AI Inclination Index. The index was calculated using three measures from our New minds, new markets survey data.</i></p>

#

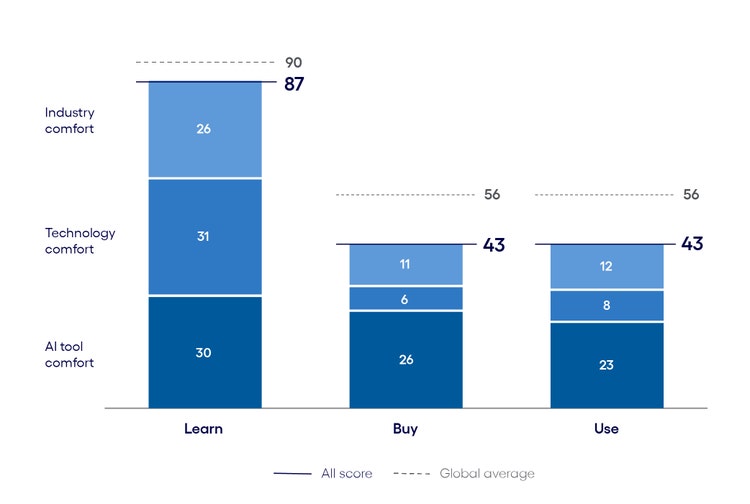

<p><b><br> AI inclination in automotive vs. the global average </b></p> <p><i>Automotive consumers are moderately less inclined to use AI than the global average across each stage of the consumer journey—with the largest gaps appearing in the Buy and Use phases.</i></p>

#

<p><span class="small">Figure 1<br> Base: 8,451 respondents in the US, UK, Germany and Australia<br> Source: Cognizant Research</span></p> <p>With these variances, it’s clear automotive organizations must tailor their AI strategy to engage consumers where they are most receptive, while thoughtfully mitigating barriers that emerge at vital moments such as purchase.</p> <p>Understanding consumer use of AI, as well as the accompanying pockets of spending power, is essential for leaders in all industries. In our global study “<a href="https://www.cognizant.com/us/en/new-minds-new-markets-ai-customer-experience" target="_blank">New minds, new markets</a>,” we found that consumers who are enthusiastic about using AI will account for up to 55% of all purchases made across industries. This amounts to $4.4 trillion in spending in the US, $690 billion in the UK, $690 billion in Australia and $540 billion in Germany.</p> <p>In this report, automotive leaders will learn about where in the car-buying journey consumers are most and least inclined to use AI, the AI tools they would be most apt to use and differences across age groups. With this information, businesses can reshape their approach to customer engagement—where and how it matters most.</p>

<h4>AI across the auto buying journey</h4> <p>As our AI Inclination Index indicates, consumers are less inclined than the cross-industry average to use AI across all three stages of the car-buying journey: Learn, Buy and Use. This lag is most notable in the Buy and Use phases, where scores fall 13 points below the global benchmark.</p> <p>Such hesitation reflects two core dynamics:</p> <ul> <li><b>AI does not yet support the emotional and financial weight of vehicle ownership. </b>Unlike in other sectors like retail or entertainment, automotive decisions involve long-term implications around financial risk, safety and lifestyle identity. Consumers are willing to research with AI, but they hesitate to hand over control when consequences are high. <br> <br> In the Use phase, that hesitation persists: AI here doesn’t fail because the tech is missing, it fails because the consumer value isn’t visible. While predictive maintenance is already built into many vehicles, it’s often under-leveraged. The real friction lies in post-sale servicing: opaque pricing, inconsistent experiences and limited visibility once the dealership hands over the keys.<br> <br> This disconnect isn’t accidental. Dealerships often act as gatekeepers between consumers and manufacturers—intentionally controlling the customer relationship. That model restricts the flow of useful vehicle data and blocks the transparency telematics could offer. Even when a car "knows" what’s wrong, the consumer doesn’t—leaving service needs, costs and vehicle health buried in a black box.<br> <br> </li> <li><b>Consumers perceive AI as opaque during the most consequential moments.</b> In the Buy phase, the data shows a sharp drop in inclination scores, especially among first-time and older buyers. This indicates discomfort with AI-driven decision-making consumers can’t fully see or influence. Tools like AI-powered trade-in valuations or finance approvals are only valued if car buyers understand how those decisions are being made. If it feels like a black box, they opt out.</li> </ul> <p>While the automotive industry has made strides in embedding AI into behind-the-scenes workflows, such as dynamic inventory pricing, demand forecasting and fleet management, the adoption of consumer-facing AI tools is marked by caution. For example, online configurators increasingly use AI to suggest bundles based on lifestyle indicators, but uptake still drops off at the transaction stage.</p> <p>The challenge for automakers and mobility providers will be to close the visibility and value gap: Consumers need AI to feel less experimental and more indispensable across their ownership lifecycle.</p> <p>Building trust, particularly during purchase moments and ongoing usage, will be key to unlocking AI’s full potential in the automotive experience.</p>

About our analysis

To understand consumer AI behaviors and attitudes at a granular level, we structured our analysis around four key pillars:

- The consumer journey. We studied the specifics of AI use at each phase of the customer journey. This journey—how consumers discover, purchase and engage with products and services before and after a sale—is at the heart of the business-customer relationship.

- Consumer demographics. To gain a better understanding of how consumer attitudes and behaviors differ by age group, we divided consumers into five categories: 18-24, 25-34, 35-44, 45-54, and 55+.

- Consumer AI tools. We defined consumer AI use by asking about their intended use of three key tools that are prevalent in the consumer world: voice assistants, chatbots and conversational AI.

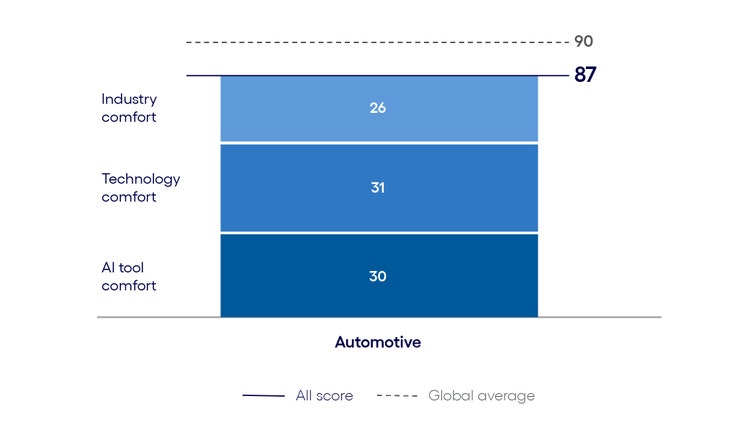

<h5>The Learn phase: Digital exploration drives early AI engagement for auto buyers</h5> <ul> <li><span class="eds-label">Consumers embrace AI to simplify complex vehicle research</span></li> </ul> <ul> <li><span class="eds-label">Younger buyers lead, but interest spans age groups</span></li> </ul> <ul> <li><span class="eds-label">Conversational AI is the tool of choice</span></li> </ul> <p>The Learn phase ranks as the most comfortable stage for AI adoption in automotive. With a total AI inclination score (87) falling just below the global average (90), it represents a critical opportunity for brands to engage consumers during early exploration—and before crucial decision-making sets in.</p> <p>Whether researching trims, comparing specs, exploring financing or reviewing fuel economy credentials, consumers are turning to AI tools to simplify the discovery process, especially when product complexity or emotional investment is high.</p> <p>Success for automotive organizations depends on understanding what drives AI adoption—what consumers find most useful, which tools they prefer and how businesses can enhance transparency and trust in AI-powered discovery.</p> <p><b>Automotive AI Inclination Index: The Learn phase</b></p>

#

<p><span class="small">Figure 2<br> Base: 8,451 respondents in the US, UK, Germany and Australia<br> Source: Cognizant Research</span></p> <p><b>Consumers embrace AI to simplify complex vehicle research</b></p> <p>Consumers’ strong interest in using AI to research vehicles reflects a broader shift in how people approach high-consideration purchases. As vehicle options expand—from powertrains and trims, to financing models and digital features—AI tools offer a way to cut through complexity. Virtual assistants, smart configurators and AI-powered recommendation engines are increasingly used to match vehicles to lifestyle, budget and environmental priorities.</p> <p>As one consumer put it, “AI plays an important role in providing personalized recommendations based on factors like my driving habits, preferred brands, budget and even environmental concerns. AI also helps compare technical specifications, highlight the different safety ratings and even suggest financial options or maintenance cost based on one’s budget and area of location.”</p> <p>The growing interest in AI is set against a backdrop of mounting consumer hesitation. UK new-car registrations fell by over <a href="https://autovista24.autovistagroup.com/news/uk-new-car-registrations-suffer-worst-result-in-almost-three-years/" target="_blank" rel="noopener noreferrer">10% in April 2025</a>—the sharpest drop in nearly three years. The decline was driven in part by confusion around new legislation and added costs for EVs, which created uncertainty and delayed purchase decisions. This is a stark reminder that when the research journey feels fragmented or opaque, demand suffers.</p> <p><b>Younger consumers lead, but interest spans age groups</b></p> <p>The 18–24 cohort shows the strongest AI inclination during the Learn phase, with an index score of 69. This underscores their comfort with digital-first discovery methods. For many, researching a first vehicle online is a familiar, intuitive experience enhanced by AI.</p> <p>That said, interest is far from limited to younger buyers. Consumers aged 45–54 (who scored 62 on the index) and 55+ (with a score of 63) report nearly as much comfort, suggesting that older generations also value AI-driven clarity when evaluating vehicle options. Whether it's understanding fuel efficiency trade-offs, ownership costs or advanced safety features, AI-enabled tools help demystify decision criteria that would otherwise require multiple dealership visits.</p> <p>This broad base of engagement positions the Learn phase as a high-impact moment for AI adoption—one where brands can make exploration feel effortless, insightful and even enjoyable.</p> <p><b>Conversational AI is the tool of choice</b></p> <p>In the Learn phase, consumer comfort with conversational AI consistently outpaces both chatbots and digital voice assistants. This reflects a growing preference for tools that offer dynamic, two-way dialogue and tailored guidance, especially when navigating a high-consideration purchase like a car.</p> <p>Conversational AI provides a more intuitive and responsive alternative to static configurators or rigid chatbot scripts. By allowing consumers to ask complex or open-ended questions, such as “What’s the best hybrid for city driving under $50,000?”, these tools can deliver personalized insights, contextual recommendations and confidence-building explanations.</p>

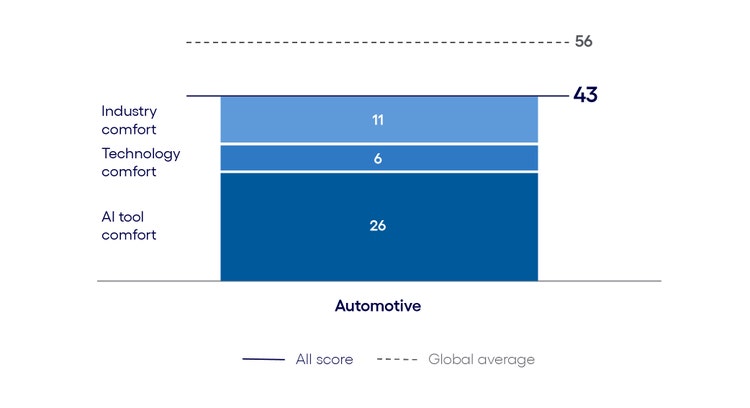

<h5>The Buy phase: Trust issues and high stakes force a drop in auto buyers’ AI interest</h5> <ul> <li><span class="eds-label">Complexity and risk dampen consumer AI confidence</span></li> </ul> <ul> <li><span class="eds-label">25–34-year-olds lead AI engagement in the purchase phase</span></li> </ul> <ul> <li><span class="eds-label">Conversational AI continues to play a pivotal support role</span></li> </ul> <p>AI inclination drops sharply in the Buy phase, plummeting 44 points from the Learn phase and 13 points below the global average. While consumers are increasingly open to using AI for research, the moment of financial commitment still triggers caution and, in many cases, skepticism.</p> <p>Capitalizing on AI potential in this phase begins with understanding what consumers value when completing complex, high-cost transactions like vehicle purchases, and what role they’re comfortable assigning to AI in the decision-making process.</p> <p><b>Automotive AI Inclination Index: The Buy phase</b></p>

#

<p><span class="small">Figure 3<br> Base: 8,451 respondents in the US, UK, Germany and Australia<br> Source: Cognizant Research</span></p> <p><b>Complexity and risk dampen consumer AI confidence</b></p> <p>Vehicle purchases involve layered considerations: financing structures, long-term maintenance expectations, emotional attachments and safety implications. For many, a car is the most expensive piece of technology they own. According to a study by Motor Finance, <a href="https://www.motorfinanceonline.com/news/most-drivers-feel-overwhelmed-by-car-tech-features/?cf-view" target="_blank">86% of Brits</a> say this is true of their automobile. While AI is welcomed for comparisons, consumers often draw the line at handing it full control over the final decision.</p> <p>Current industry tools, such as AI-led deal finders, instant credit preapproval engines and real-time inventory matching, are beginning to bridge the gap. However, full automation remains rare. Most consumers still expect a hybrid experience: digital-first for research and qualification; human-led for negotiation and closing.</p> <p>And that expectation is far from hypothetical. According to <a href="https://retailtimes.co.uk/omoda-reveals-showroom-visits-remain-crucial-for-76-of-car-buyers-despite-digital-shift/" target="_blank">research by OMODA</a>, almost three out of four car buyers still value visiting car showrooms, with 64% of UK car buyers wanting a hands-on test drive before committing to a purchase.</p> <p>The shift toward online car buying platforms such as Carvana and Cinch has started to normalize digital transactions. However, even these services often involve live agent support, underscoring that AI alone is not yet viewed as sufficient for automotive decisions.</p> <p><b>25- to 34-year-olds lead AI engagement in the Buy phase</b></p> <p>AI inclination is highest among those aged 25–34 (with a score of 41), many of whom are transitioning from entry-level cars to more lifestyle-driven or family-oriented choices. For this cohort, AI adds value through loan simulations, trade-in valuations and dynamic price comparisons that streamline what can be a tedious, fragmented process.</p> <p>By contrast, the 18–24 group shows low engagement (with a score of 23) despite being digital natives. The purchase of a vehicle, often their first major financial commitment, may feel too consequential to trust AI without human validation. Older consumers (55+) also show lower engagement (with a score of 22), reflecting continued preference for human-led negotiations and concerns over transparency in AI-generated recommendations.</p> <p>This creates an inflection point: AI must evolve from a discovery companion to a transactional partner, offering clarity and control without sacrificing the sense of agency that buyers of all generations value.</p> <p><b>Conversational AI continues to play a pivotal support role</b></p> <p>Conversational AI maintains a presence in the Buy phase, though its role shifts from exploration to facilitation. Consumers use it to clarify pricing breakdowns, compare financing options or assess trade-in scenarios; such tasks benefit from AI’s ability to synthesize complex information on demand.</p> <p>However, chatbots and digital voice assistants gain only modest traction, as they often lack the flexibility or precision needed for nuanced conversations about credit terms, lease vs. purchase considerations or value-added service bundles.</p> <p>This phase reinforces the importance of explainable, transparent AI. If consumers are to trust AI with part of the decision-making load, they need tools that not only answer questions but also show their math.</p>

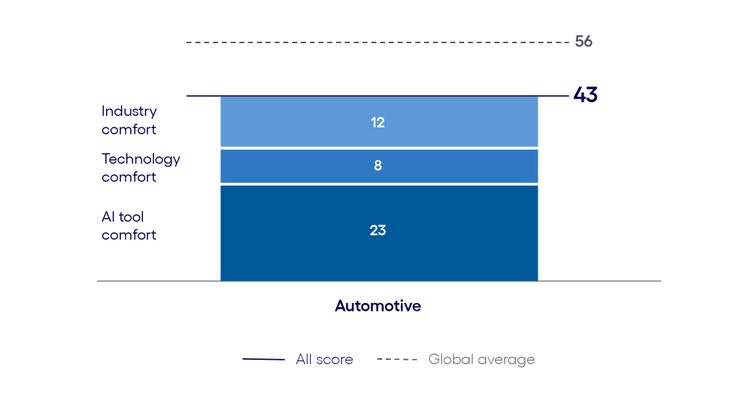

<h5>The Use phase: Value gaps and low visibility blunt AI’s potential for auto buyers</h5> <ul> <li><span class="eds-label">AI adoption lags despite robust Use-phase features</span></li> </ul> <ul> <li><span class="eds-label">Mid-career consumers lead again in the post-purchase phase</span></li> </ul> <ul> <li><span class="eds-label">Conversational AI shows potential for ongoing support, but trust must be earned</span></li> </ul> <p>AI inclination scores are similarly low for the Use phase, also trailing the global average by 13 points. While automakers and mobility providers have deployed a range of connected services, from predictive maintenance alerts to digital service scheduling, the promise of these AI-driven offerings has yet to translate into everyday value for consumers, who seem to feel disconnected from the benefits of AI once the vehicle is in their hands.</p> <p>Notably, this dip in AI interest bucks the trend seen in our cross-industry report, where the Use phase sees an uptick in comfort and engagement compared with the Buy phase. It is also contrary to the expectation that AI could help drivers stay informed, anticipate needs and resolve issues before they escalate, reinforcing trust well beyond the point of sale.</p> <p>Automotive businesses would do well to design, demonstrate and communicate the value of AI in this phase to enrich and extend the relationship between automotive brands and consumers—transforming post-purchase engagement into a more seamless, intelligent and responsive experience.<b></b></p> <p><b>Automotive AI Inclination Index: The Use phase</b></p>

#

<p><span class="small">Figure 4<br> Base: 8,451 respondents in the US, UK, Germany and Australia<br> Source: Cognizant Research</span></p> <p><b>AI adoption lags despite robust Use-phase features</b></p> <p>While AI plays a major role in back-end systems for powering diagnostics, service scheduling and fleet operations, these benefits often remain invisible or disjointed to the consumer. Ownership-phase AI features are frequently fragmented across OEM apps, third-party services, dealer platforms and vehicle user interfaces.</p> <p>As the European Commission observed in its <a href="https://digital-strategy.ec.europa.eu/en/library/workshop-ai-automotive-barriers-challenges-and-opportunities" target="_blank">2025 workshop report</a>, fragmented ecosystems and limited data access are major obstacles to AI deployment in the automotive sector. Consumers may not see clear benefits or may be unaware of existing functionality altogether. The issue isn’t a lack of innovation—it’s a lack of intuitive, cohesive integration into the ownership experience.</p> <p>But fragmentation isn’t the only issue. Dealerships typically operate as the primary customer touchpoint, with data access and service visibility often routed through their systems. This structure makes it more difficult for consumers to fully benefit from AI features like predictive diagnostics and cost estimators, especially when transparency around servicing and pricing remains limited.</p> <p>While most brands have already introduced more proactive tools, such as real-time alerts for tire pressure, battery status or warranty renewals, these systems still feel reactive and shallow. What’s missing is a more intelligent feedback loop: status reports that contextualize diagnostics, clarify service cost ranges and help drivers make informed decisions—without handing over control. AI’s future in the Use phase isn’t more alerts. It’s better accountability.</p> <p><b>Mid-career consumers lead post-purchase AI interest</b></p> <p>Despite low inclination overall, AI comfort in the Use phase is strongest among 25- to 34-year-olds (with a score of 33). This group is accustomed to managing services through mobile apps and open to proactive alerts, maintenance reminders and usage-based insurance adjustments. These consumers often prioritize efficiency and convenience, making them more receptive to digital tools that simplify ownership.</p> <p>The 18–24 and 55+ cohorts follow closely behind (with scores of 26 and 29, respectively). Younger users may be more willing to experiment with connected vehicle features, especially in app-native formats, while older drivers show interest in AI when it offers clear utility, like avoiding unnecessary service visits or tracking running costs.</p> <p>The 45–54 group shows the lowest score (24), suggesting frustration or skepticism about the usefulness and reliability of AI in day-to-day ownership.</p> <p><b>Conversational AI shows potential for ongoing support, but trust must be earned</b></p> <p>Conversational AI shows the most promise in supporting post-purchase engagement. From guiding service appointment scheduling to helping explain dashboard alerts or recommending service intervals, this tool can offer consumers contextual guidance that builds confidence over time.</p> <p>But while overall AI inclination in the Use phase remains low, a closer look at the index reveals a key nuance: Comfort with AI tools significantly outpaces comfort with traditional tech interfaces. Automotive tech comfort sits at just eight, while AI tool comfort rises to 23. This suggests consumers may be more open to AI-led support than legacy digital channels if the experience is well designed, transparent and intuitive.</p> <p>By contrast, chatbots and digital voice assistants lag behind, often falling short in offering real-time answers to practical, vehicle-specific questions. As with the Buy phase, success depends on transparency, accuracy and human-override mechanisms that reassure users they’re not stuck with a black-box solution.</p>

<h4>Meeting consumers where they are in the auto buying journey</h4> <p>Consumer use of AI is accelerating, and with it, the emergence of intelligent, embedded AI agents capable of managing entire aspects of the vehicle journey. For automotive consumers, AI will soon function like a virtual co-driver, financing consultant and service advisor rolled into one, handling everything from model discovery to post-purchase maintenance scheduling and real-time driving optimization.</p> <p>This evolution points toward a larger transformation: the rise of the agentic internet, a hyper-connected ecosystem of AI-enabled agents that autonomously source, compare, transact and manage the products and services consumers rely on. For automotive brands, this shift will require deep integration not just across internal systems but also with navigation apps, insurance providers, EV charging networks, service centers and beyond.</p> <p>While consumer AI inclination in automotive currently lags behind other industries, particularly in high-trust and post-purchase moments, leaders have a narrow window to get ahead of the curve. To prepare for the AI-powered mobility era, industry stakeholders must rethink how they operate across three critical areas:</p> <ul> <li><b>Rebuild trust at the transaction point</b>: Consumers’ sharp drop in AI engagement from Learn to Buy highlights a deep trust gap. To close it, brands must reframe AI not as a salesperson, but as an advocate. <br> <br> Explainable loan estimators, transparent trade-in calculators and AI-powered incentives that clearly show what’s driving pricing decisions can shift perception from “automation” to “empowerment.” Businesses should focus on offering hybrid experiences where AI supports but doesn’t substitute for human interaction during high-stakes moments.<br> <br> </li> <li><b>Elevate post-purchase utility through proactive visibility and consumer-first integration:</b> In the Use phase, the issue isn’t a lack of AI; it’s a lack of integration and clarity. Predictive maintenance features may be standard in modern vehicles, but consumers still lack access to critical data about their car's condition, servicing history and cost breakdowns. Much of this remains siloed within dealership systems, leaving drivers dependent and disengaged.<br> <br> To build trust and drive adoption, AI must do more than trigger alerts—it needs to democratize vehicle data. That means surfacing real-time health diagnostics, transparent pricing estimates and servicing timelines—all delivered through the platforms drivers already use. When AI acts as an ownership ally, not just a software feature, it unlocks a new kind of utility: one rooted in control, confidence and continuous value.<br> <br> </li> <li><b>Let conversational AI drive first impressions and lasting connections:</b> We found strong consumer comfort with conversational AI during the early exploration phase. Automakers should expand beyond “build and price” tools and create intelligent advisors that guide users through lifestyle-fit vehicles, ownership costs, charging options and green incentives. These tools can help brands stand out before a consumer ever sets foot in a showroom and continue delivering value during ownership.</li> </ul>

Jump to a section

Introduction #spy-1

AI across the auto buying journey #spy-2

subnav- The Learn phase: Digital exploration drives early AI engagement for auto buyers#spy-21

subnav- The Buy phase: Trust issues and high stakes force a drop in auto buyers’ AI interest#spy-22

subnav- The Use phase: Value gaps and low visibility blunt AI’s potential for auto buyers#spy-23

Meeting consumers where they are in the auto buying journey #spy-3

<h5>Authors</h5>