How RegTech optimizes compliance for banks (Part 2) styles-h2 text-white

data-xy-axis-lg:null; data-xy-axis-md:null; data-xy-axis-sm:30% 40%

<p><span class="medium"><br>April 27, 2022</span></p>

How RegTech optimizes compliance for banks (Part 2)

<p><b>Distributed ledger technology, combined with other emerging RegTech technologies, promises to be a game-changer for banking and the financial services industry.</b></p>

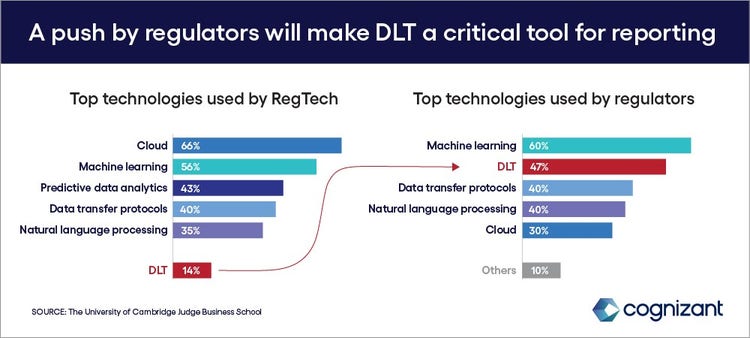

<p>Distributed ledger technology (DLT), automation, data analytics and artificial intelligence (AI) have shown great promise in reinventing complex regulatory reporting systems that regulators, along with banks and financial institutions, have long sought to simplify. Particularly, DLT has emerged as a tool that promises to transform regulatory reporting, heralding the “pull era.”</p> <p>In <a href="/content/cognizant-dot-com/us/en/insights/perspectives/how-regtech-optimizes-compliance-for-banks.html" target="_blank">part 1</a> of this series, we looked at how RegTech offers hope in an increasingly complex regulatory reporting landscape. Now we’ll explore how DLT can act as the core and unifying platform for resolving longstanding reporting bottlenecks and facilitating on-demand reporting.</p> <p>DLT’s immutability, transparency and ability to create single point of truth, among other features, is seen as an antidote to the current, highly complex, regulatory reporting process. Banking regulations, which are trending toward greater granularity and transparency, will soon demand that financial institutions engineer a shift from a report-generation model to an embrace of standardized granular data and enhanced timeliness.</p> <p>These pressures, plus the potential to unlock cost savings in processes such as trade-and-transaction reporting and reconciliation and <a href="https://www.thomsonreuters.com/en/press-releases/2016/may/thomson-reuters-2016-know-your-customer-surveys.html" target="_blank">Know Your Customer</a> (KYC) regulations, are set to push banks and financial institutions toward DLT, with as many as <a href="https://www.blockdata.tech/blog/general/banks-investing-blockchain-companies" target="_blank">55 of the world’s top 100 banks</a> investing in blockchain or crypto start-ups.</p> <p>This all-round ability to enhance reporting has put DLT high on regulators’ list of transformative technologies, as the following illustration shows. Regulators’ push toward DLT is a key force in motivating banks and financial institutions to embrace it.</p>

#

<h4><br> How to drive DLT-led changes in regulatory reporting</h4> <p>Regulators and banks and financial institutions have long suffered from diverging compliance reports, long waiting periods and avoidable penalties.</p> <p>Building granular reporting processes suitable for exploiting the power of DLT will require all stakeholders to cooperate. We believe regulators, financial institutions and providers should work in coordination in what might be termed an ecosystem, in which where banks and financial institutions’ disparate systems and advanced RegTech solutions work hand-in-hand with a DLT-based reporting platform. Banks and financial institutions, along with regulators, will be required to enact significant technological changes. We believe the following requirements are critical for driving transformation.</p> <h5><b><i>1</i>.</b> Develop robust governance.</h5> <p>The governance model is at the heart of a DLT-based reporting platform. With the interests of multiple stakeholders in play, it should be designed to enable decision-making and change management that builds and sustains trust. This also enables scaling of the DLT platform; new participants must be onboarded easily as the platform matures. Data sharing and data integrity will be critical to achieve this. DLT’s capability to create an auditable trail and automated access; to enable metadata sharing; and to integrate new participants as and when needed make it an ideal base technology on which to build an inclusive reporting platform.</p> <p>One necessity for effective governance is an agreement on data standards such as usage of metadata, anytime access of data, etc. Agreements on audits, data integrity and data aggregation are also needed. These agreements need to be reached ahead of any material investments between stakeholders. We believe banks and financial institutions must move internal data processing and storage over a DLT network. Final reporting would be to move blocks over a network managed by regulators.</p> <h5><b><i>2</i>.</b> Evolve a consistent taxonomy.</h5> <p>A comprehensive taxonomy of components of a DLT-based reporting platform will dictate the key design choices of the reporting system. A standardized set of definitions helps distil insights from the relationships between thousands of data points of a DLT system for all the participants and, ultimately, reduce cost of implementation. An effort to create such a taxonomy has to be collaborative in nature, involving key industry players, RegTech providers and regulators. The <a href="https://www.regulationasia.com/how-a-consortium-created-the-mas-610-open-taxonomy/" target="_blank" rel="noopener noreferrer">Monetary Authority of Singapore</a>, for instance, worked with a consortium of stakeholders to create a taxonomy that filters 300,000 data points into 1,000 reusable business concepts, thus making it easy for banks and financial institutions to understand regulatory asks and report accordingly.</p> <h5><b><i>3</i>.</b> Drive substantial changes to regulatory reporting processes.</h5> <p>DLT can help create granular data-based processes that let regulators directly access required information, saving the time and costs involved in requesting data. However, all trading and other transactional data at banks and financial institutions currently flows through disparate systems as reports are generated. The regulator then checks the input for consistency. If a DLT-based platform is to become operational, banks and financial institutions need to generate their data in a manner compatible with the main DLT. This would mean substantial changes at all levels within the organization. Banks and financial institutions realize the value blockchain can bring. In a cross-industry survey we did last year, <a href="/content/dam/connectedassets/cognizant-global-marketing/marketing-channels/cognizant-dotcom/en_us/insights/documents/the-work-ahead-in-banking-and-financial-services-the-digital-road-to-financial-wellness-codex6473.pdf" target="_blank" rel="noopener noreferrer">banks outpaced other industries</a> in piloting blockchain technology. This high level of optimism suggests that banks and financial institutions are willing to make the changes necessary for a move to DLT.</p> <p>The onset of granular reporting means that regulators too need to build processes and applications that proactively mine information required for banking supervision and better regulation.</p> <h5><b><i>4</i>.</b> Automate to overcome data challenges.</h5> <p>We believe banks and financial institutions should deploy technologies such as AI, automation and big-data analytics to bring a level of uniformity necessary to work with a DLT-based reporting platform. This way, they can create a single source of financial records, ensuring that everyone on the blockchain — regulators and the regulated — has access to the same validated record. This results in standardization at the operational data level and transparency that automates reporting and reduces the need for reconciliation. Streamlining and standardizing data also helps create an auditable trail that will be critical in meeting regulatory demands for granularity. Smart contracts can be used for automated data validation and data consistency checks, while natural language processing can parse regulatory texts and automatically populate databases that regulatory reports run on.</p> <h5><b><i>5</i>.</b> Re-architect reporting.</h5> <p>Building DLT-based reporting will require an overhaul of existing architectures at banks and financial institutions. We experienced the breadth of change required for this first-hand during our work with a securities depository in India to create an authoritative data store of immutable, time-stamped records of debentures and underlying assets. The initiative sought to bring transparency in debenture and asset charges, prevent double spend, streamline asset validation, and improve participant collaboration.</p> <h5><b><i>6</i>.</b> Harness the power of machines.</h5> <p>Machine learning and neural networks have emerged as technologies that can enhance a DLT-based reporting platform by improving the nuts-and-bolts functions in regulatory reporting. Examples include the following.</p> <ul> <li><b>Report pulling</b>: The UK’s Financial Conduct Authority has proposed a <a href="https://www.fca.org.uk/publication/feedback/fs18-02.pdf" target="_blank" rel="noopener noreferrer">digital regulatory reporting</a> model based on a machine-readable regulatory language that machines could understand, removing the need for human interpretation. Machines could then use this language to automatically execute rules. Banks and financial institutions should leverage such models to facilitate a shift to the pull model of reporting.<br> <br> </li> <li><b>Cutting</b> f<b>alse positives</b>: Reducing false positives in anti-money laundering and combating terrorist financing operations is a top priority for the industry. <a href="https://www.reuters.com/article/bc-finreg-laundering-detecting-idUSKCN1GP2NV" target="_blank" rel="noopener noreferrer">Only 1% to 2%</a> of the millions of suspicious action reports worldwide are known to be correct. Machine learning can be leveraged to augment existing transaction monitoring efforts and improve detection of anomalies in customer behavior. This can reduce false positives while making KYC processes more efficient.<br> <br> </li> <li><b>Building predictive</b> <b>capabilities:</b> Banks and financial institutions and regulators can build predictive capabilities leveraging granular data made available over distributed ledgers using modern digital tools such as analytics to let their organizations take timely actions. While regulators have the opportunity to deploy predictive insights to take proactive supervisory actions, financial institutions can use predictive insights for improving compliance. For instance, they can nip compliance failures in the bud and prevent penalties. Auto-encoders are an unsupervised learning technique that use neural networks that can be deployed to augment complex decisions and processes. Experimental results on real-world payment data show that autoencoders can detect <a href="https://www.sciencedirect.com/science/article/abs/pii/S095741740800078X" target="_blank" rel="noopener noreferrer">financial failure</a> at banks as well as <a href="https://www.axionable.com/fraud-detection-keras-mlp-autoencoder/" target="_blank" rel="noopener noreferrer">credit card fraud</a>.</li> </ul> <h5><b><i>7</i>.</b> Future-proof the reporting mechanism.</h5> <p>DLT, with its ability to provide vast volumes of high-quality data, can act as a technological base layer<b> </b>upon which<b> </b>other emerging technologies and advances in machine learning, natural language processing and neural networks can be integrated to further enhance regulatory reporting and related functions. Banks and financial institutions should design their DLT-based standardized reporting mechanisms to remain flexible to keep pace with ever changing regulatory requirements.</p> <h4>Looking forward</h4> <p>DLT-based reporting platforms, alongside other emerging technologies, can bring much needed transparency, efficiency gains and cost optimization in the financial regulatory reporting landscape. While these are still early days, the needs of an increasingly digital world transformed by the pandemic have created a sense of urgency among regulators and banks and financial institutions alike to leverage these technologies to resolve longstanding bottlenecks in reporting.</p> <p><i>This article was written by Vinod Malpani, Gaurav Mundra and Suprotim Dutta, Senior Director, Senior Manager and Consultant respectively with Cognizant’s Banking and Financial Services Consulting Practice.</i></p> <p><i>For more information, visit the <a href="/content/cognizant-dot-com/us/en/industries/banking-technology-solutions.html" target="_blank" rel="noopener noreferrer">Banking section</a> of our website or <a href="/content/cognizant-dot-com/us/en/about-cognizant/contact-us.html" target="_blank" rel="noopener noreferrer">contact us</a>.</i></p>

<p>We’re here to offer you practical and unique solutions to today’s most pressing technology challenges. Across industries and markets, get inspired today for success tomorrow.</p>